Editor’s Note: The Daily Brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 200+ that read this report daily, below!

What Happened

Overnight, equity index futures auctioned sideways, providing some more validation to Thursday morning’s reversal fueled by aggressive short-covering.

Geopolitical tensions and monetary tightening are the two major narratives news outlets are assigning to the volatility.

The U.S. and its allies applied more sanctions on Russia for its invasion of Ukraine and markets are still pricing around six quarter-point rate hikes by the Fed.

Ahead is data on personal income, consumer spending PCE inflation, core inflation, disposable income, durable goods orders, and core capital equipment orders (8:30 AM ET), University of Michigan sentiment, inflation expectations, and pending home sales (10:00 AM ET).

What To Expect

Fundamental: Must keep it short, today.

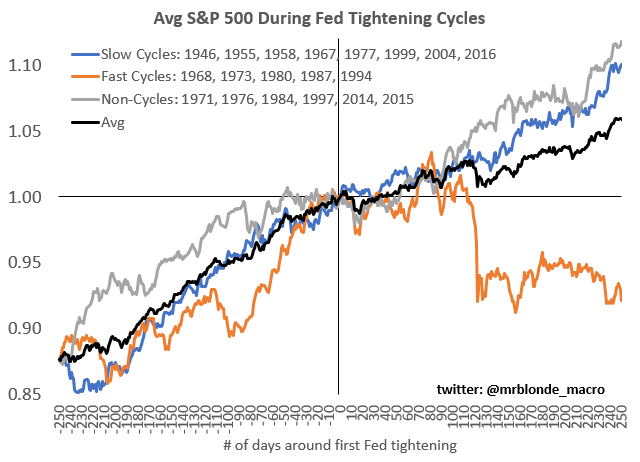

Per JPMorgan Chase & Co’s (NYSE: JPM) Marko Kolanovic, “While Equities are down year-to-date due to rising rates, we note that historically the initial volatility around rate liftoff didn’t last and equities made new all-time highs 2-4 quarters out.”

“The start of policy tightening is usually a confirmation that the cycle has legs, rather than the signal of its end. As we don’t see the yield curve inverting or real yields reaching problematic levels this year, it is premature to talk about end-of-cycle worries.”

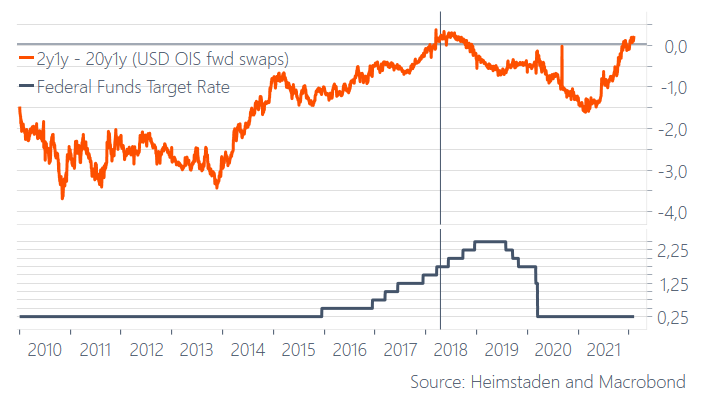

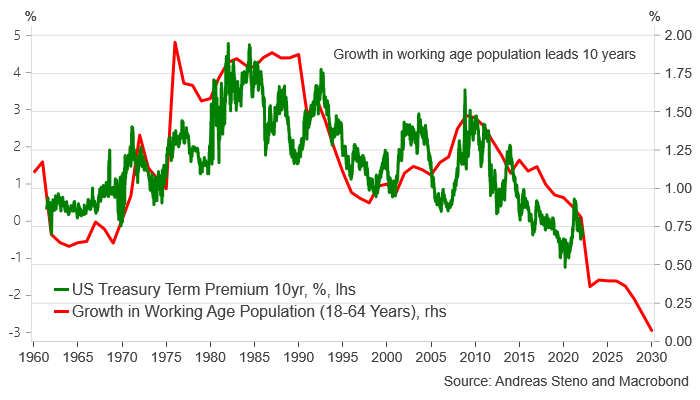

Pursuant to Kolanovic’s remarks, Andreas Steno Larsen of Heimstaden explains that bond yields remain governed by demographics, and this is good news for tech.

“I still think that inflation and bond markets will be governed by other structural trends over the medium term,” he said. “Just look at the growth rate of the working-age population (10 years forward) versus the term premium of US Treasury bonds. The current bond bear market is not standing on structural pillars.”

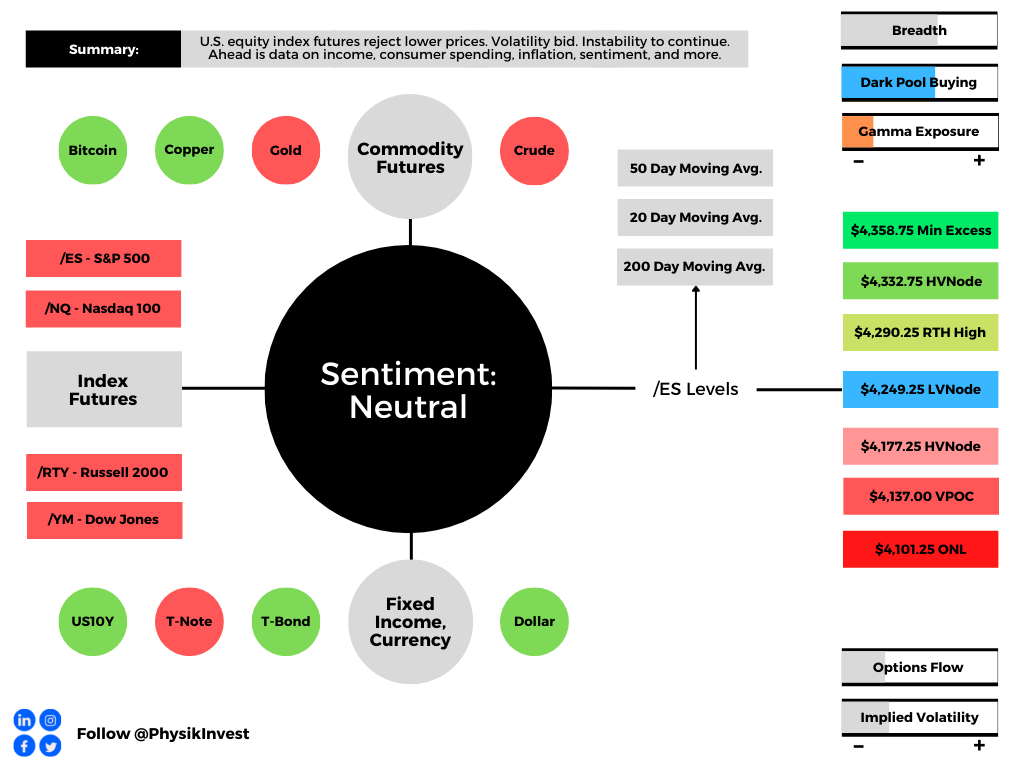

Positioning: Based on a variety of metrics, some of which were pointed to in yesterday’s commentary, there were no clear signs of capitulation.

For instance, one of the largest ETF products that track the Nasdaq 100 (QQQ) “has seen persistently illiquidity (daily range / $ volume). There was not much volume (participation) behind the move in price. The 1-week return distribution gets pretty wild.”

Similarly, “1 Month relative volume (today’s volume / 1-month average) on SPY today (1.66) doesn’t have a capitulatory look to it. Bottoms in the past year occurred at 2+.”

There was, however, a massive covering of short (negative delta) exposures. The gap lower presented participants a “gift” and many took it as an opportunity to monetize downside bets.

Despite metrics pointing to continued accumulation, and buying support, equity products are in negative gamma wherein the hedging of put-heavy exposures results in whip-saw action (i.e., options counterparties hedge in a manner that exacerbates moves to upside and downside).

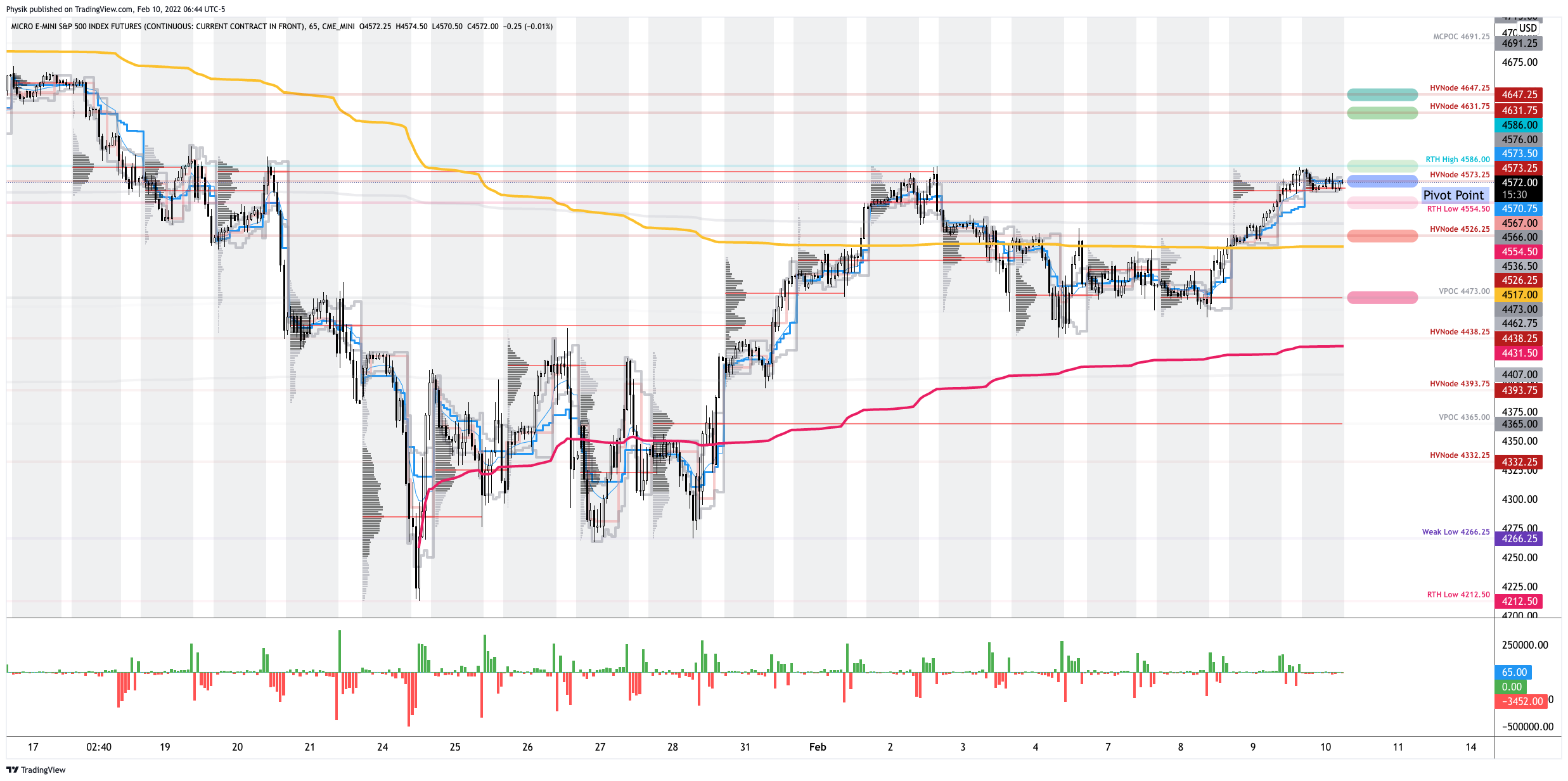

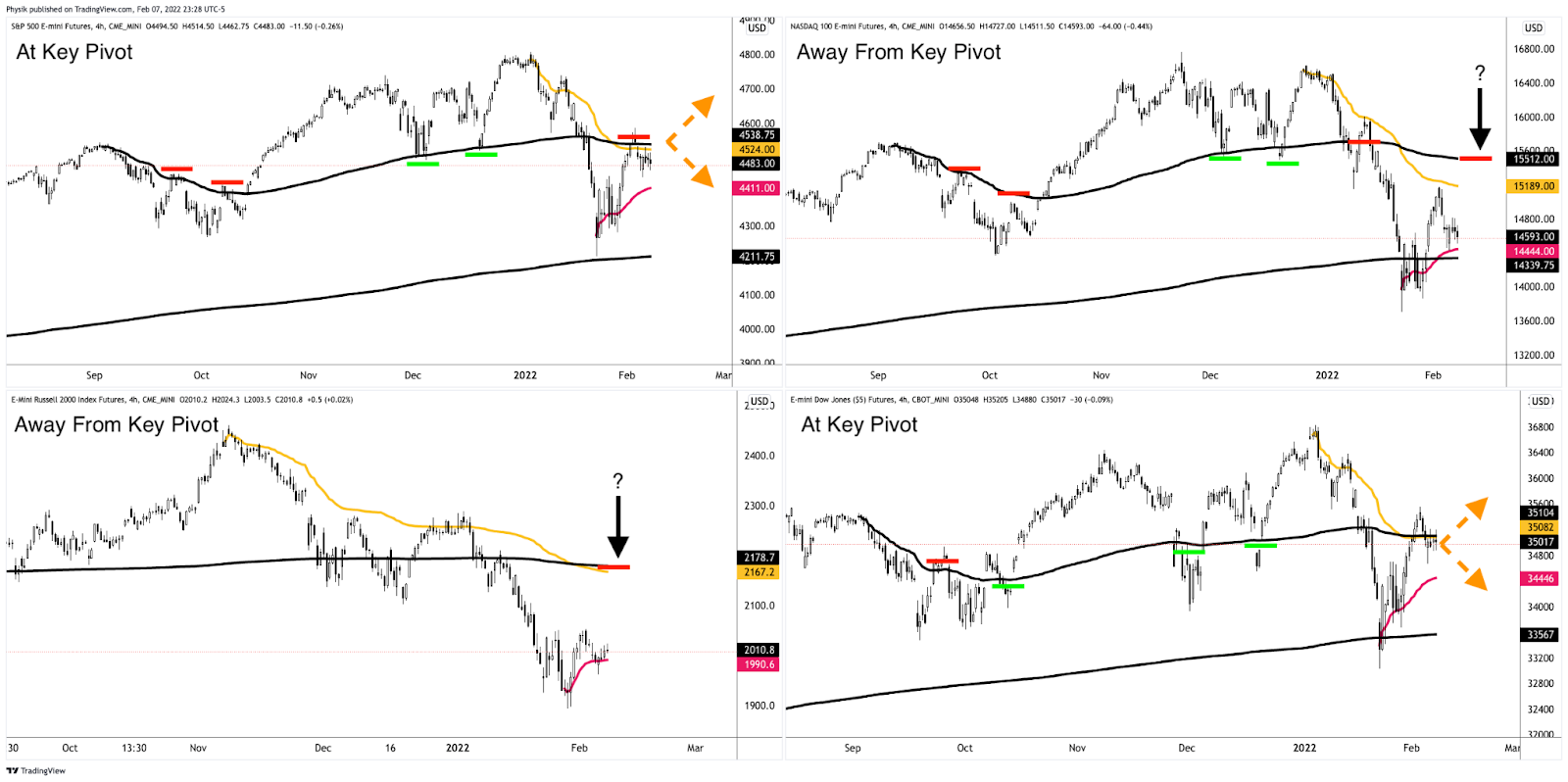

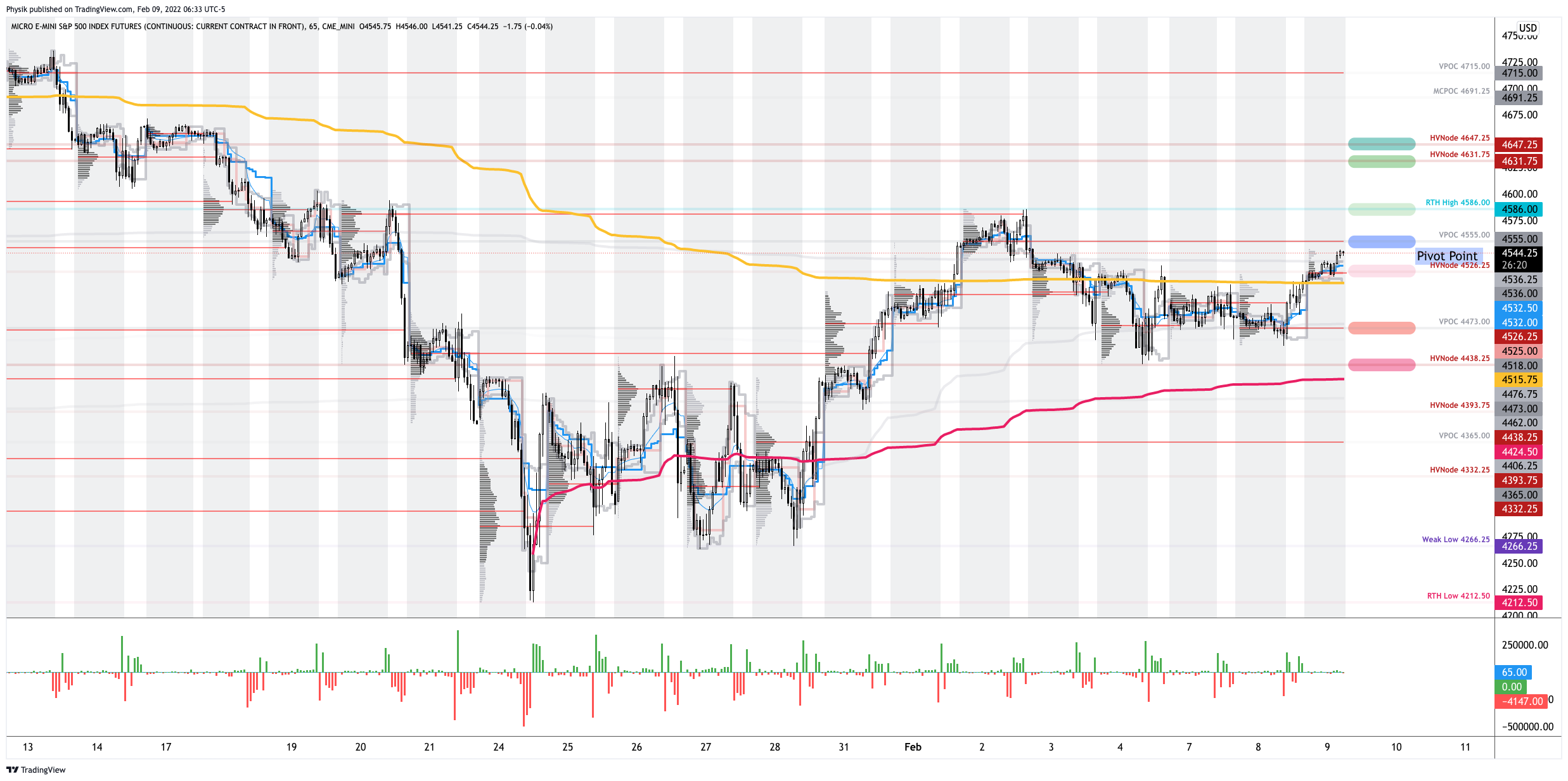

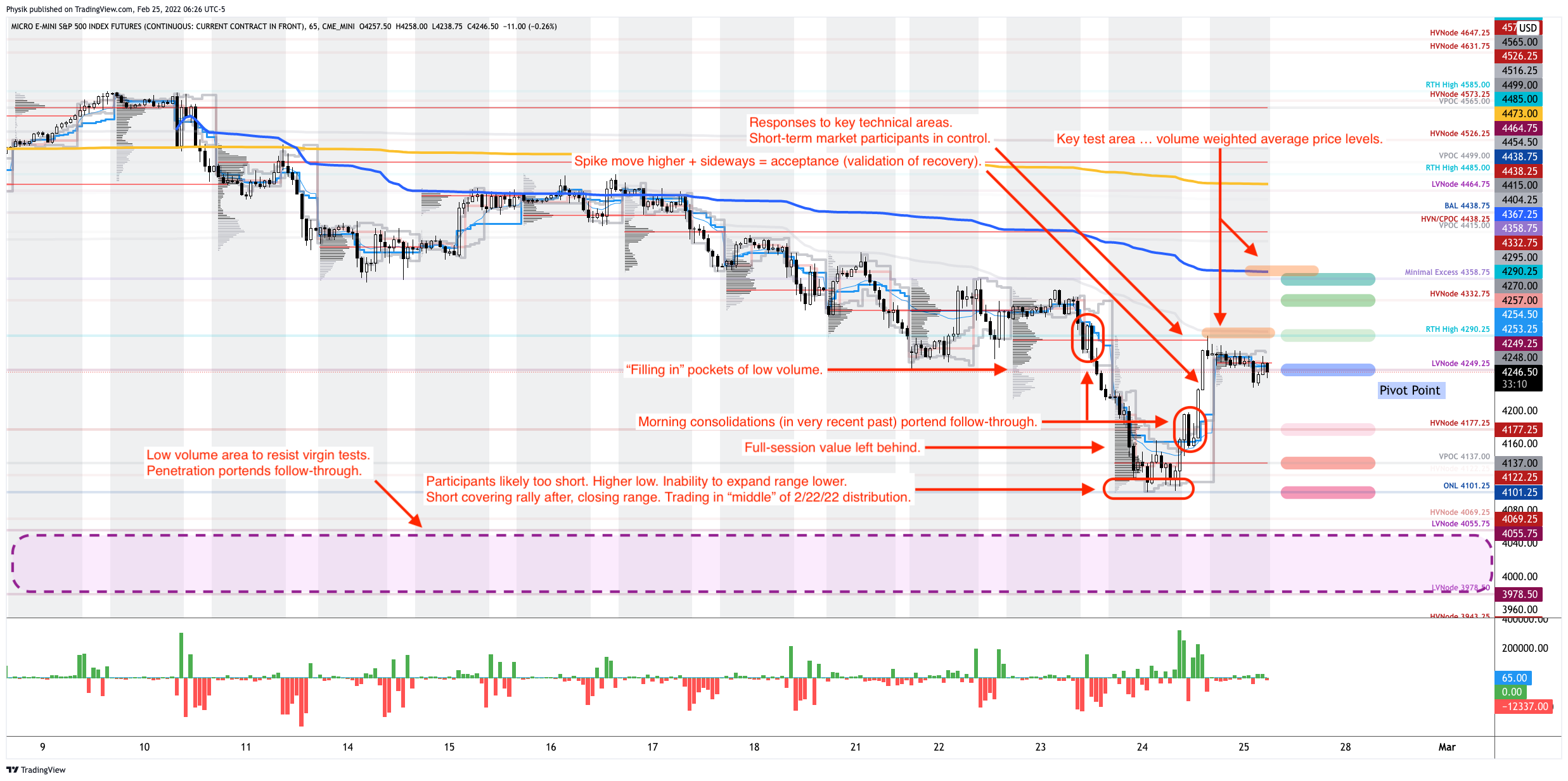

Technical: As of 6:30 AM ET, Friday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the upper part of a balanced skewed overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher; activity above the $4,249.25 low volume area (LVNode) puts in play the $4,290.25 regular trade high (RTH High). Initiative trade beyond the RTH High could reach as high as the $4,332.75 high volume area (HVNode) and $4,358.75 minimal excess high, or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,249.25 LVNode puts in play the $4,177.25 HVNode. Initiative trade beyond the HVNode could reach as low as the $4,137.00 untested point of control (VPOC) and $4,101.25 overnight low (ONL), or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Definitions

Overnight Rally Highs (Lows): Typically, there is a low historical probability associated with overnight rally-highs (lows) ending the upside (downside) discovery process.

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

Excess: A proper end to price discovery; the market travels too far while advertising prices. Responsive, other-timeframe (OTF) participants aggressively enter the market, leaving tails or gaps which denote unfair prices.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj is also a Benzinga finance and technology reporter interviewing the likes of Shark Tank’s Kevin O’Leary, JC2 Ventures’ John Chambers, FTX’s Sam Bankman-Fried, and ARK Invest’s Catherine Wood, as well as a SpotGamma contributor developing insights around impactful options market dynamics.

Disclaimer

Physik Invest does not carry the right to provide advice.

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.