Market Commentary

Equity index futures sideways overnight. Volatility ebbs.

- Senate passed debt-ceiling raise.

- Ahead: NFP, unemployment data.

- Clarity regarding tapering by Fed.

- Responsive selling into RTH high.

What Happened: U.S. stock index futures auctioned sideways overnight alongside news that the Senate passed a short-term debt ceiling increase.

Ahead is data on nonfarm payrolls, the unemployment rate, and average hourly earnings (8:30 AM ET), as well as wholesale inventories (10:00 AM ET).

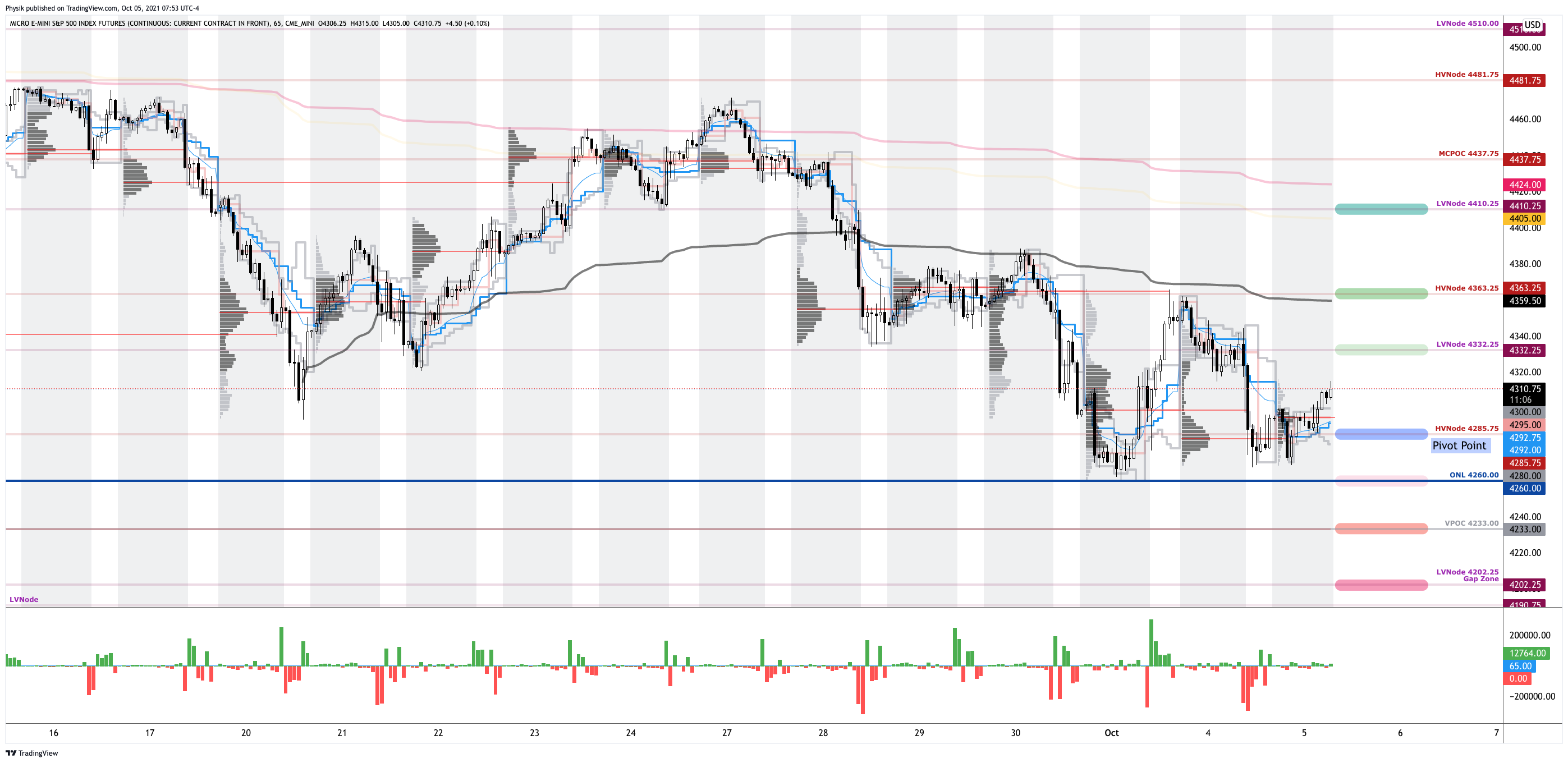

What To Expect: As of 6:40 AM ET, Friday’s regular session (9:30 AM – 4:00 PM EST) in the S&P 500 may open inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

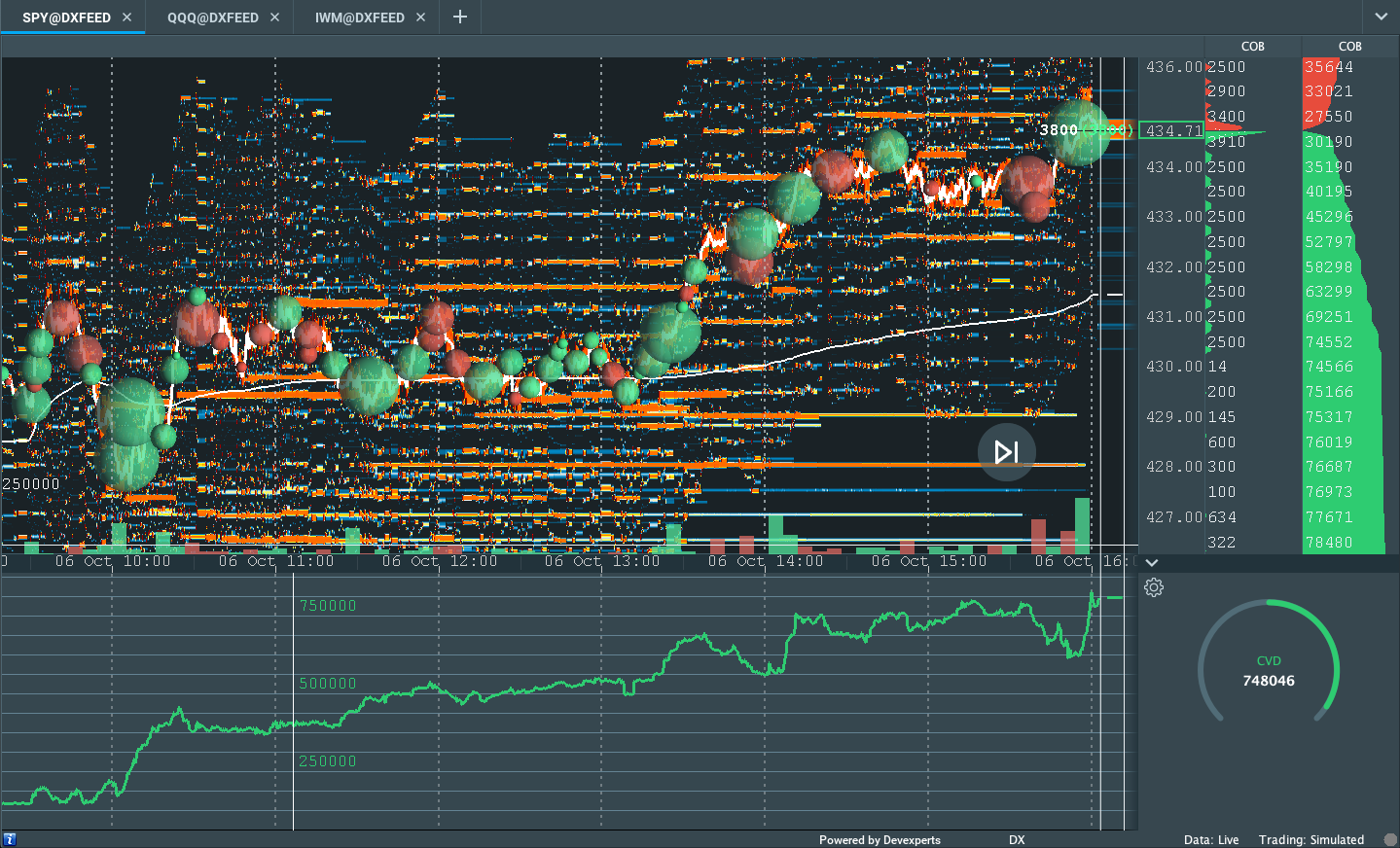

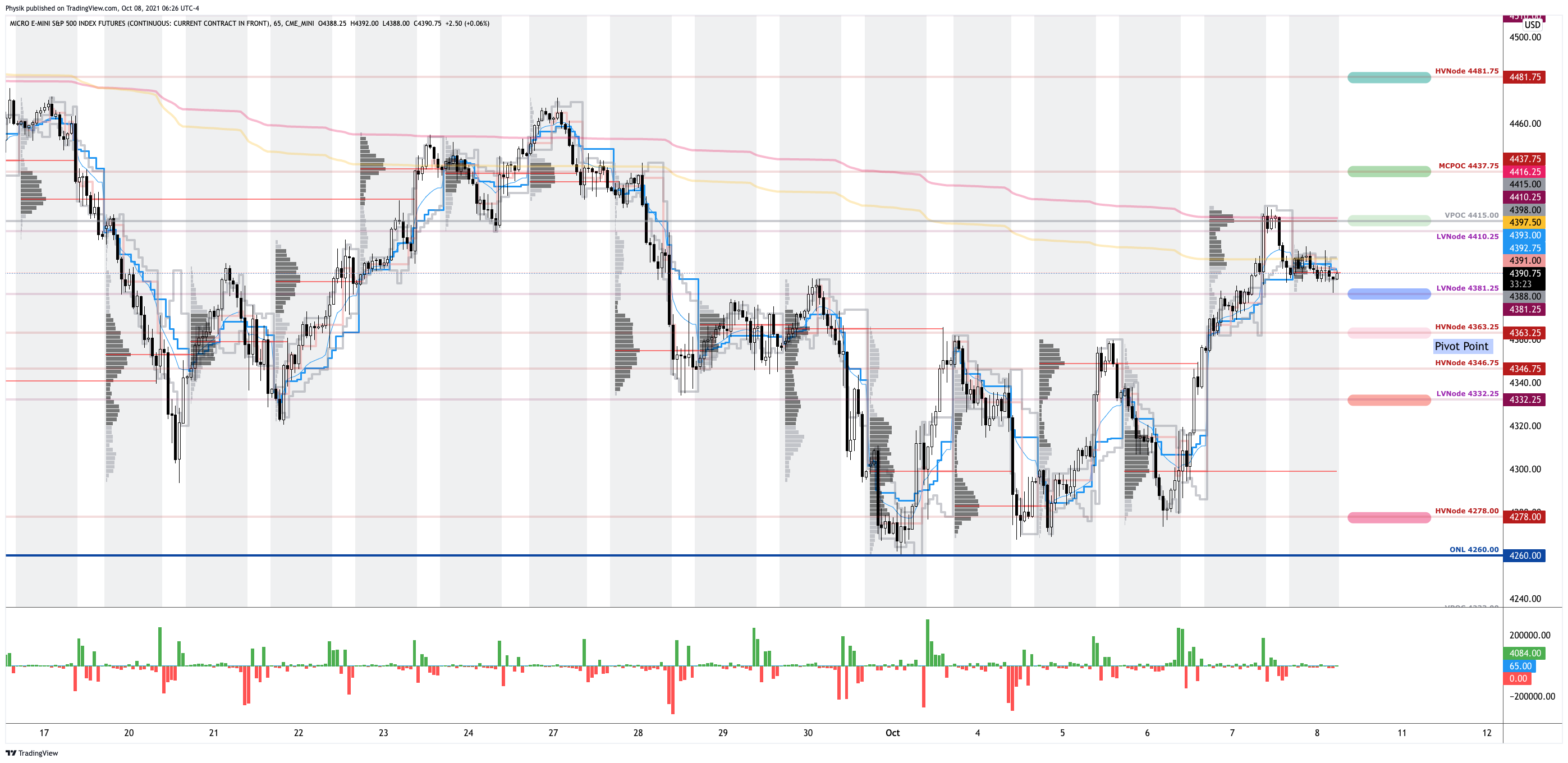

During the prior day’s regular trade, on strong intraday breadth and divergent market liquidity metrics, the best case outcome occurred, evidenced by the expansion of range and value above the $4,410.25 low volume area (LVNode), between two key anchored-volume weighted average price (AVWAP) levels.

Into the price rise, however, we note that participants sold responsively (i.e., sold in response to prices printing above an area of recent acceptance or balance); as prices came into the resting liquidity (Graphic 2) – also the location of a key AVWAP in – at and around /ES $4,410.25 (SPY $441.00), buying and selling power as calculated by the difference in volume traded at the bid and offer diverged, markedly.

In other words, at the AVWAP – a metric highly regarded by chief investment officers, among other participants, for quality of trade – there were liquidity algorithms programmed to sell. Why? Liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

This trade is significant because it suggests a willingness to slow price discovery and balance (i.e., trade sideways as participants look to establish an equilibrium in light of new information).

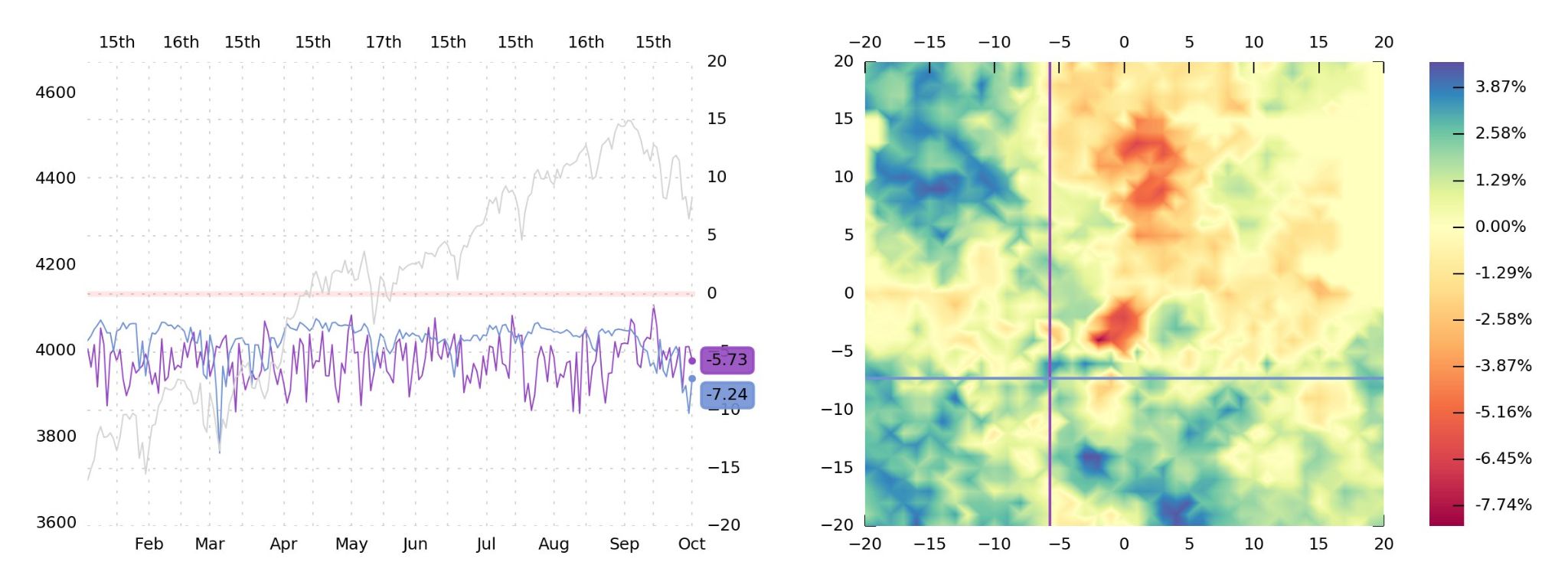

We’re carrying forward the presence of a p-shaped emotional, multiple-distribution profile structure (i.e., old-money shorts covering) left behind prior initiative trade, as well as continued trade below the 20- and 50-day simple moving averages; these dynamics induce anxiety and stress for the technical-driven, weaker-handed buy-the-dip crowd.

Further, the aforementioned trade is happening as investors await key employment data that will provide context on what the Federal Reserve with respect to monetary policy.

According to Bloomberg, Friday’s payroll data – which is likely to indicate strong improvement – likely emboldens tapering initiatives and improves the prospects of a rise in the Fed funds rate.

“What we see in the equity space is a lot of sensitivity to higher real yields,” Joseph Little, chief global strategist at HSBC Asset Management, said. “We are seeing policy normalization everywhere. That creates a little bit of a challenge for equity market because it does change the drivers of equity performance.”

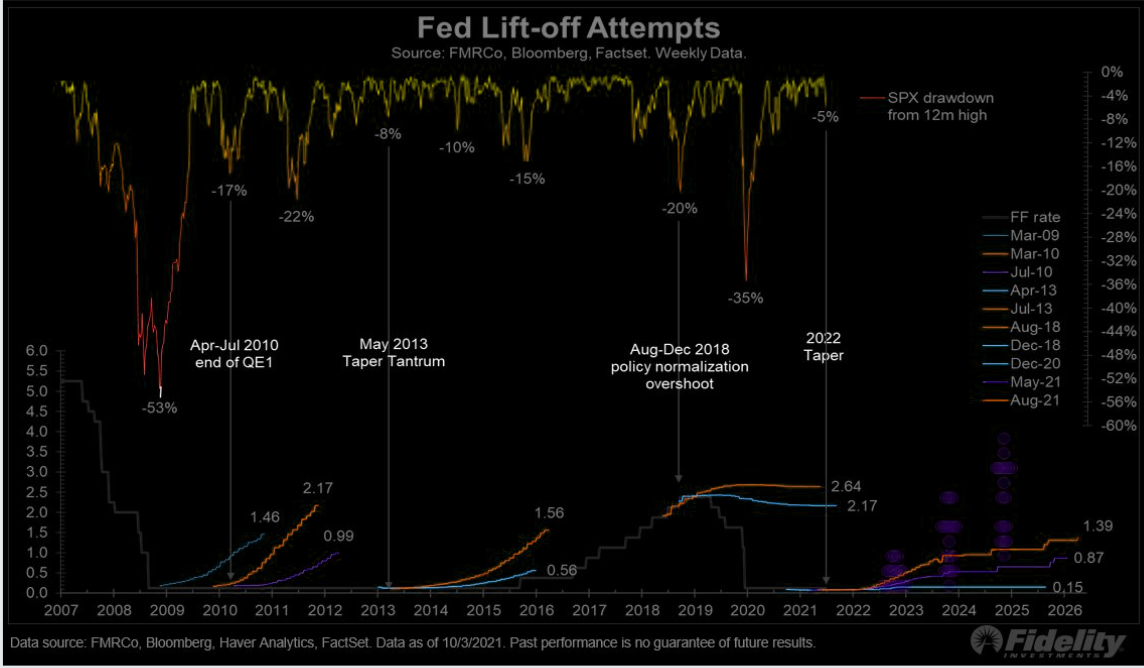

Adding, earlier this week, we noted that indices were best positioned for a vicious rebound as near-term downside discovery metrics likely reached a limit. These dynamics remain.

Moreover, for today, participants may make use of the following frameworks.

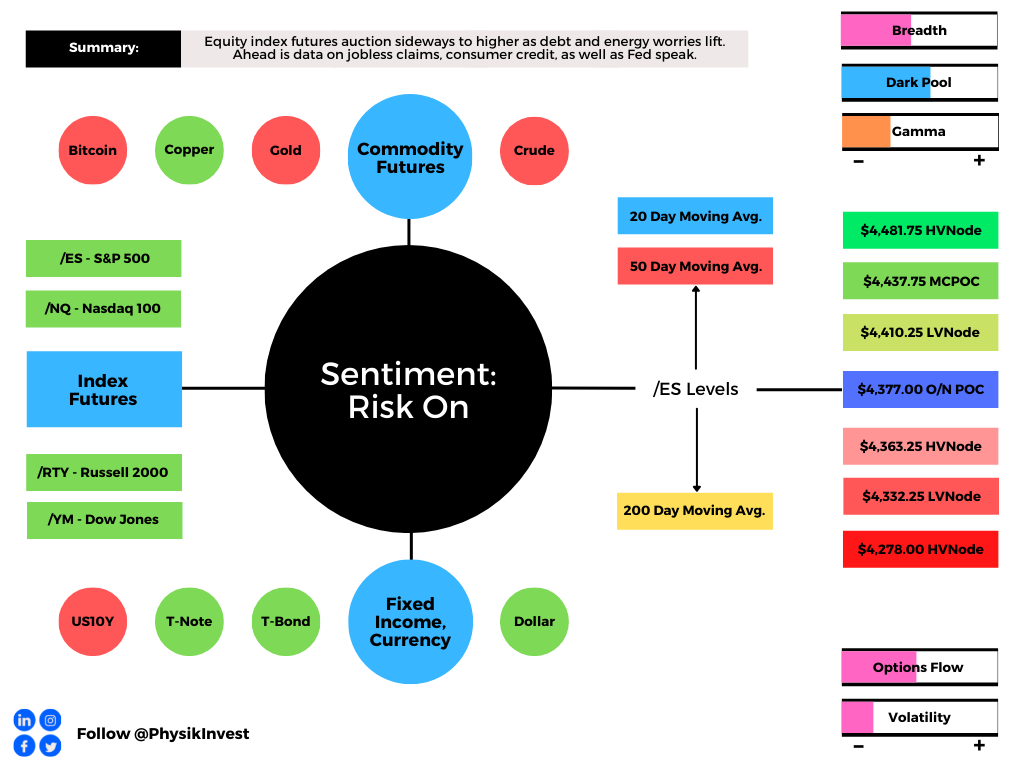

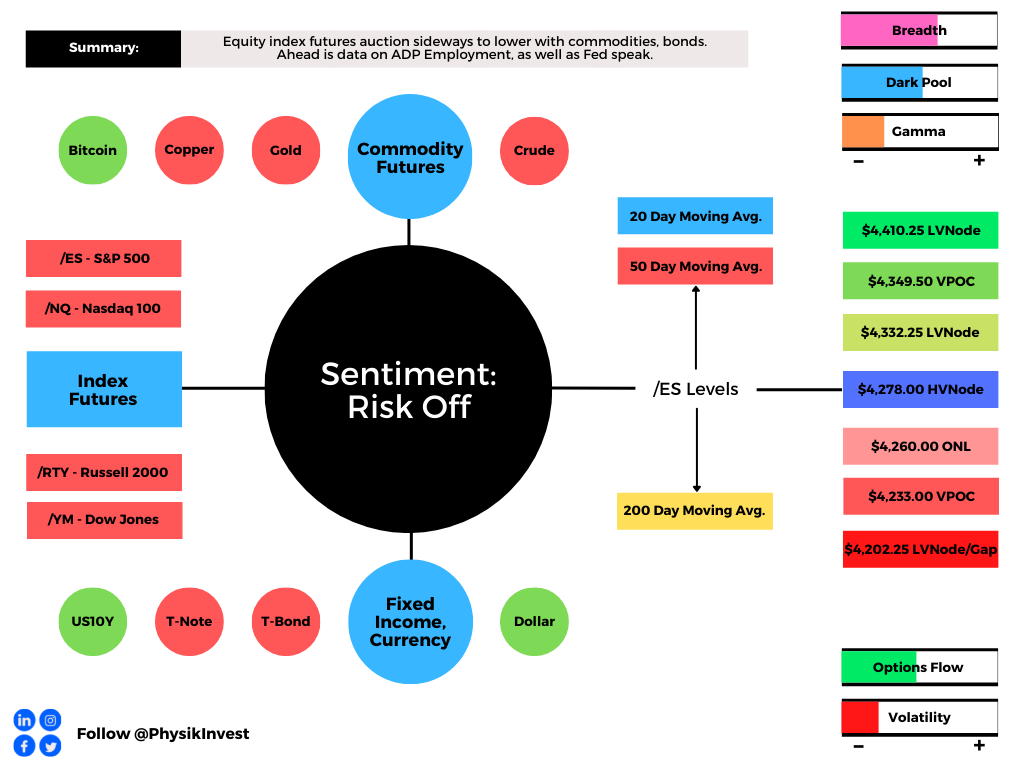

In the best case, the S&P 500 trades sideways or higher; activity above the $4,381.25 low volume area (LVNode) puts in play the $4,415.00 untested point of control (VPOC). Initiative trade beyond the VPOC could reach as high as the $4,437.75 micro-composite point of control (MCPOC) and $4,481.75 high volume area (HVNode), or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,381.25 LVNode puts in play the $4,363.25 HVNode. Initiative trade beyond the HVNode could reach as low as the $4,332.25 LVNode and $4,278.00 HVNode, or lower.

Definitions

Balance (Two-Timeframe Or Bracket): Rotational trade that denotes current prices offer favorable entry and exit. Balance-areas make it easy to spot a change in the market (i.e., the transition from two-time frame trade, or balance, to one-time frame trade, or trend).

Modus operandi is responsive trade (i.e., fade the edges), rather than initiative trade (i.e., play the break).

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

More On Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

Short Covering: The profile shape suggests participants were “too” short and had poor location.

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

News And Analysis

Short-term increase in U.S. debt ceiling passes Senate.

U.S. special operations rotating into Taiwan for training.

Moody’s: Kicking [debt limits] not too far down the road.

Energy Transition: Demand destruction stalking Europe.

APAC CBDCs – pathways plenty, destination uncertain.

Vaccinations and policy decisions are key to EM growth.

Richest Americans flee Treasuries with holdings at lows.

Crypto Mystery: Where’s the $69B behind Tether’s coin.

What People Are Saying

About

After years of self-education, strategy development, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Additionally, Capelj is a finance and technology reporter. Some of his biggest works include interviews with leaders such as John Chambers, founder and CEO, JC2 Ventures, Kevin O’Leary, businessman and Shark Tank host, Catherine Wood, CEO and CIO, ARK Invest, among others.

Disclaimer

At this time, Physik Invest does not manage outside capital and is not licensed. In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.