Market Commentary

Equity index futures, commodities, and bonds trade sideways to lower.

- Fed action, debt ceiling fear mounting.

- Ahead: ADP Employment, Fed speak.

- Indices position for directional resolve.

What Happened: U.S. stock index futures auctioned sideways to lower overnight alongside narratives surrounding adjustments to monetary policy and debt ceiling complications.

Ahead is data on ADP employment (8:15 AM ET) and Fed speak (9:00 and 11:30 AM ET).

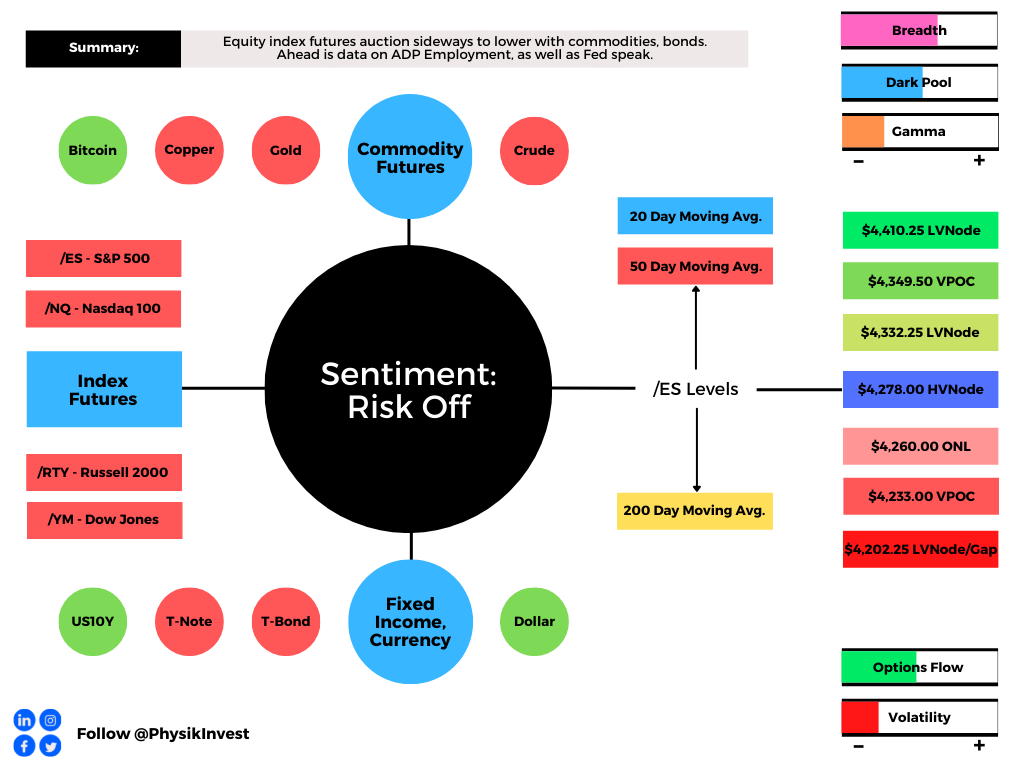

What To Expect: As of 6:30 AM ET, Wednesday’s regular session (9:30 AM – 4:00 PM EST) in the S&P 500 will likely open outside of prior-range and -value, suggesting an increased potential for immediate directional opportunity.

Adding, during the prior day’s regular trade, on positive albeit weak intraday breadth and divergent market liquidity metrics, the best case outcome occurred, evidenced by trade up to $4,358.00, the level of a key anchored volume-weighted average price (VWAP).

Thereafter, equity index futures, led by the Nasdaq 100 and Russell 2000, liquidated overnight, leaving behind Tuesday’s prominent point of control (POC) before finding responsive buyers at a key high volume area (HVNode) for this most recent developing balance area (between the $4,363.25 and $4,278.00 HVNodes).

This trade is significant because it marks acceptance, or a willingness to transact at lower prices. We’re carrying forward, though, the presence of poor structures (e.g., Friday’s advance away from session value on a taper of volume, and a minimal excess low, suggests a lack of commitment to take prices lower).

Given the overnight gap inside of balance, the following scenarios apply.

Balance-Break Scenarios: A change in the market (i.e., the transition from two-time frame trade, or balance, to one-time frame trade, or trend) may occur. Monitor for acceptance (i.e., more than 1-hour of trade) outside of the balance area. Rejection (i.e., return inside of balance) portends a move to the opposite end of the balance.

Further, the aforementioned trade is happening in the context of a traditionally volatile October, as well as narratives surrounding adjustments to monetary policy and debt ceiling complications.

Despite these themes supporting fear and uncertainty, Marko Kolanovic, JPMorgan’s chief global markets strategist, said the following in a note Monday: “We do not believe the recent bout of de-risking will lead to sustained falls, and maintain the stance to keep buying into any weakness.”

On the other hand, in support of continued volatility, Nordea believes there are “4 macro reasons why 2022 should be noisier than 2021: liquidity, growth slowdown, cost/margin problems and the risk of the Fed put looking very different if inflation indicators stay elevated.”

Prior to yesterday’s advance, this newsletter noted that indices were best positioned for a vicious rebound as near-term downside discovery metrics likely reached a limit.

The overnight liquidation challenges that thesis, putting indexes in a peculiar position; it’s likely that participants are seeking more information to base a directional move.

Moreover, for today, participants may make use of the following frameworks.

In the best case, the S&P 500 trades sideways or higher; activity above the $4,278.00 HVNode puts in play the $4,332.25 low volume area (LVNode). Initiative trade beyond the LVNode could reach as high as $4,349.00 untested POC (VPOC) and $4,410.25 LVNode, or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,278.00 HVNode puts in play the $4,260.00 overnight low (ONL). Initiative trade beyond the ONL could reach as low as $4,233.00 VPOC and $4,202.25 LVNode, or lower.

Definitions

Overnight Rally Highs (Lows): Typically, there is a low historical probability associated with overnight rally-highs (lows) ending the upside (downside) discovery process.

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

Balance (Two-Timeframe Or Bracket): Rotational trade that denotes current prices offer favorable entry and exit. Balance-areas make it easy to spot a change in the market (i.e., the transition from two-time frame trade, or balance, to one-time frame trade, or trend).

Modus operandi is responsive trade (i.e., fade the edges), rather than initiative trade (i.e., play the break).

Excess: A proper end to price discovery; the market travels too far while advertising prices. Responsive, other-timeframe (OTF) participants aggressively enter the market, leaving tails or gaps which denote unfair prices.

More On Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

Rates: Low rates have to potential to increase the present value of future earnings making stocks, especially those that are high growth, more attractive. To note, inflation and rates move inversely to each other. Low rates stimulate demand for loans (i.e., borrowing money is more attractive). In conjunction with the rapid recovery, lower rates solicit hawkish commentary as policymakers look to inhibit inflation.

News And Analysis

‘Volmageddon’ history as SEC greenlights leveraged VIX ETFs.

World trade rebounds at a faster clip than was initially expected.

Treasuries’ pain deepened amid the grimmest year since 2013.

European gas surges 60% in two days as EU sounds the alarm.

Unrelenting political brinkmanship edging U.S. closer to default.

What People Are Saying

About

After years of self-education, strategy development, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Additionally, Capelj is a finance and technology reporter. Some of his biggest works include interviews with leaders such as John Chambers, founder and CEO, JC2 Ventures, Kevin O’Leary, businessman and Shark Tank host, Catherine Wood, CEO and CIO, ARK Invest, among others.

Disclaimer

At this time, Physik Invest does not manage outside capital and is not licensed. In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.