Editor’s Note: The Daily Brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 200+ that read this report daily, below!

What Happened

Overnight, equity index futures added to losses after news that Russia invaded Ukraine.

The MOEX Russia Index fell nearly 50% while, at home in the U.S., equity index futures were off about 3%. Bonds rose with commodities which were led by crude oil (up ~9%).

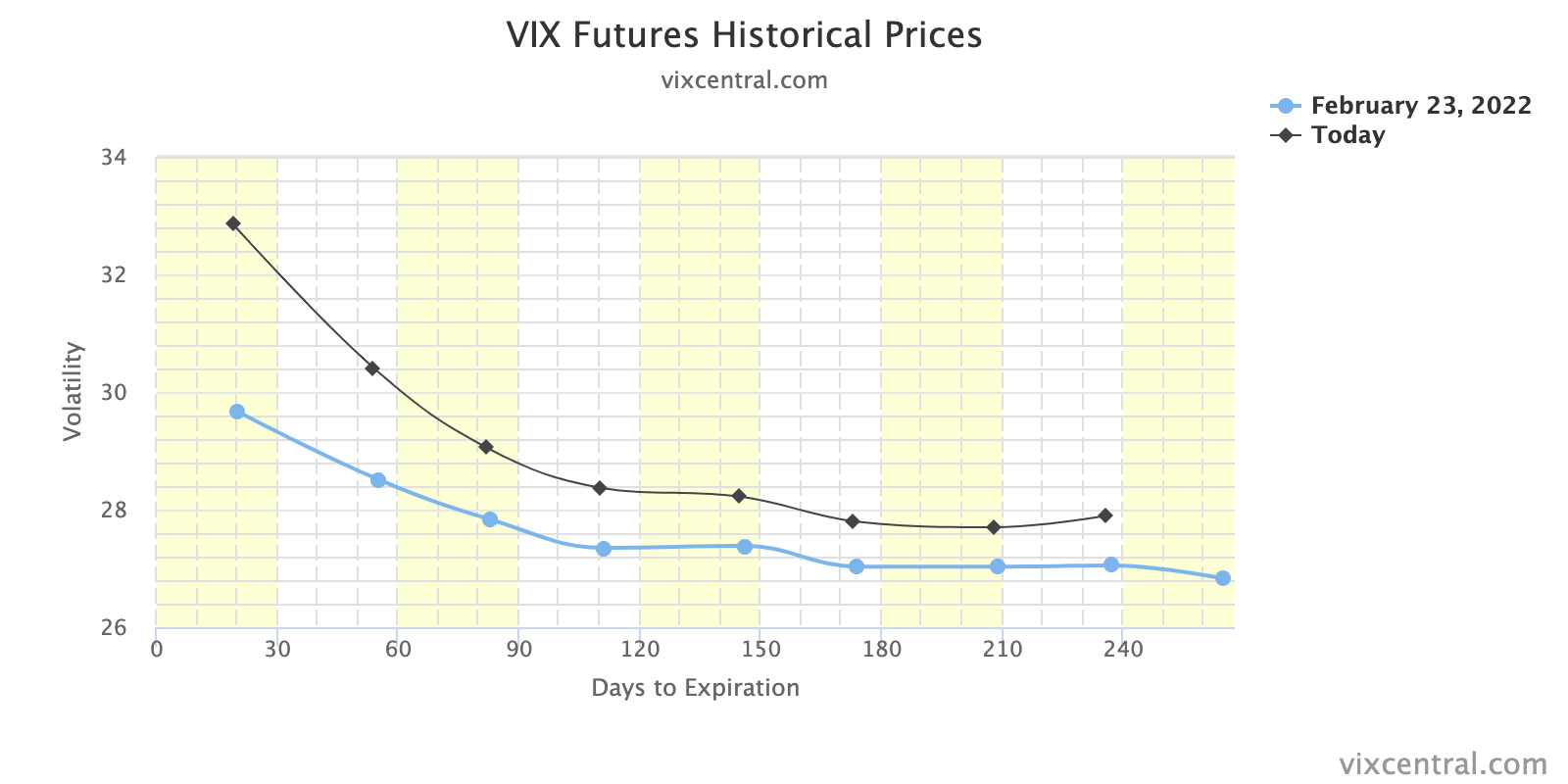

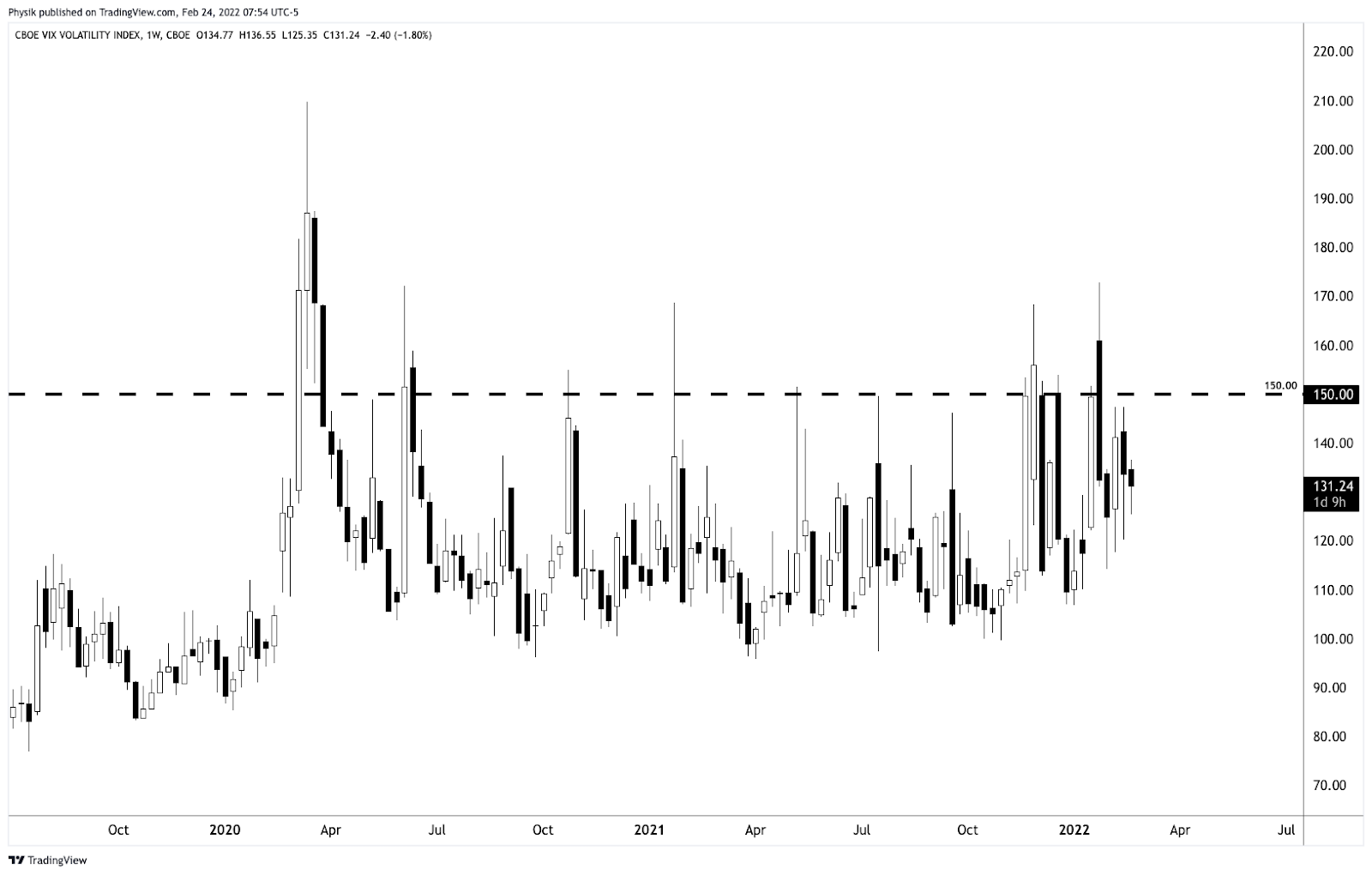

The CBOE Volatility Index (INDEX: VIX), a measure of implied volatility or participants’ forecast of likely movement in prices, printed 37.79 a ~7.00 jump from Wednesday.

This high-level context suggests to us the need for patience. Ranges will be wide. Positioning will compound headline-driven moves. Technical analyses will fail. Caution.

Ahead is data on jobless claims, gross domestic product, gross domestic income (8:30 AM ET), as well as new home sales (10:00 AM ET).

What To Expect

Fundamental: “The ‘bad news = good news’ narrative for markets doesn’t work if the Fed is tightening amidst a slowdown and a military escalation risk. In this case, bad news = bad news.”

Pursuant to this remark by Alfonso Peccatiello, Russian equities fell the most on record (nearly 50%) after President Vladimir Putin ordered the demilitarization of Ukraine.

According to Bloomberg, this crisis comes “after the U.S. and its allies crossed Russia’s ‘red lines’ by expanding the NATO alliance.”

In terms of the economic implications of Russia sanctions, it is “Cyprus and eastern European countries [that] are the most reliant on Russian imports in the EU.”

Ukraine’s crisis also throws a wrench at monetary tightening initiatives, abroad; “the European Central Bank will put even greater emphasis on its flexibility and options as it exits stimulus measures and shifts toward raising rates,” Governing Council member Francois Villeroy de Galhau said.

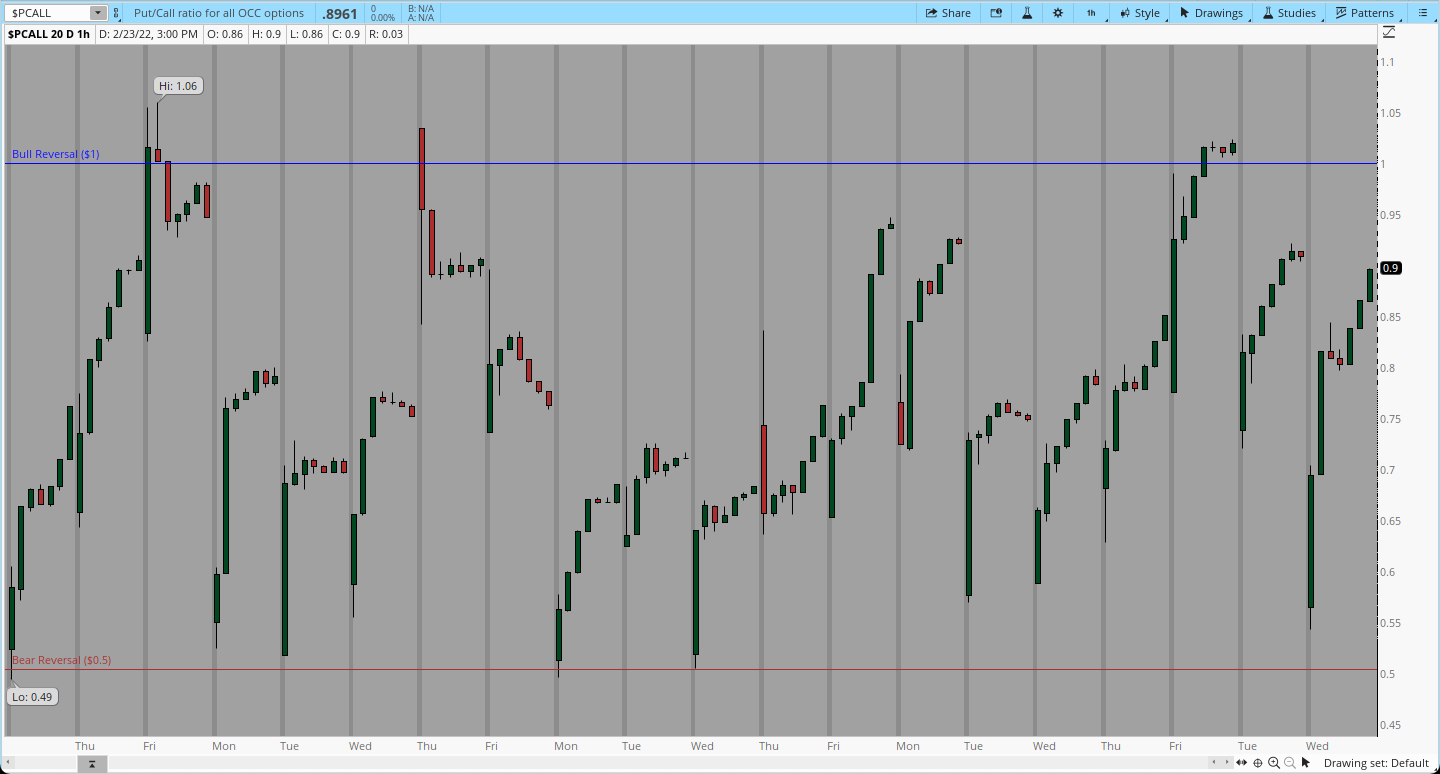

Positioning: Implied volatility expands as heightened demand for protection is priced in.

This comes after, according to views expressed by The Ambrus Group’s Kris Sidial, “we saw larger inflow[s] into equity funds, outflow[s] out of money markets, larger buying in the ATSs, with no real put buying.”

In other words, measures of implied volatility were not performing; participants opportunistically buying the dip witnessed an SPX down, VIX down environment in which hedges were not being marked up accordingly.

The implications of this action are staggering.

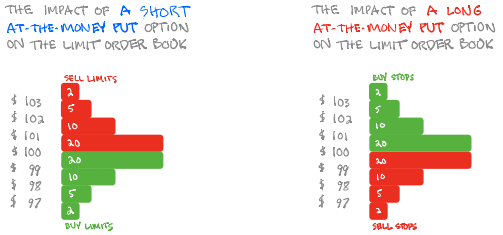

As stated yesterday, as most participants, at least at the index level, own protection, the counterparties to this trade are short protection.

These counterparties, therefore, have positive exposure to delta (i.e., as index falls [rises], position loses [makes] money) and negative exposure to gamma, or delta (directional) sensitivity to underlying price changes (i.e., as the index moves against short option exposure, losses are multiplied).

With measures of implied volatility expanding, as is the case when there is heightened demand for downside put protection, protection is bid and the dealer’s exposure to positive delta rises, which solicits more selling in the underlying (addition of short-delta hedges).

To monitor for capitulation, we may look for when the volatility expectations of implied volatility metrics rise to extremes. Learn more about VVIX, here.

We may also measure for one-sidedness in sentiment by looking to naive metrics like the put/call ratio. Learn more about PCALL, here.

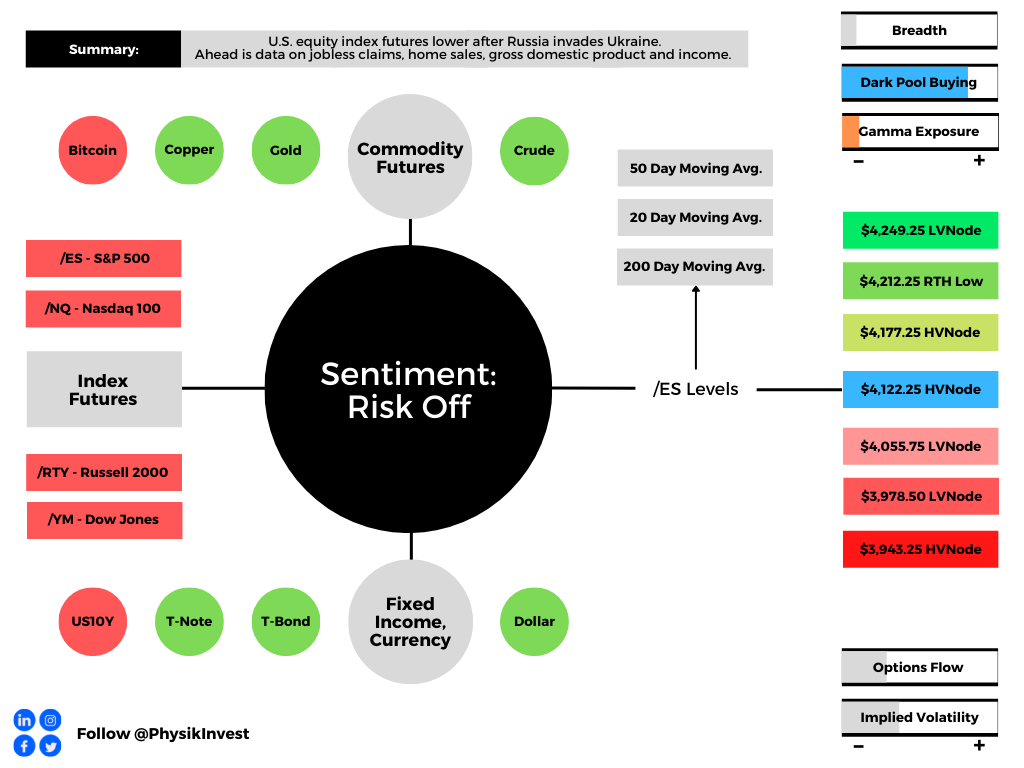

Technical: As of 6:30 AM ET, Thursday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the lower part of a negatively skewed overnight inventory, outside of prior-range and -value, suggesting a potential for immediate directional opportunity.

Gap Scenarios: Gaps ought to fill quickly. Should they not, that’s a signal of strength; do not fade. Leaving value behind on a gap-fill or failing to fill a gap (i.e., remaining outside of the prior session’s range) is a go-with indicator. Auctioning and spending at least 1-hour of trade back in the prior range suggests a lack of conviction; in such a case, do not follow the direction of the most recent initiative activity.

In the best case, the S&P 500 trades higher; activity above the $4,122.25 high volume area (HVNode) puts in play the $4,177.25 HVNode. Initiative trade beyond the HVNodes could reach as high as the $4,212.25 regular trade low (RTH Low) and $4,249.25 low volume area (LVNode), or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,122.25 HVNode puts in play the $4,055.75 LVNode. Initiative trade beyond the latter could reach as low as the $3,978.50 LVNode and $3,943.25 HVNode, or lower.

Considerations: If you are not well-versed in navigating trade at heightened levels of volatility, it is best to sit on your hands (SOH) or trade with a smaller size. Often, on large gaps, indexes may move sideways (and not up or down). This can be frustrating. Also, in high volatility, negative-gamma environments, headlines matter, and technical analyses often fail. Do not think “this time is as others” and let this event lead to your demise. Caution. Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

What People Are Saying

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj is also a Benzinga finance and technology reporter interviewing the likes of Shark Tank’s Kevin O’Leary, JC2 Ventures’ John Chambers, FTX’s Sam Bankman-Fried, and ARK Invest’s Catherine Wood, as well as a SpotGamma contributor developing insights around impactful options market dynamics.

Disclaimer

Physik Invest does not carry the right to provide advice.

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.