What Happened

Overnight, equity index futures were sideways alongside the narrative that a strengthening dollar and the need to counteract inflation may endanger the rally in risk assets.

Ahead is data on the Chicago Fed National Activity Index (8:30 AM ET) and Existing Home Sales (10:00 AM ET).

What To Expect

To start, on weak intraday breadth and supportive market liquidity metrics, the best case outcome occurred, evidenced by the balance and overlap of value areas in the S&P 500.

Taken together, the activity of the past two weeks or so signals participants’ willingness to position for directional resolve (i.e., trend) in the face of new information, and the like.

Context: The aforementioned trade is happening in the context of concerns over peak liquidity and prevailing monetary frameworks.

Specifically, as Bloomberg’s John Authers put it, the abundance of global liquidity, that stoked one of the best stock market recoveries in history, is in peril by the strengthening of the dollar and the need to counter inflationary pressures.

“Obstinately low real yields help to explain why the threat to liquidity has as yet had minimal effect on the stock market. Higher real yields are the shoe that hasn’t dropped this year; investors need a clear plan of evasive action for such an eventuality. For now, liquidity, liquidity, liquidity is still keeping stocks going up, up, up.”

Some of this fear around monetary evolution, so to speak, though, has yet to feed into the pricing of equity market risk. Fear in one market tends to feed into the fear of another.

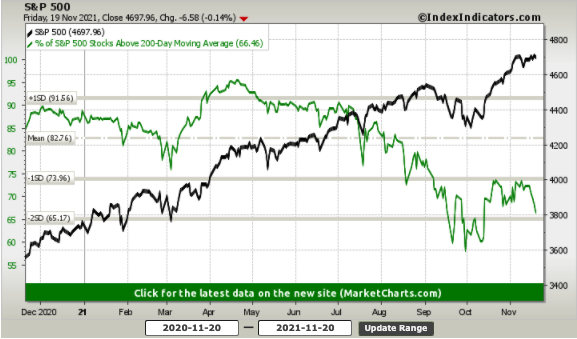

At the same time, we see a divergence in breadth.

The takeaway here is that the SPX is sideways to higher while many of its constituents seem to not be participating in the most recent round of markup.

What factors are to blame for this? Two include an all-time high in buybacks, as well as extremes in speculation and upside volatility in heavily-weighted index constituents.

Adding, the S&P 500 closing last week pinned to the level at which dealers (i.e., those participants that take the other side of options trades and warehouse risk) exposure to positive options gamma was highest.

Note that I talk about the implications options so much due to increased use and impact on underlying price, as a result of associated hedging.

The aforementioned explains why the S&P can’t move; “If dealer hedging has suppressed index level volatility, but underlying components are still exhibiting idiosyncratic volatility, then the only reconciliation is a decline in correlation,” according to one paper by Newfound Research.

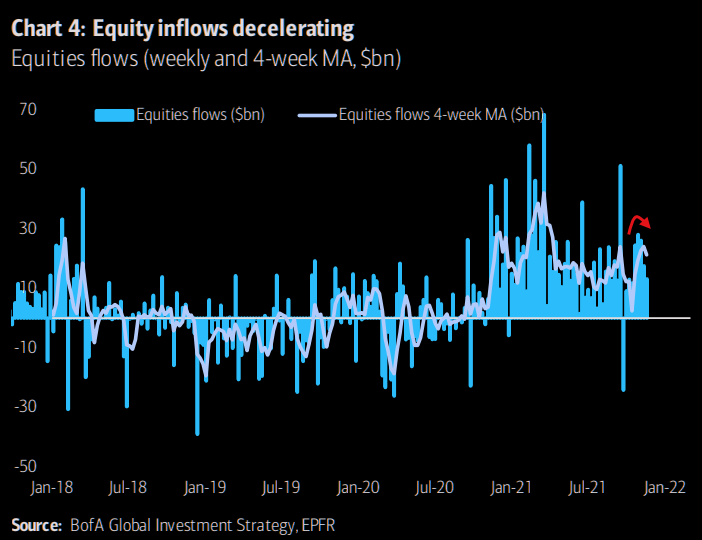

So trash breadth and a deceleration in equity inflows, coupled with exuberance (and upside volatility in heavily weighted index constituents) and clustered options positioning over the past weeks, is part of the reason why indices are sideways. Yes, to some extent.

The tone is to change, soon.

After OPEX, the absence of supportive vanna and charm flows (defined below), for which we can attribute some of the trends in extended day outperformance, alongside that sticky gamma hedging, so to speak, frees the market for directional resolve.

According to SpotGamma, in light of recent exuberance, “participants are underexposed to downside put protection. Should these participants reach for long-gamma put exposures amidst volatility, there is a potential for a destabilizing, reflexive reaction on the part of dealers.”

The reason is, as volatility rises and customers demand out-of-the-money put protection, counterparties are to hedge by selling stock and futures into weakness.

Cognizant of the risks, though, I end this section with the following.

“[D]uring the 12-month period starting six months before and ending six months after a tightening cycle begins, the valuation of the S&P 500 has on average remained remarkably steady,” according to a post by The Market Ear.

At the same time, seasonality is great as, according to Callum Thomas, “Historically most of the time if the market closed up 20%+ for the year, the next year was also positive (84% of the time). As of writing, the market is up some 27% YTD (albeit, this year ain’t over yet!).”

Going forward, we shall monitor for the first signs of instability via spikes in the CBOE Volatility-Of-Volatility Index (INDEX: VVIX) and upward shifts in the VIX futures term structure.

Expectations: As of 6:20 AM ET, Monday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the upper part of a positively skewed overnight inventory, inside of prior-range, suggesting a limited potential for immediate directional opportunity.

Balance-Break Scenarios: A change in the market (i.e., the transition from two-time frame trade, or balance, to one-time frame trade, or trend) may occur. We monitor for acceptance (i.e., more than 1-hour of trade) outside of the balance area. Rejection (i.e., return inside of balance) portends a move to the opposite end of the balance. Given the passage of OPEX, we ought to give more weight to directional resolve (i.e., trend).

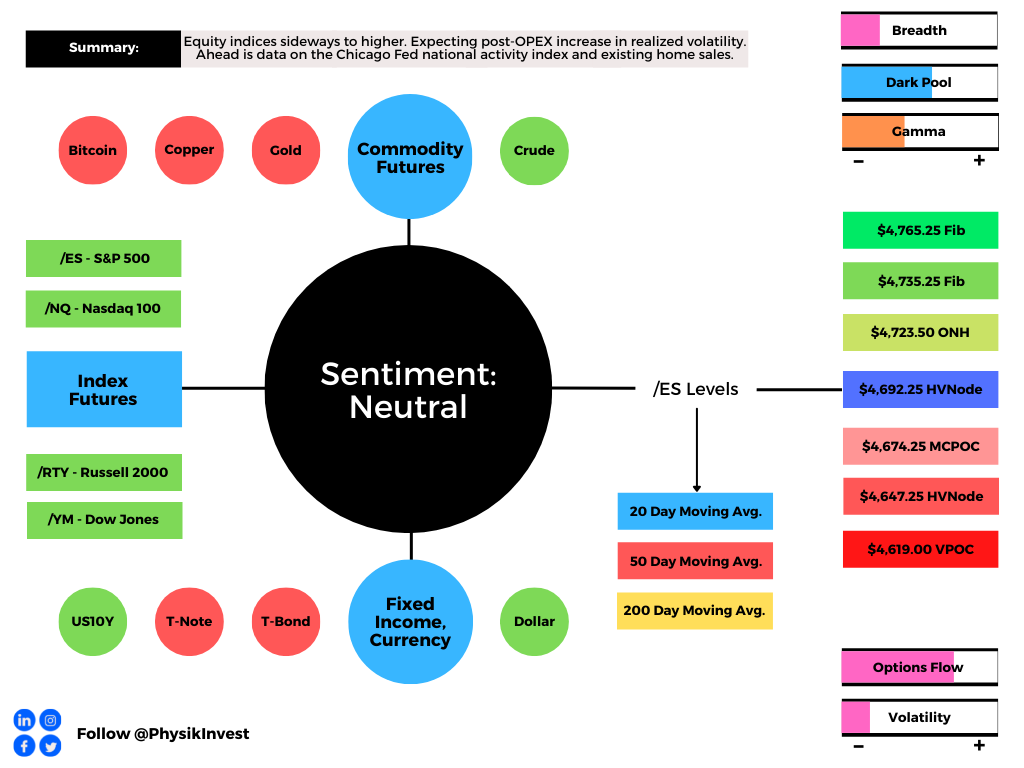

In the best case, the S&P 500 trades sideways or higher; activity above the $4,692.25 high volume area (HVNode) puts in play the $4,723.50 overnight high (ONH). Initiative trade beyond the ONH could reach as high as the $4,735.25 and $4,765.25 Fibonacci, or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,692.25 HVNode puts in play the $4,674.25 micro composite point of control (MCPOC). Initiative trade beyond the MCPOC could reach as low as the $4,647.25 HVNode and $4,619.00 VPOC, or lower.

Click here to load today’s updated key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Definitions

Overnight Rally Highs (Lows): Typically, there is a low historical probability associated with overnight rally-highs (lows) ending the upside (downside) discovery process.

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

Gamma: Gamma is the sensitivity of an option to changes in the underlying price. Dealers that take the other side of options trades hedge their exposure to risk by buying and selling the underlying. When dealers are short-gamma, they hedge by buying into strength and selling into weakness. When dealers are long-gamma, they hedge by selling into strength and buying into weakness. The former exacerbates volatility. The latter calms volatility.

Vanna: The rate at which the delta of an option changes with respect to volatility.

Charm: The rate at which the delta of an option changes with respect to time.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

About

After years of self-education, strategy development, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Additionally, Capelj is a Benzinga finance and technology reporter interviewing the likes of Shark Tank’s Kevin O’Leary, JC2 Ventures’ John Chambers, and ARK Invest’s Catherine Wood, as well as a SpotGamma contributor, developing insights around impactful options market dynamics.

Disclaimer

At this time, Physik Invest does not manage outside capital and is not licensed. In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.