Although banks’ earnings were better than anticipated, sone figures indicate that the broader economy is declining, as retail sales and manufacturing output fell more than projected. Despite the challenges, most believe the Federal Reserve will raise interest rates next month.

Loretta Mester of the Federal Reserve, explained there should be another rate hike as the monetary policy will need to be more restrictive this year, with the fed funds rate rising above 5% and the real fed funds rate remaining positive for an extended period.

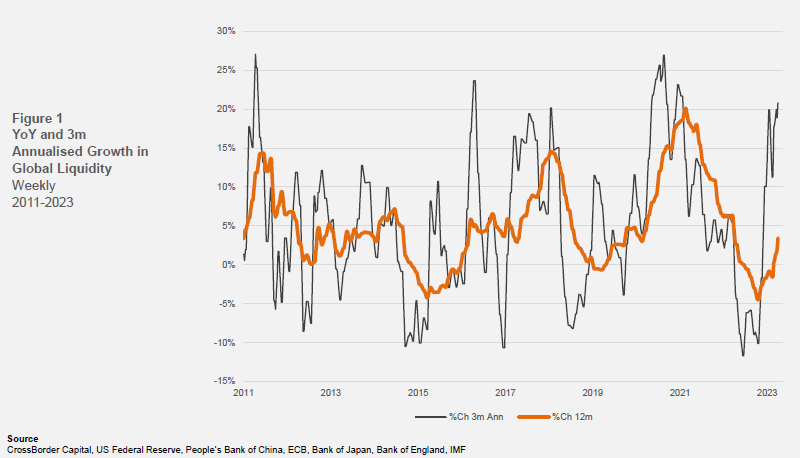

Thus far, monetary policymakers’ efforts to work liquidity out of the system have been complicated, particularly with rates at the back end falling, said Kai Volatility’s Cem Karsan in a conversation with TD Ameritrade Network. CrossBorder Capital confirms. Liquidity has been on an upward trend since October, partly due to China’s efforts to recover from Covid-19 restrictions and the collapse of the UK gilts markets.

Graphic: Retrieved from CrossBorder Capital via Bloomberg.

“Our original conjecture that Central Banks have effectively split their policy tools to use quantitative or balance sheet policies (QE) to ensure financial stability, whilst targeting inflation with interest rate policy is becoming more widely discussed in the media,” CrossBorder Capital’s Mike Howell said. “This splitting of roles can explain why interest rates have risen at the same time that Global Liquidity is turning higher.”

Accordingly, with the recent response to the bank issues cutting down tail risks for the S&P 500 (INDEX: SPX), markets are positioned to stay contained with falling implied volatility (IVOL) and correlations, as well as the passage of time, positioning-wise, key market boosters, Karsan added.

It’s appears the SPX may strengthen before it weakens with risk indicators, including IVOL measures, rising with the SPX. Physik Invest agrees: buy call structures on any weakness and monetize them into strength to finance long dated put structures.

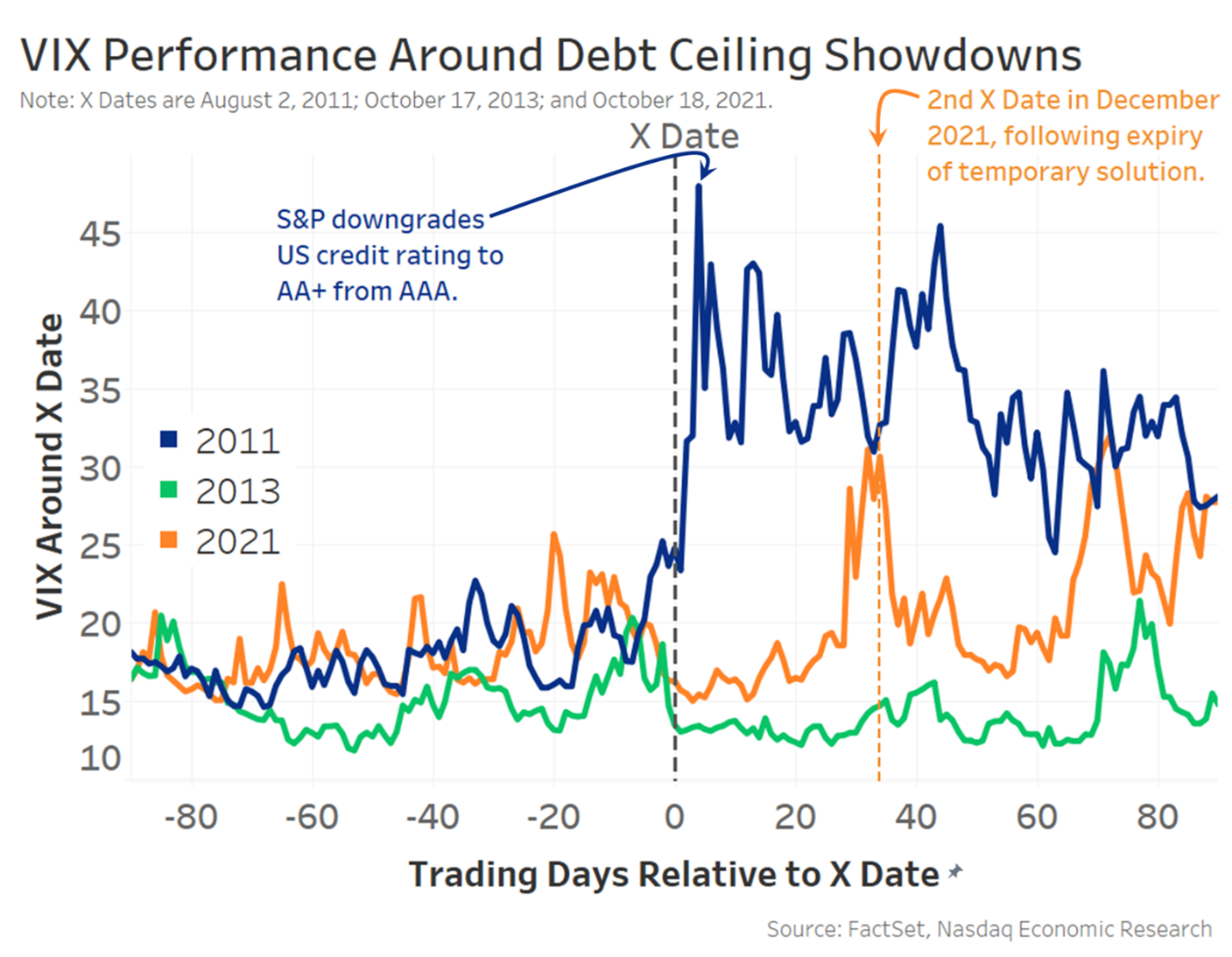

It is better for traders to limit their expectations and stay the course, despite the big gap between IVOL measures like the Cboe Volatility Index and Merrill Lynch Option Volatility Estimate or MOVE, and big bets on market movement in the VIX complex, potentially to hedge against the breach of the US debt limit as soon as June.

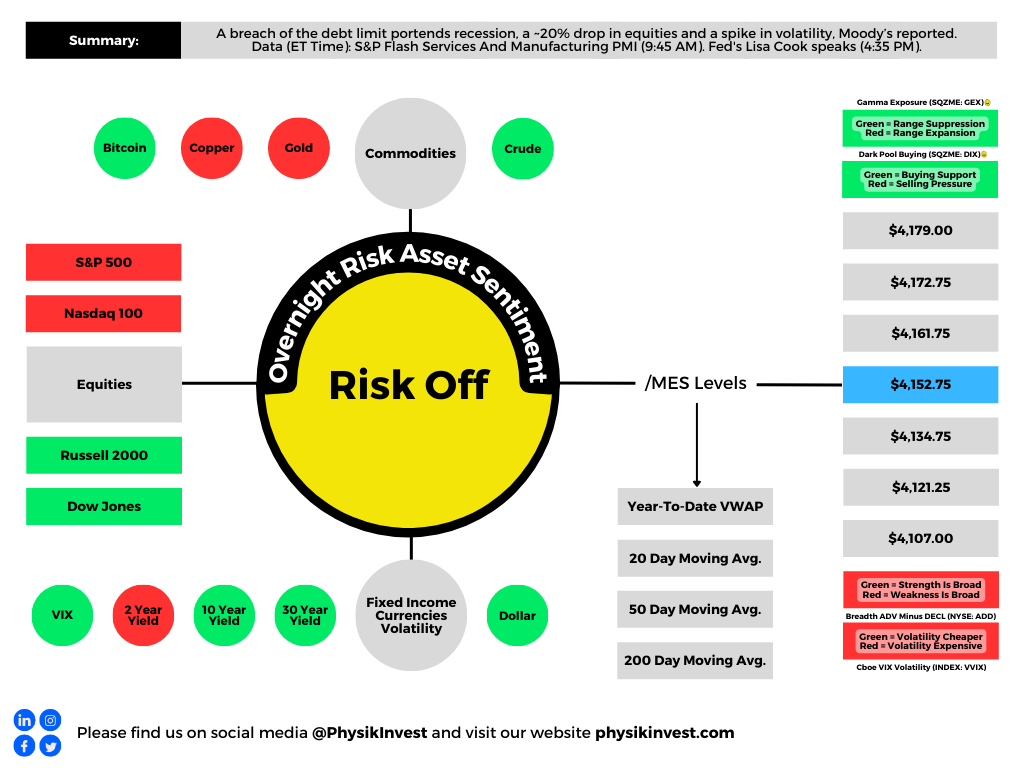

As an aside, recent VIX hedging makes sense given that a breach of the debt limit likely results in recession, a ~20% drop in equities, and a volatility spike, Moody’s said.

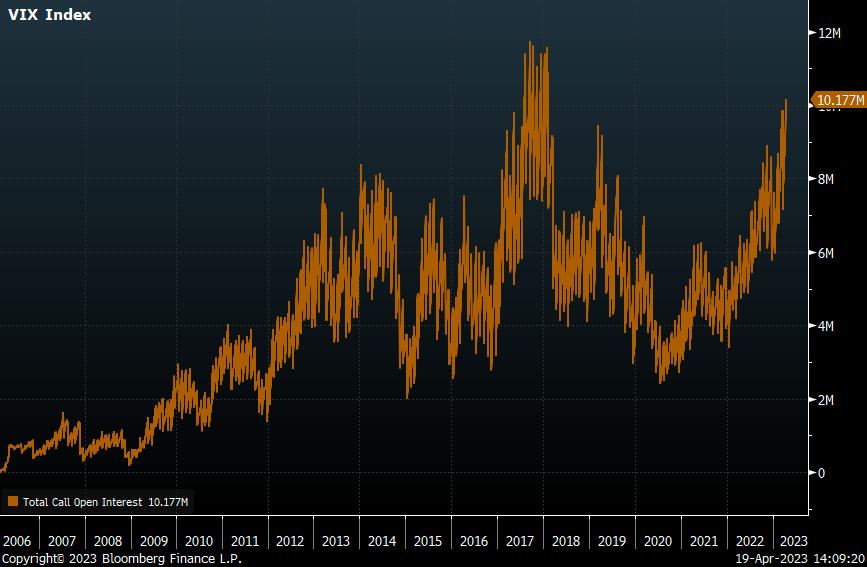

Graphic: Retrieved from Nasdaq Inc (NASDAQ: NDAQ).

Quoting The Ambrus Group’s Kris Sidial, “When volatility starts to move, it moves at a higher rate than S&P volatility which is something that’s really important for the call option buyers,” which are stepping in aggressively as we’ve shown in the past letters.

Graphic: Retrieved from Piper Sandler Companies’ (NYSE: PIPR) Danny Kirsch. “With $VIX sitting at lowest level since early 2022, VIX call open interest approaching all-time highs reached in 2017/2018.”

About

Welcome to the Daily Brief by Physik Invest, a soon-to-launch research, consulting, trading, and asset management solutions provider. Learn about our origin story here, and consider subscribing for daily updates on the critical contexts that could lend to future market movement.

Separately, please don’t use this free letter as advice; all content is for informational purposes, and derivatives carry a substantial risk of loss. At this time, Capelj and Physik Invest, non-professional advisors, will never solicit others for capital or collect fees and disbursements. Separately, you may view this letter’s content calendar at this link.

Welcome to the Daily Brief by Physik Invest. Learn about our origin story here, and consider subscribing for free daily updates on the most important market updates.

We keep recent letters brief as a lengthy one is still being written. Thank you for being so patient.

The Job Openings and Labor Turnover Survey showed a decrease in job vacancies and a tightening of the labor market; vacancies per job-seeker have reduced by 20%, and workers are in a weaker position to bargain.

Accordingly, rate expectations dropped ahead of the next Federal Open Market Committee meeting; traders are bidding up the price of equities.

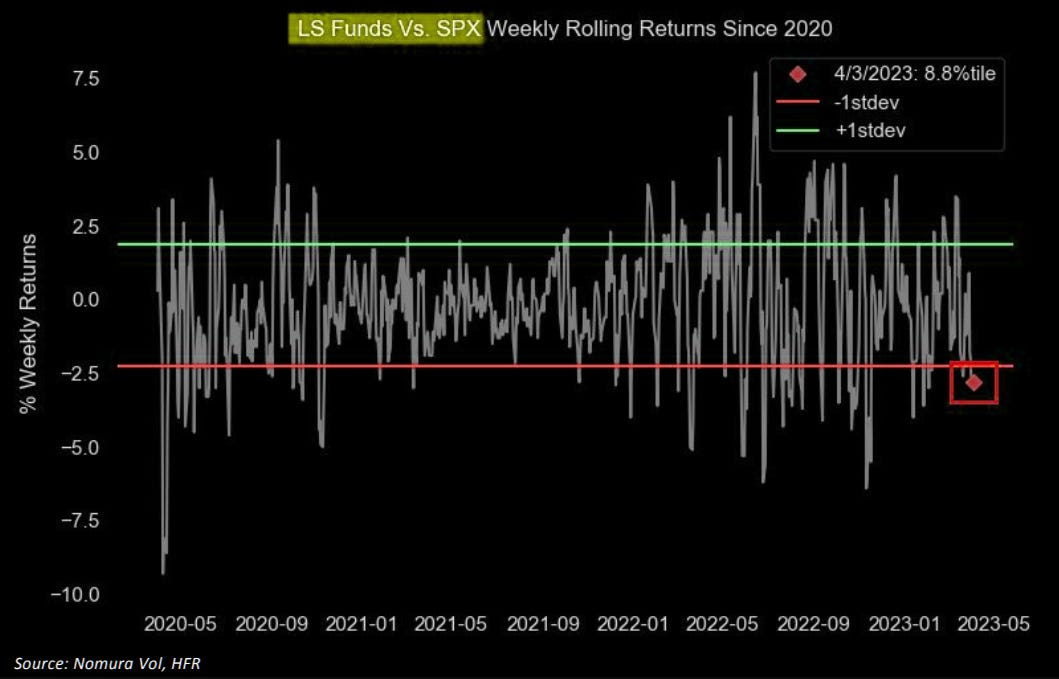

Graphic: Retrieved from Noura Holdings Inc (NYSE: NMR) via The Market Ear. “Long/short vs SPX rolling returns shows you the pain. Nomura’s quant guru McElligott weighs in: ‘…all of last year’s Equities Alpha was in your ‘Short’ books, which were loaded with ‘Expensive / High Multiple / Low Quality / Un-Profitable’ Growth…but that’s now the stuff that is exploding higher on the violent Rates reset LOWER.”

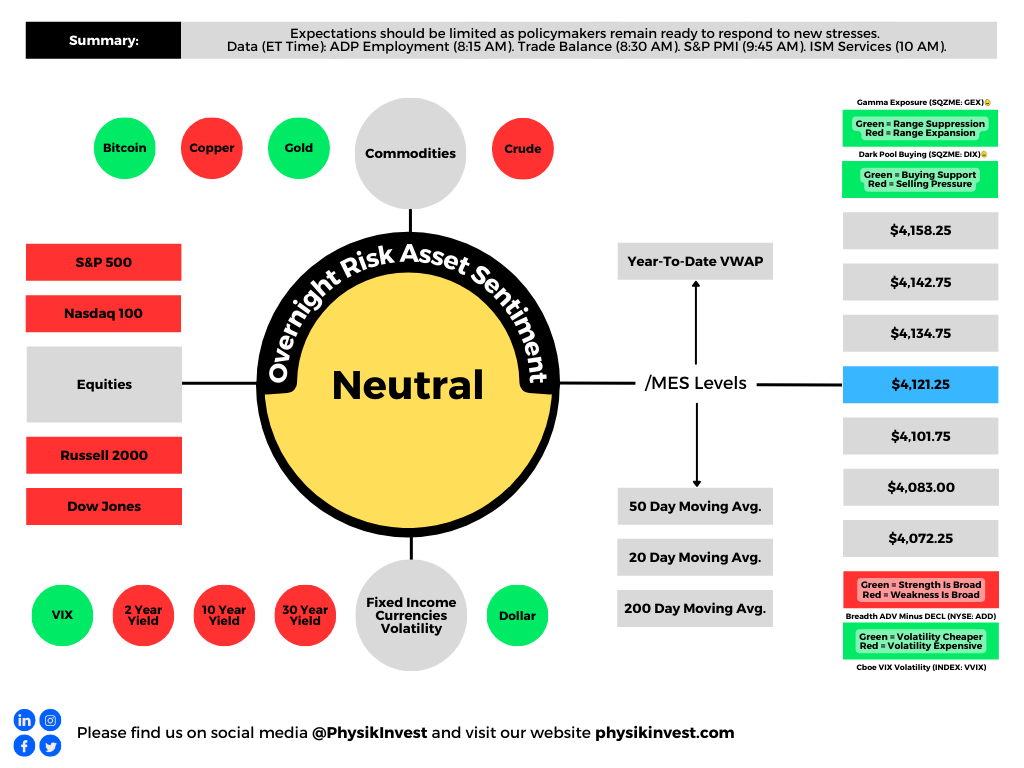

Federal Reserve President Loretta Mester maintained that the benchmark rate should move and stay above 5% to control inflation, adding that no rate cuts may happen this year, barring a significant change in price pressures. Mester said inflation is on its way out – price growth is likely to drop to 3.75% this year and reach 2% by 2025 – and the banking system is sound, though policymakers are ready to respond to new stresses.

A peek at the Secured Overnight Financing Rate or SOFR market shows activity or the consensus centered at the 95.00 options strike (~5%). Per Bloomberg, large positions include a June 95.00/96.00 1×2 call spread, a June 95.75/95.50/95.25/95.00 put condor, and 95.00/94.75/94.50 put flies in both September and December tenors.

From a positioning perspective, this letter maintains the idea of starting to monetizecall structures and rolling profits into fixed-risk bear put spreads. However, given the potential for an underwhelming selloff or “grinding de-leveraging,” keep those debits you pay in check!

To end, the upcoming non-farm payrolls or NFP reportsandinflation figures will provide crucial data on the state of the economy.

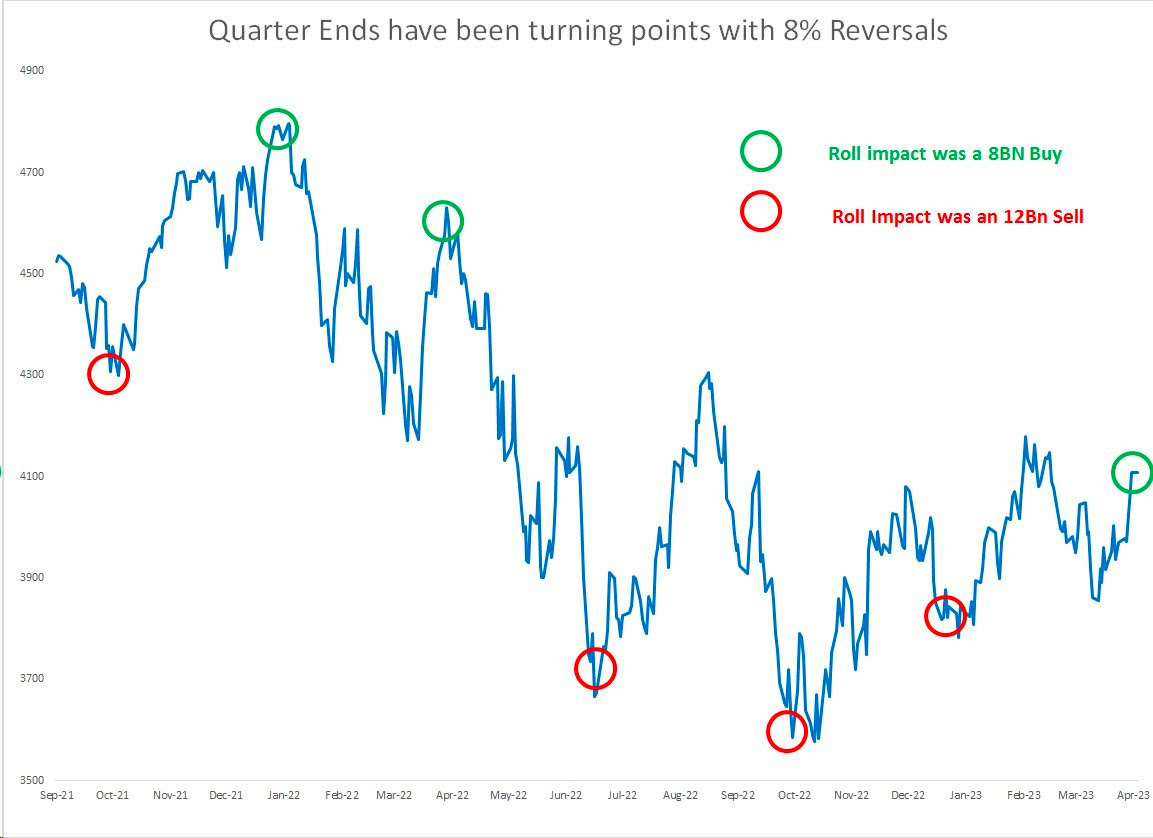

Graphic: Retrieved from Damped Spring Advisors’ Andy Constan. “6 of the last 6 quarters, the quarter end flow has resulted in a spike or dip and a subsequent 8%+ reversal.”

Disclaimer

Don’t use this free letter as advice; all content is for informational purposes, and derivatives carry a substantial risk of loss. At this time, Capelj and Physik Invest, non-professional advisors, will never solicit others for capital or collect fees and disbursements. Separately, you may view this letter’s content calendar at this link.

The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 300+ that read this report daily, below!

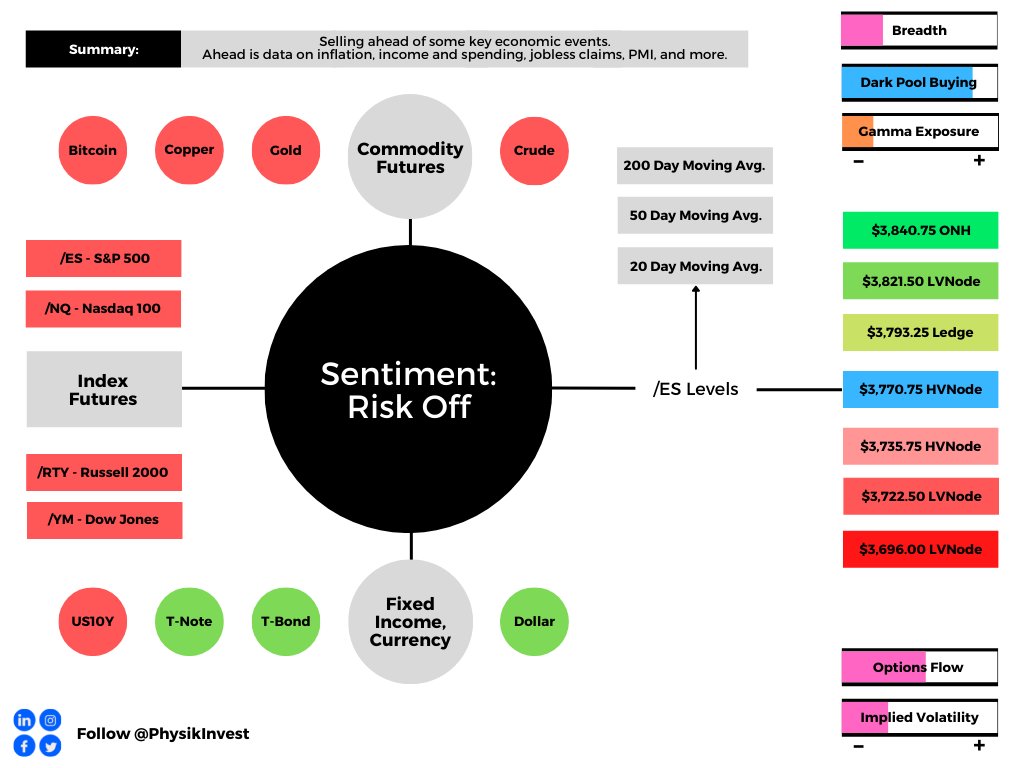

Overnight, equity index and commodity futures auctioned lower while bonds, the dollar, and implied volatility metrics were bid at the tail-end of the quarterly rebalancing period.

Pursuant to this letter’s remarks in the days prior, trades biased long volatility are performing well, particularly those structured a standard deviation and beyond prior prices. We’ll unpack why that is, today.

Ahead is data on PCE inflation, disposable income, and consumer spending, as well as jobless claims (8:30 AM ET) and Chicago PMI (9:45 AM ET).

Graphic updated 6:30 AM ET. Sentiment Risk-Off if expected /ES open is below the prior day’s range. /ES levels are derived from the profile graphic at the bottom of the following section. Levels may have changed since initially quoted; click here for the latest levels. SqueezeMetrics Dark Pool Index (DIX) and Gamma (GEX) calculations are based on where the prior day’s reading falls with respect to the MAX and MIN of all occurrences available. A higher DIX is bullish. At the same time, the lower the GEX, the more (expected) volatility. Learn the implications of volatility, direction, and moneyness. SHIFT data used for S&P 500 (INDEX: SPX) options activity. Note that options flow is sorted by the call premium spent; if more positive, then more was spent on call options. Breadth reflects a reading of the prior day’s NYSE Advance/Decline indicator. VIX reflects a current reading of the CBOE Volatility Index (INDEX: VIX) from 0-100.

What To Expect

Fundamental: Discussed in recent letters were the prospects of whether a recession would be necessary for stemming inflation.

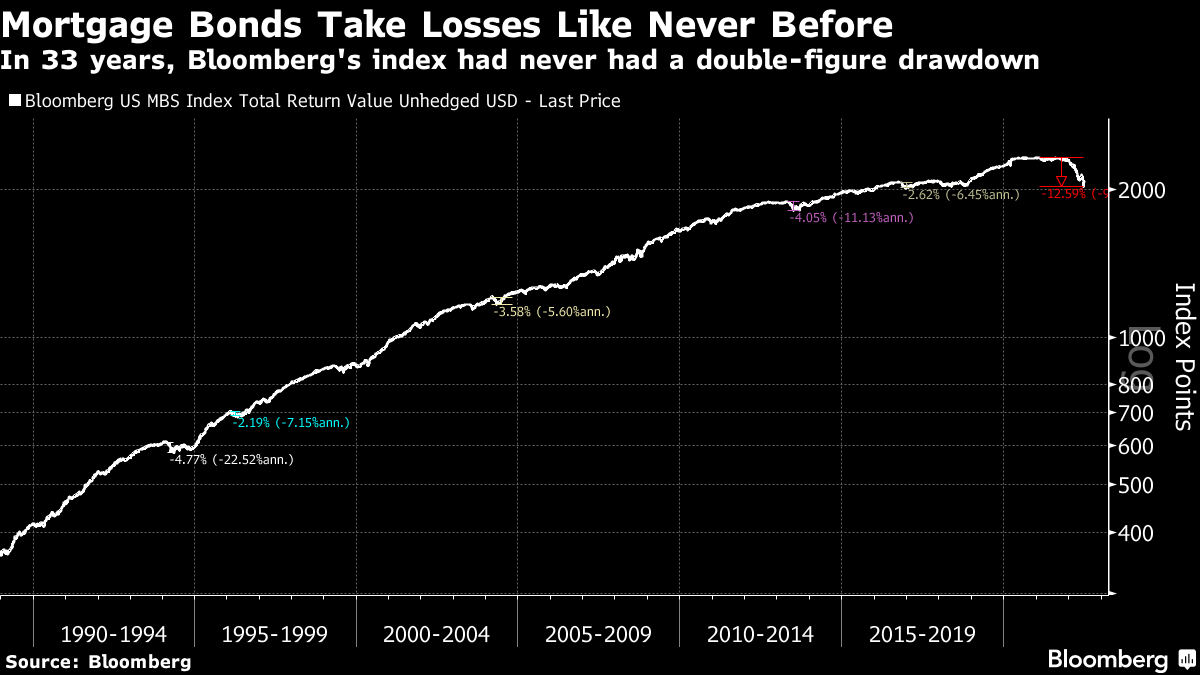

Graphic: Via Bloomberg. “[W]hat’s happened to mortgage-backed bonds this year is a radical departure. Bloomberg’s index dates back to 1988 when the asset class was still in its infancy. This is the first time it has ever withstood a decline that stretches into double figures.”

“That’s the message the market took,” Bloomberg’s John Authers explained. “[T]he most painful surprise over the second half of this year would be for inflation to stay sticky.”

“That would quash the belief in a swift easing campaign in 2023.”

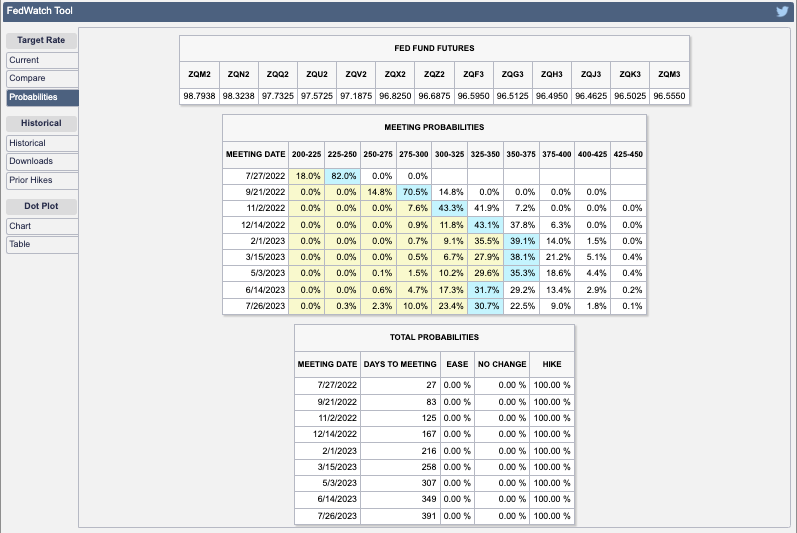

Graphic: CME Group Inc’s (NASDAQ: CME) FedWatch Tool.

Some, like the Federal Reserve’s (Fed) Loretta Mester, suggest that gone are the days to err on the side of being too accommodative.

“It also calls into question the conventional view that monetary policy should always look through supply shocks,” Mester said. “In some circumstances, such shocks could threaten the stability of inflation expectations and would require policy action.”

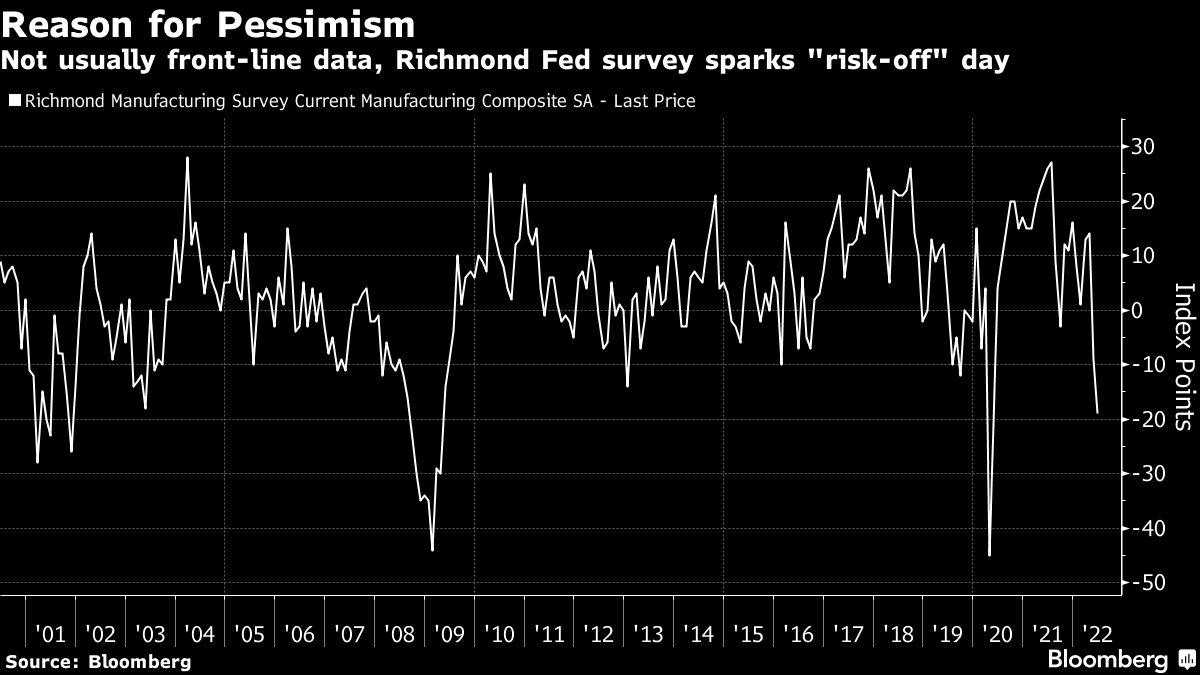

Graphic: Via Bloomberg. “The Richmond Fed’s survey of manufacturing isn’t generally one of the most closely monitored releases, but as this one was the worst since the Great Recession (barring only one month during the Covid shutdown), it garnered more attention than usual.”

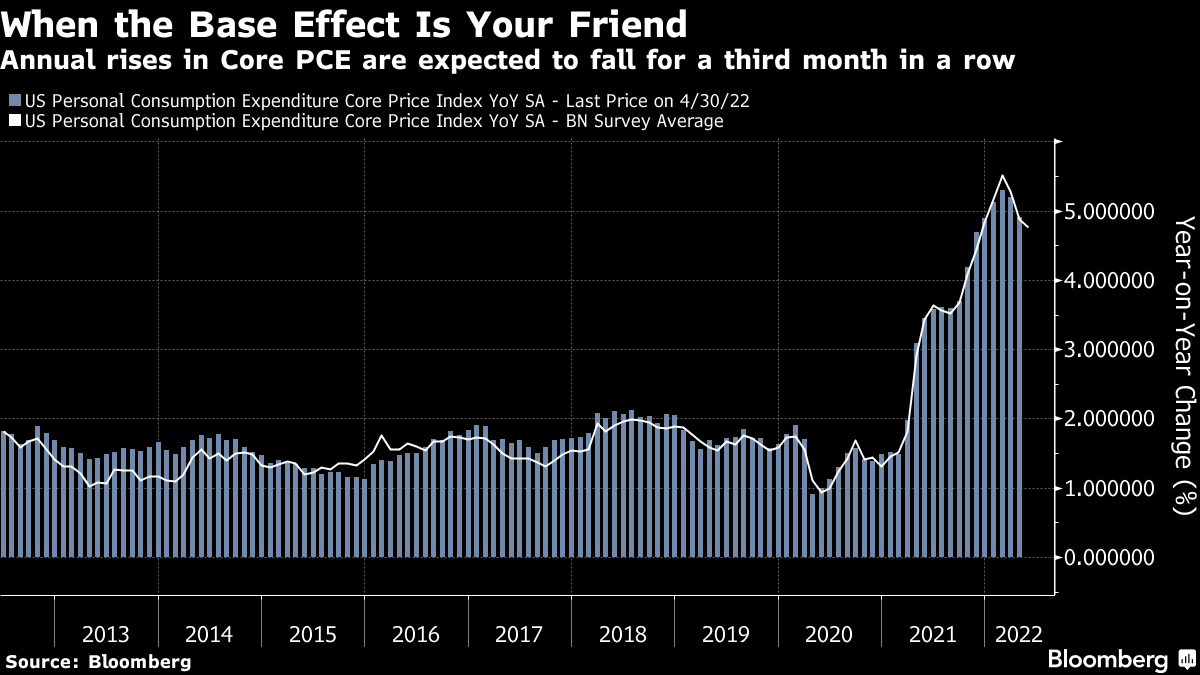

Moreover, the Fed’s preferred inflation measure – the personal consumption expenditure deflator (PCE) – is set to update. The expectation is that core PCE drops, “thanks to base effects from last year,” bolstering the “narrative that inflation will soon be licked.”

Positioning: Discussed, earlier this week, was whether it made sense to lean toward owning volatility, rather than selling it outright.

A “higher starting point” in implied volatility (IVOL), and a still-present right-tail (from the positioning for a bear market rally), made it so we could position, for less cost, in short-dated structures with asymmetric payouts, on both sides of the market.

For instance, S&P 500 (INDEX: SPX) spreads +1 (near-the-money) x -2 (out-of-the-money), in excess of 200 points or so in width and up to 15 days to expiration, are performing well, today, pricing in excess of a 600% gain, only after pricing for little to no cost to enter in the days prior.

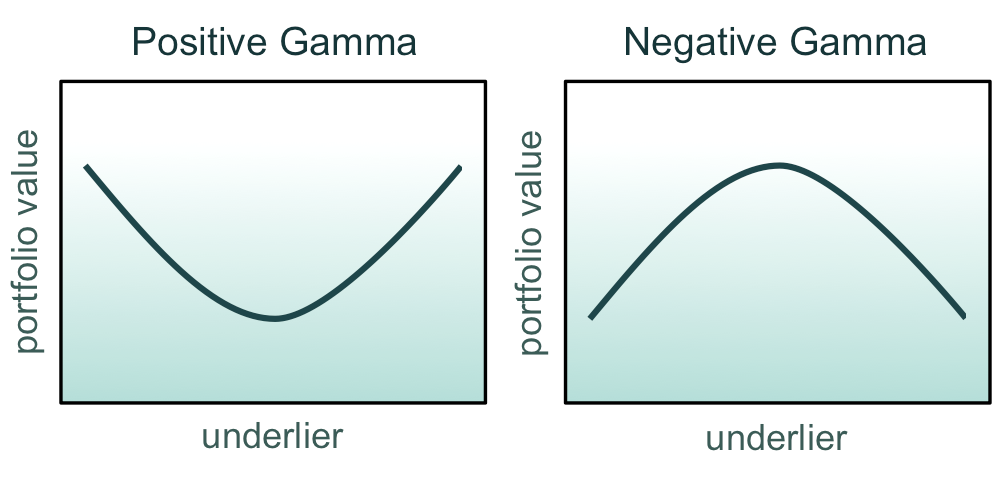

Disclaimer: Have delta in the direction you want the market to move, as well as positive gamma. In our case, we wanted negative delta (short bias) and positive gamma (profits amplified).

Graphic: Via Glyn Holton. “Positive gamma corresponds to curvature that opens upward. Negative gamma corresponds to curvature that opens downward.”

Recent market weaknesses will allow us to monetize and rotate those proceeds into speculative directional bets on the call-side, potentially. After all, the money is made in not losing it. Stay nimble. These are not trade recommendations. Be open-minded.

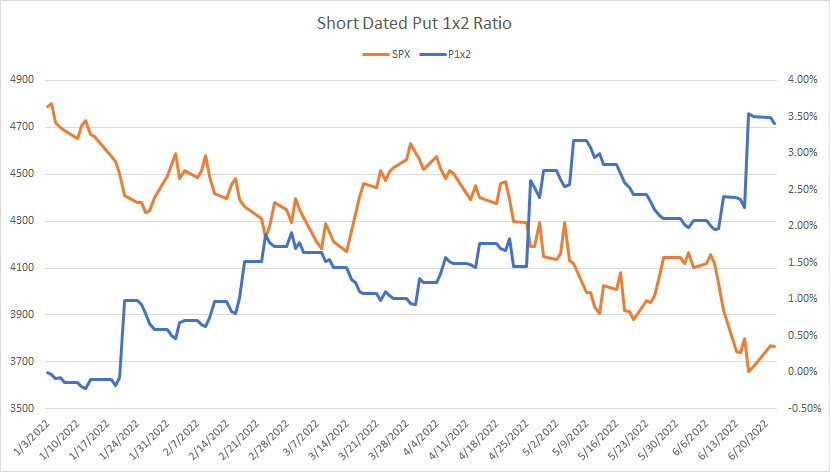

Graphic: Via Pat Hennessy. “[T]he performance of short-dated 1×2 put ratios in SPX this year. Despite being short the tail, the grind lower has been well captured by this trade structure.”

Technical: As of 6:30 AM ET, Thursday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the lower part of a negatively skewed overnight inventory, outside of prior-range and -value, suggesting a potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher; activity above the $3,770.75 HVNode puts in play the $3,793.25 Ledge. Initiative trade beyond the Ledge could reach as high as the $3,821.50 LVNode and $3,840.75 ONH, or higher.

In the worst case, the S&P 500 trades lower; activity below the $3,770.75 HVNode puts in play the $3,735.75 HVNode. Initiative trade beyond the HVNode could reach as low as the $3,722.50 LVNode and $3,696.00 LVNode, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Graphic: 65-minute profile chart of the Micro E-mini S&P 500 Futures.

Considerations: Responsiveness near key-technical areas (that are discernable visually on a chart), suggests technically-driven traders with short time horizons are very active.

Such traders often lack the wherewithal to defend retests and, additionally, the type of trade may be indicative of the other time frame participants waiting for more information to initiate trades.

Definitions

Overnight Rally Highs (Lows): Typically, there is a low historical probability associated with overnight rally-highs (lows) ending the upside (downside) discovery process.

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.