Welcome to the Daily Brief by Physik Invest, a soon-to-launch research, consulting, trading, and asset management solutions provider. Learn about our origin story here, and consider subscribing for daily updates on the critical contexts that could lend to future market movement. Take care, and let’s dig in.

Markets are mixed with equities under light pressure following OPEC+’s surprise oil production cut. It’s likely that Saudi Arabia “realized they were getting played [on the Strategic Petroleum Reserve refill] and took matters into their own hands,” some say.

As a recap, on Friday, measures of inflation abated. Though these measures remain high and support the context for rates to stay high, markets responded positively.

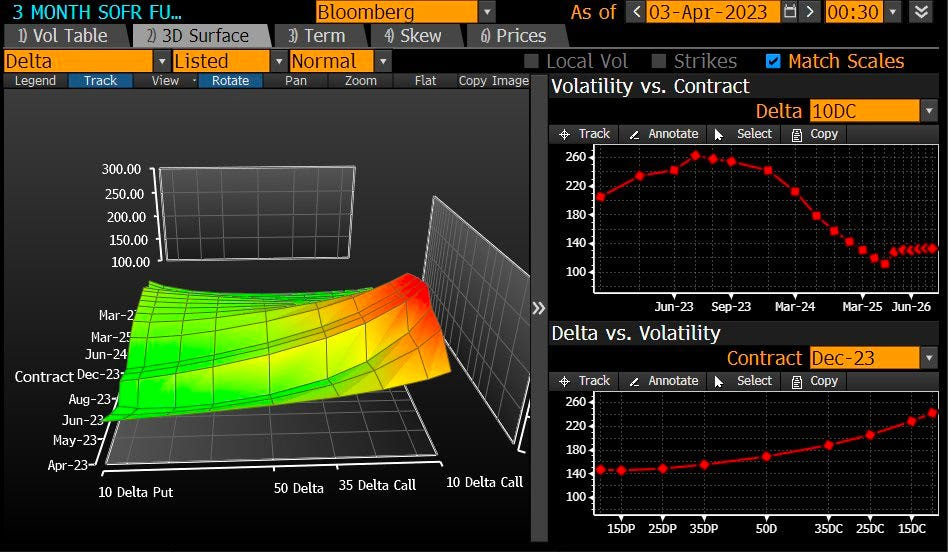

Expectations of interest rate cuts have been pulled forward based on markets like SOFR, correlated to existing money market rates, where traders’ demand for call options (i.e., bet on rates falling) reveals the fear of a heavy rate-cutting cycle.

Graphic: Retrieved from Bloomberg via @countdraghula.

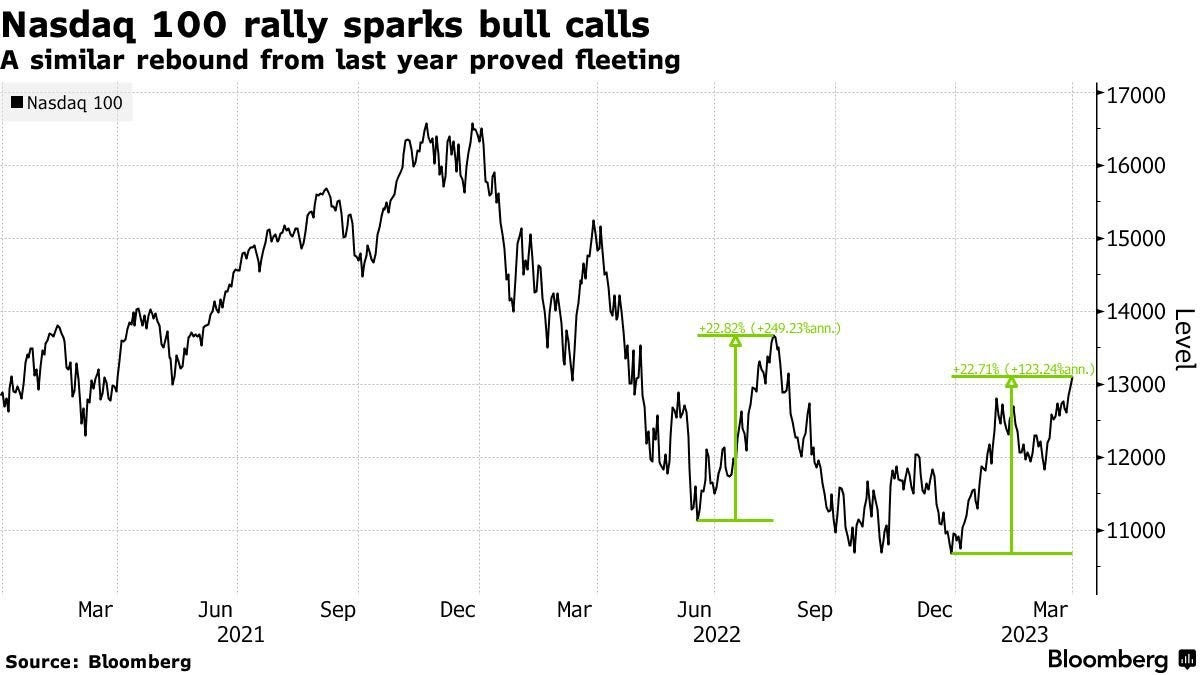

The S&P 500 (INDEX: SPX) closed above $4,100.00 for the first time in months. Many quickly wrote about new bull markets blooming in previously depressed market areas most sensitive to monetary policymakers’ policymaking.

Recall, however, that during the dot-com bust, the Nasdaq 100 (INDEX: NDX) rallied ~20% numerous times before an actual bull market was born. Experts think the same thing is happening; the rally, partly driven by monetary policy expectations and the removal/monetization of downside protection, particularly in markets where traders were most concerned about a de-rate and volatility, is probably in its later stages.

The marginal benefit of any further volatility compression is far less than the cost one may incur by volatility expanding; “there isn’t much juice left to squeeze,” SpotGamma adds, and though short-biased volatility trades (e.g., sell options) could work for a bit longer, the risks remain, as explained on Friday. Rolling profits from the initially low- or no-cost call options structures we discussed last week into fixed-risk debit equity put options structures seem attractive. More to come. Hope you liked the new format!

Disclaimer

Please don’t use this free letter as advice; all content is for informational purposes, and derivatives carry a substantial risk of loss. At this time, Capelj and Physik Invest, non-professional advisors, will never solicit others for capital or collect fees and disbursements. Separately, you may view this letter’s content calendar at this link.

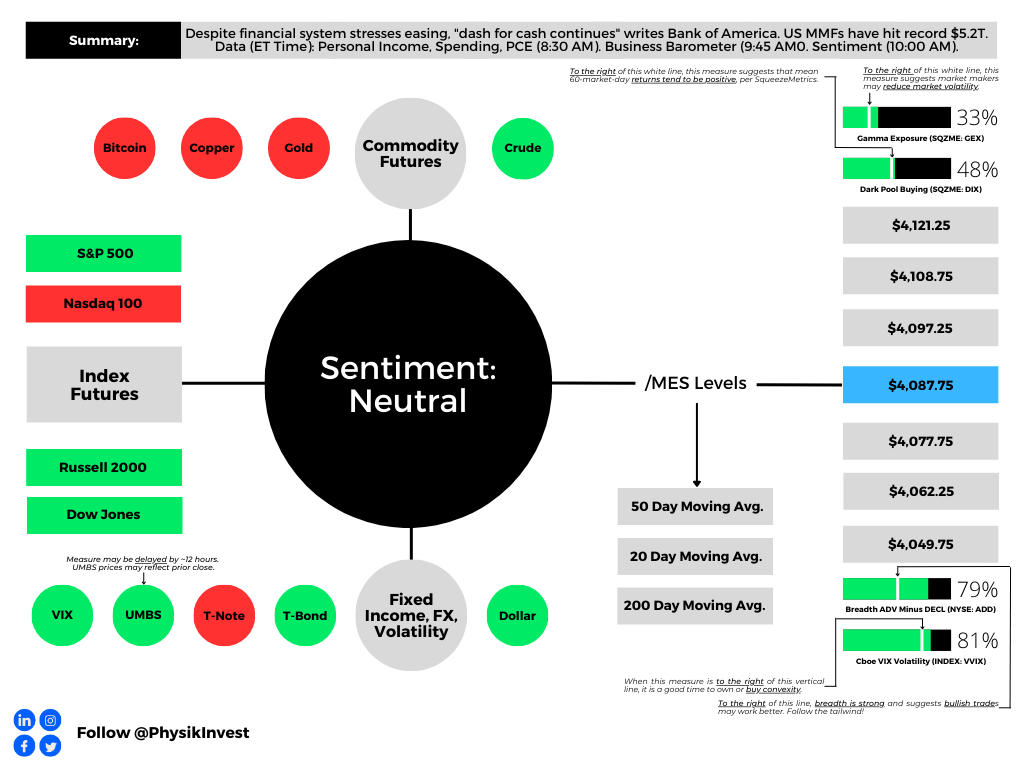

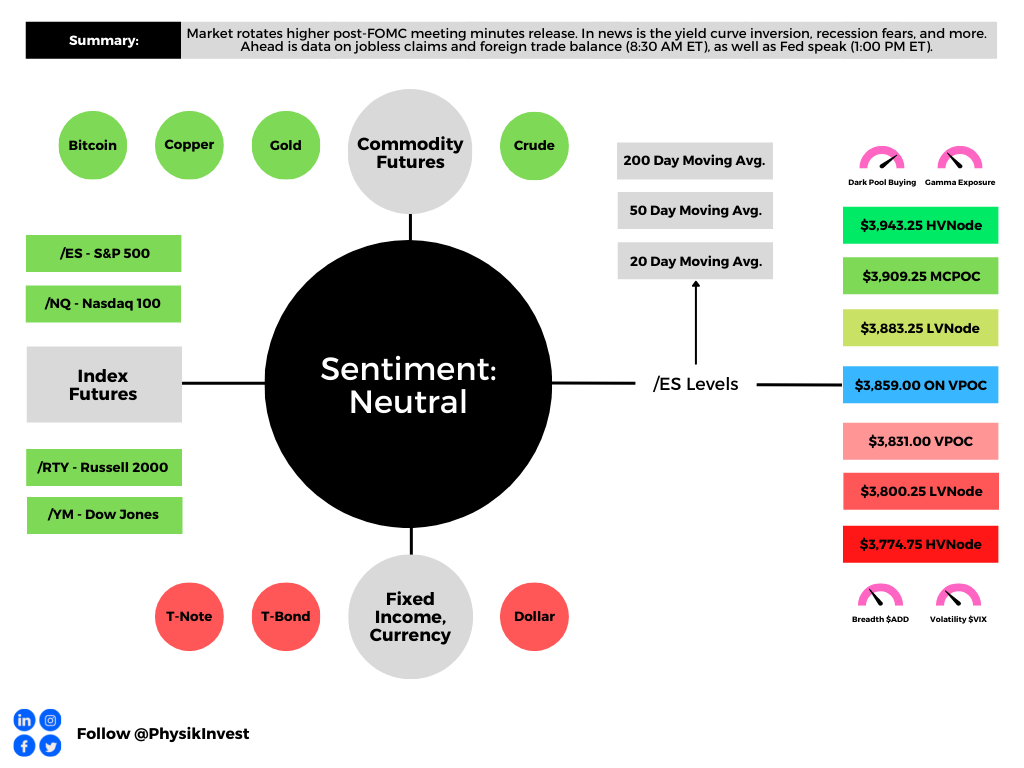

Graphic updated 8:00 AM ET. Sentiment Neutral if expected /MES open is inside of the prior day’s range. /MES levels are derived from the profile graphic at the bottom of this letter. Click here for the latest levels. SqueezeMetrics Dark Pool Index (DIX) and Gamma (GEX) with the latter calculated based on where the prior day’s reading falls with respect to the MAX and MIN of all occurrences available. A higher DIX is bullish. The lower the GEX, the more (expected) volatility. Click to learn the implications of volatility, direction, and moneyness. Breadth reflects a reading of the prior day’s NYSE Advance/Decline indicator. The CBOE VIX Volatility Index (INDEX: VVIX) reflects the attractiveness of owning volatility. UMBS prices via MND. Click here for the economic calendar.

Administrative

Keeping it brief for today. Enjoy your Friday. Be opportunistic and watch your risk.

Positioning

For days prior, top-line measures of implied volatility or IVOL like the Cboe Volatility Index (INDEX: VIX) fell, as did the Cboe VIX Volatility Index (INDEX: VVIX), the latter which is a way to gauge the expensiveness of IVOL or convexity. It was, in part, the resolution of a recent liquidity crisis that prompted this to happen. Under the hood, volatility skew told a different story; traders were hedging against tail outcomes.

Even so, this hedging and volatility skew behavior did little to boost the pricing of most spread structures above and below the market we analyzed. The non-stickiness of IVOL into this rally may have been detrimental to the more expensive call options structures, as we expected; hence, our consistent belief that structures should be kept at low- or no-cost.

The environment changed yesterday, however. Both top- and bottom-line measures of IVOL were sticky into equity market strength. This was observed via the pricing of spread structures (e.g., verticals and back- and ratio-spreads) structured above and below the market. The stickiness of volatility seemed to impact most the put side of the market. Some savvy traders may have been able to build spread structures below the market at a lesser cost potentially.

As an aside, some may have observed how well our levels have been working. For instance, as shown below (middle bottom), yesterday’s Daily Brief levels marked the session high and low for the Micro E-mini S&P 500 Index (FUTURE: /MES).

Graphic: Retrieved from TradingView.

Commentators online have rightly pointed out the build-up of short-dated options exposures near current market prices. In short, this activity, and its potential hedging, help promote mean-reversion and responsiveness at our volume profile-derived key levels, which often overlap with centers of significant options activity, as we see. Particularly after the quarterly options expiry (OpEx), this activity’s ability to contain markets will ease; markets will yield to fundamental strengths or weaknesses. Based on top-line measures of breadth and IVOL, “there isn’t much juice left to squeeze,” SpotGamma says. From an options positioning perspective, for volatility to reprice lower and solicit re-hedging that boosts the market, “we need a change in [the] volatility regime (i.e., soft landing, bank crisis resolved, etc.),” SpotGamma adds. The likelihood of that happening is low; some expect the Federal Reserve (Fed) to stick to its original message and continue to tighten and withdraw liquidity. So, blindly selling options (colloquially referred to as volatility) in this environment is dangerous.

Graphic: Retrieved from Bloomberg’s Joe Weisenthal.

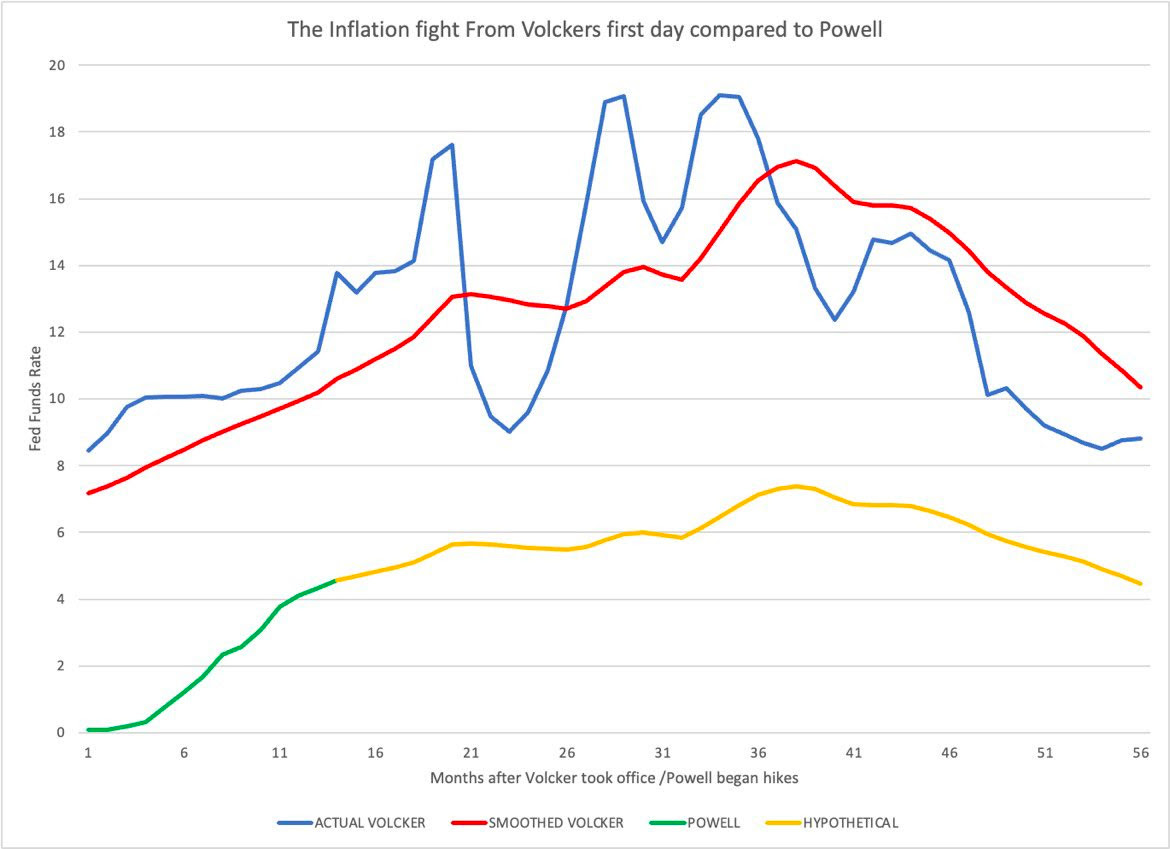

Damped Spring’s Andy Constan overlays past and present inflation fights. What if?

Graphic: Retrieved from Andy Constan of Damped Spring Advisors.

Technical

As of 8:00 AM ET, Friday’s regular session (9:30 AM – 4:00 PM ET) in the S&P 500 will likely open in the middle part of a balanced overnight inventory, inside of the prior day’s range, suggesting a limited potential for immediate directional opportunity.

The S&P 500 pivot for today is $4,087.75.

Key levels to the upside include $4,097.25, $4,108.75, and $4,121.25.

Key levels to the downside include $4,077.75, $4,062.25, and $4,049.75.

Disclaimer: Click here to load the updated key levels via the web-based TradingView platform. New links are produced daily. Quoted levels likely hold, barring an exogenous development.

Graphic: 65-minute profile chart of the Micro E-mini S&P 500 Futures (bottom middle).

About

The author, Renato Leonard Capelj, spends the bulk of his time at Physik Invest, an entity through which he invests and publishes free daily analyses to thousands of subscribers. The analyses offer him and his subscribers a way to stay on the right side of the market.

You may view this letter’s content calendar at this link.

Disclaimer

Do not construe this newsletter as advice; all content is for informational purposes, and derivatives carry a substantial risk of loss. Capelj and Physik Invest, non-professional advisors, will never solicit others for capital or collect fees and disbursements for their work.

The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 300+ that read this report daily, below!

Graphic updated 7:00 AM ET. Sentiment Neutral if expected /ES open is inside of the prior day’s range. /ES levels are derived from the profile graphic at the bottom of the following section. Levels may have changed since initially quoted; click here for the latest levels. SqueezeMetrics Dark Pool Index (DIX) and Gamma (GEX) calculations are based on where the prior day’s reading falls with respect to the MAX and MIN of all occurrences available. A higher DIX is bullish. At the same time, the lower the GEX, the more (expected) volatility. Learn the implications of volatility, direction, and moneyness. Breadth reflects a reading of the prior day’s NYSE Advance/Decline indicator. VIX reflects a current reading of the CBOE Volatility Index (INDEX: VIX) from 0-100.

Fundamental

An incredibly busy past few months with what it seems are back-to-back historic developments.

For instance, just this week, crypto broker Voyager Digital (OTC: VYGVF) filed for bankruptcy. “Impaired” will be account holders who likely won’t be “getting back exactly what they’re owed,” as reported by Bloomberg.

This is on the heels of crypto market volatility affecting some of Voyager’s largest borrowers like Three Arrows Capital, an embattled hedge fund. Voyager lent deposits to these parties at rates of interest that were ultra-high. Customers were then, accordingly, paid high rates.

However, this was done under the impression that the customer holdings were liquid, easy to access, and not subject to counterparty risks. That didn’t happen. Voyager, like others, was “making a lot of unsecured or undersecured loans.”

What’s the takeaway, here? Bloomberg’s Matt Levine explains well.

“If supposedly safe crypto brokerages keep failing and customers keep losing money, that is bad for the whole ecosystem; if your money isn’t safe with any crypto brokerage then you might just not buy crypto.”

Others in the ecosystem have continued to lever on the supposed successes of crypto. The failure of Voyager, among others, may have knock-on effects to be felt much later in the cycle.

From Voyager's subreddit. Pretty messed up; we keep talking about these companies throwing around nine-figure sums and make fun of people like Su Zhu, but in the end, they're all still living lavish lives. That $650m wasn't theirs – it was hundreds of people's savings added up. pic.twitter.com/DGxl09lCQz

Another historic development was the London Metal Exchange’s (LME) cancellation of billions of dollars in trades. This made whole large bettors in that ecosystem, all the while dinging liquidity providers, badly.

Some, including algorithmic fund Transtrend, left the LME as they could no longer trust it with client funds.

The question is what now? What’s the next big thing and, more importantly, will it have an impact on the traditional markets we watch?

As talked about in past analyses, it is over the last four decades that monetary policies were a go-to for supporting the economy. From that, created was “a disinterest and unimportance to cash flows.”

The commitment to reducing liquidity and credit has consequences on the real economy and asset prices, accordingly, which rose and kept the deflationary pressures of policies at bay.

It is elevated volatility, persistent declines, slower tightening processes abroad, among other things, that are to prompt investors to lower their selling prices in risk(ier) assets (e.g., options bets, metals, cryptocurrency and stablecoins, equities, bonds) and compete for cash.

Graphic: Via TradingView. Retrieved by Physik Invest.

This all is to continue bolstering the dollar’s surge to some of its strongest levels in years.

As well as further douse inflation (which is likely to peak on inventories bloat and a “supply gut”) and, eventually, prompt the Federal Reserve to reverse its aggressive rate hike and quantitative tightening (QT) path.

Graphic: Posted by Joe Weisenthal. “Wheat has erased all of its gains for the year. Also, it looks like corn and soy are rolling over.”

“It is starting,” Nassim Nicholas Taleb said online. “I’ve seen gluts not followed by shortages, but I’ve never seen a shortage not followed by a glut.”

ARK Invest’s Catherine Wood, who was very early to call the peak inflation, puts forth that “If inventories and stock prices are leading indicators for employment and wages, … then fears of cost-push inflation a la 1970’s should disappear during the next six months.”

Positioning

Thus far, we’re far into a dot-com type collapse, albeit one that has happened “underneath the surface of the indices,” per Simplify Asset Management’s Mike Green, as those largest stocks still are recipients of strong passive flows.

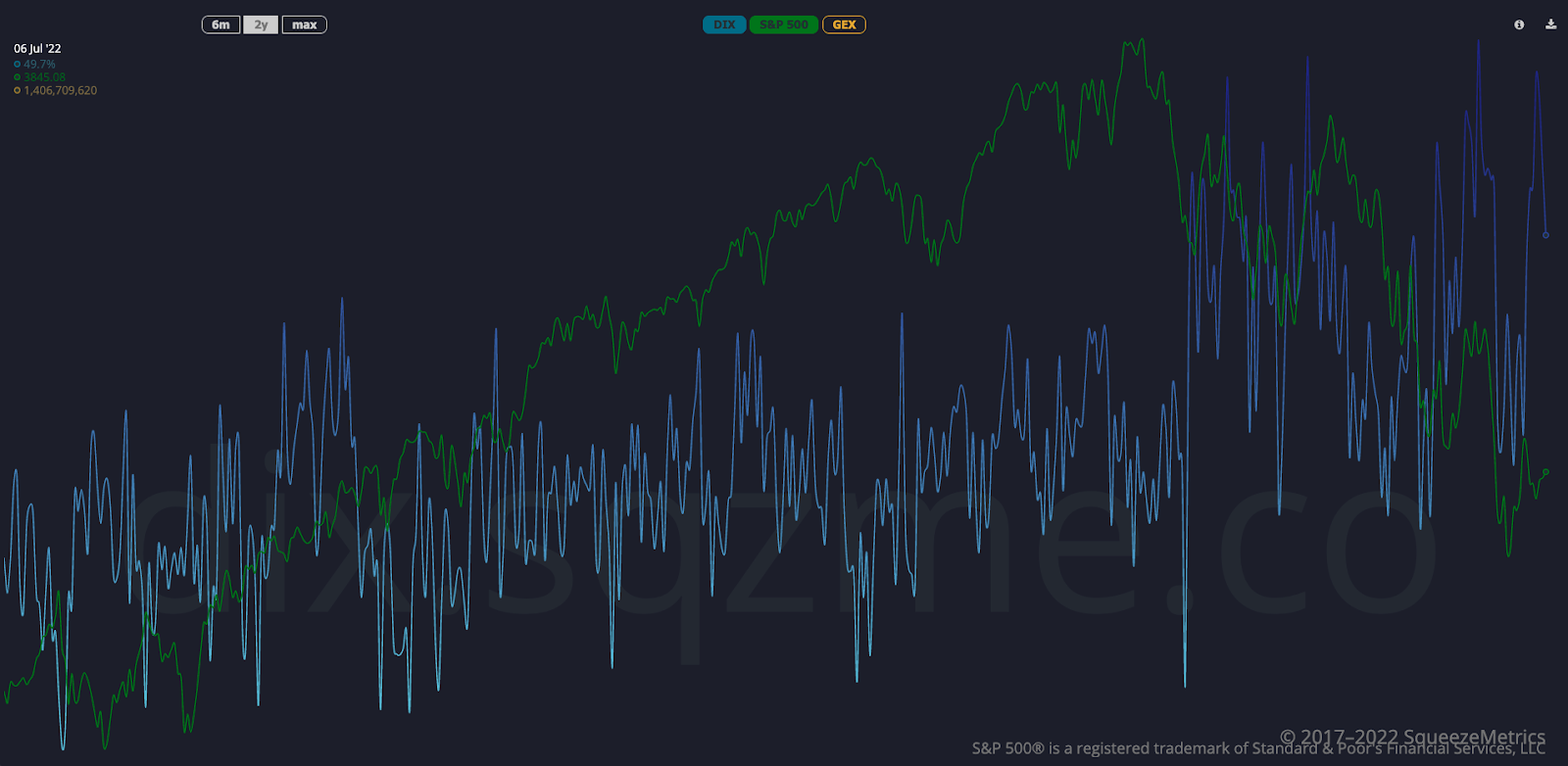

Graphic: SqueezeMetrics’ Dark Pool Index shows a trend in heightened implicit buying support.

The upcoming earnings season is likely to shed clarity with respect to corporates’ ability to weather or pass on higher costs. It is possible, as some put forth, that there is a broad “earnings compression,” deepening the de-rate in the face of what has been a “multiple compression.”

From a positioning perspective, so awing is the absence of heightened demand for downside skew, all the while that, on the upside, is bid probably due to the reach for bets on a ferocious bear market rally.

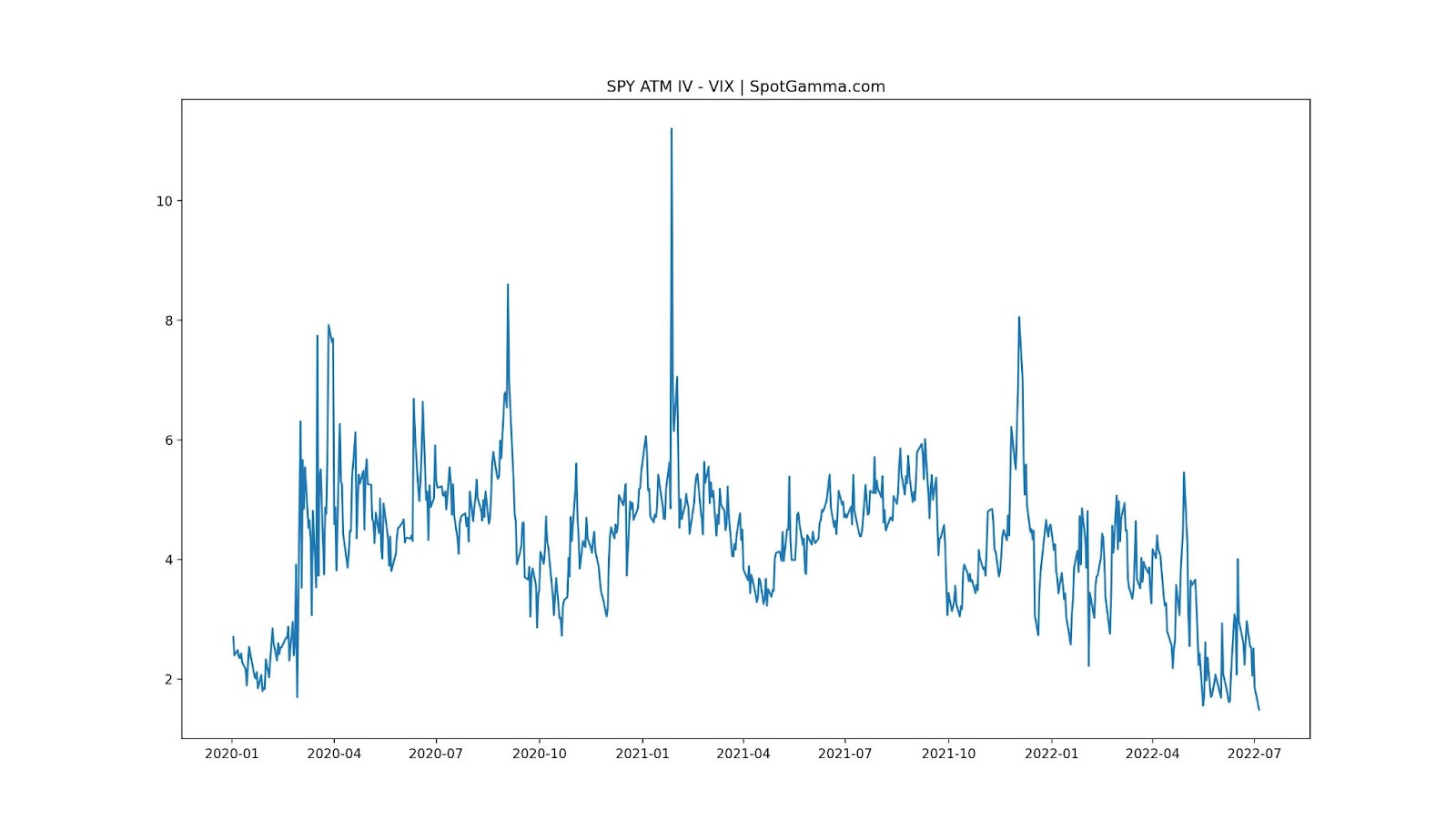

Graphic: Posted by SpotGamma. “30-day ATM SPY IV vs the VIX and while this plot has a bit of noise it seems to very closely resemble @Nations_Indexes VIX/VOLI measurement. One interpretation here is that OTM options aren’t trading for much premium over ATM (flat skew).”

As explained yesterday, it makes sense to be a buyer of volatility, albeit via complex structures.

For instance, buying volatility on the upside that is closer to current prices and selling that which is farther out (if bullish). And (if bearish), opting for calendars (as it is volatility in the shortest of maturities being sold heavily), back spreads, and the like.

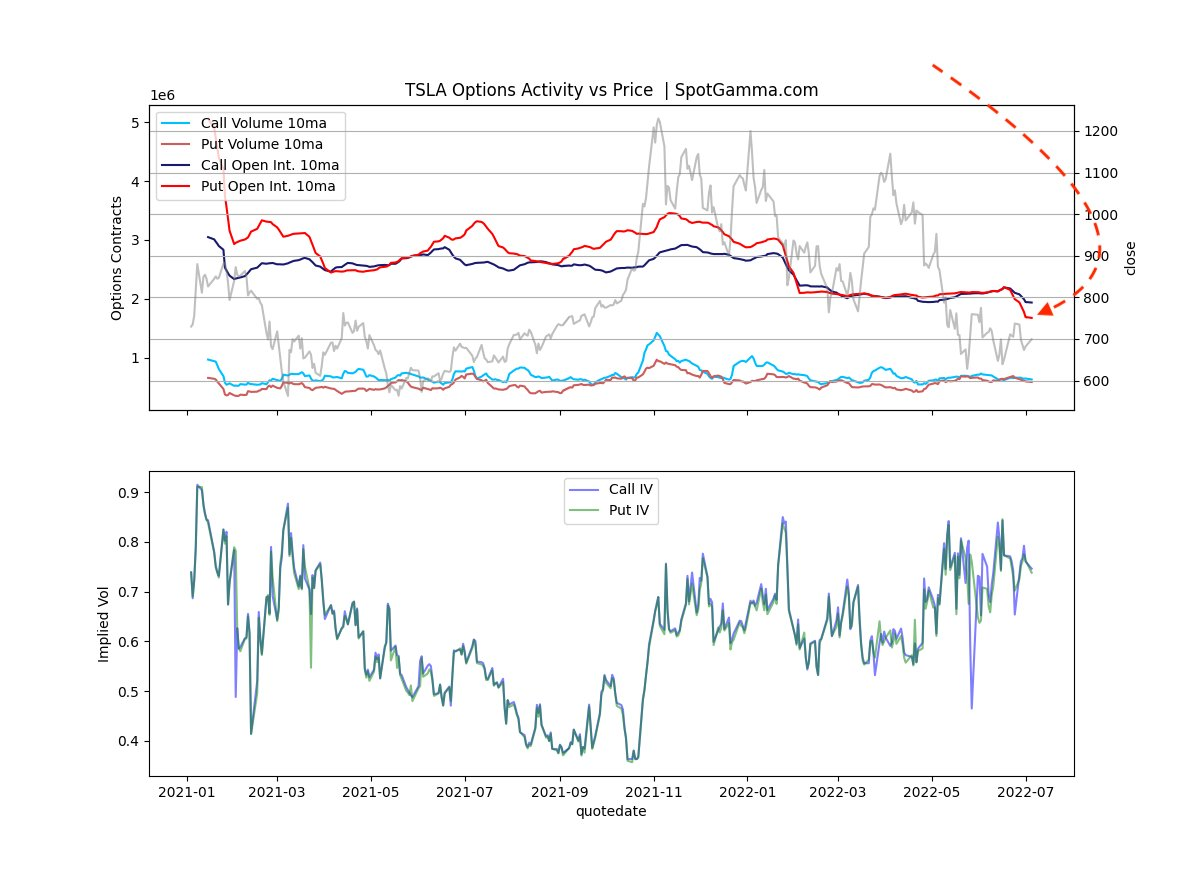

Graphic: Posted by SpotGamma. “TSLA open interest continues to decline, particularly on the put side as the stock trades near 1year lows. Interestingly at-the-money IV remains elevated to levels going back to the days of the $1200 call gamma squeeze.”

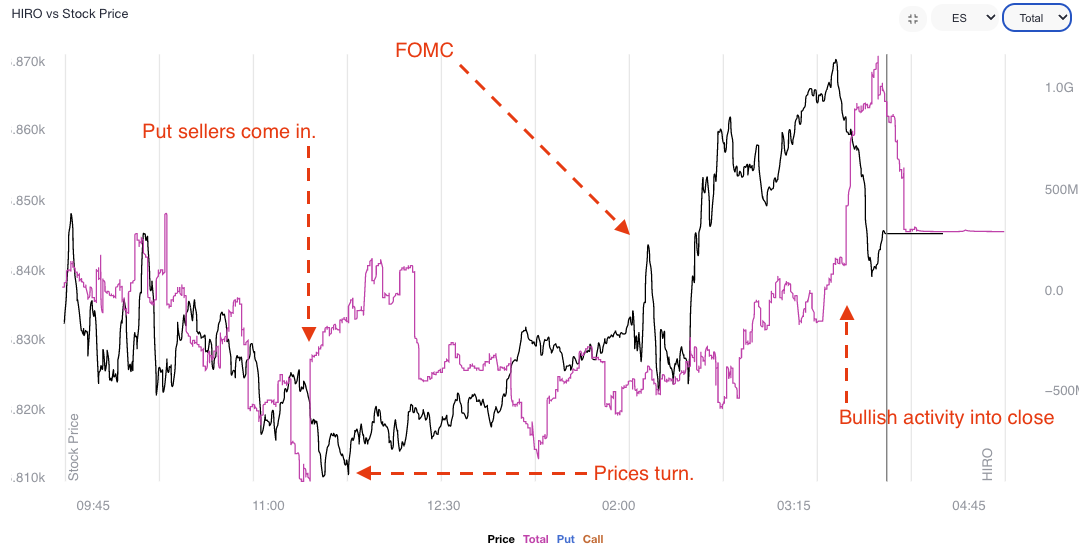

On a more granular level, after the release of the Federal Open Market Committee (FOMC) meeting minutes, participants added to their put sales and call buys, at the index level. The hedging of this does more to take from potential realized volatility.

Graphic: Pictured is SpotGamma’s Hedging Impact of Real-Time Options (HIRO) indicator.

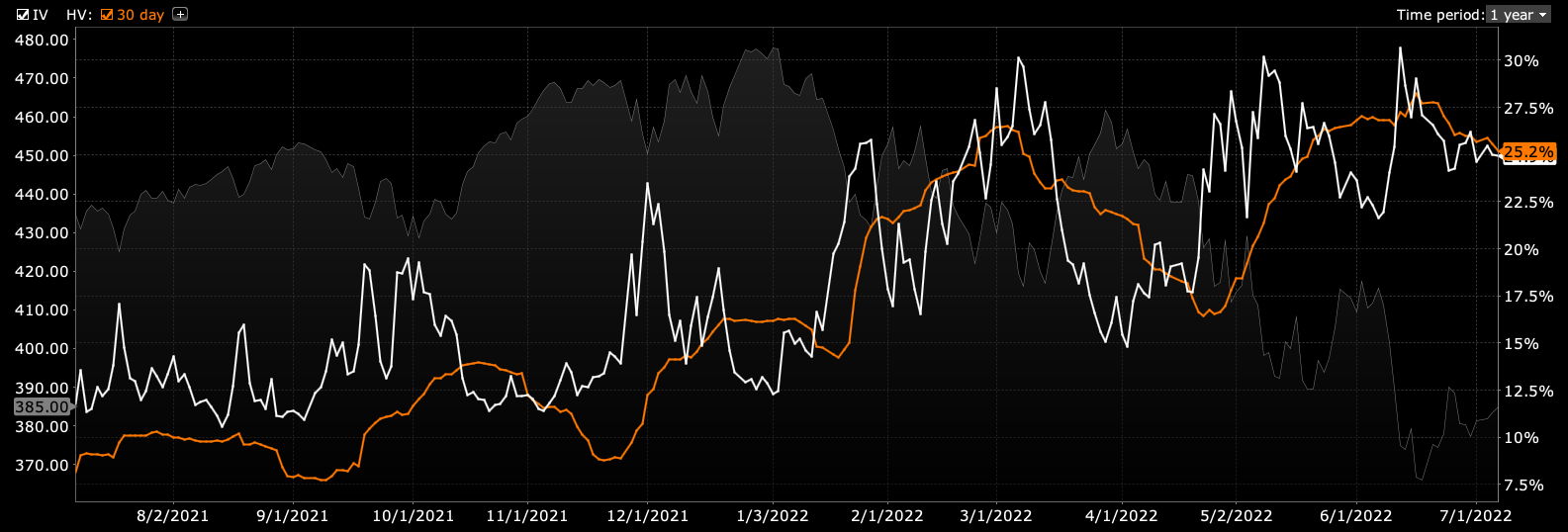

At its core, though, the market is at a pivot and losing the $3,800.00 S&P 500 area likely does more to bolster the creep in realized (RVOL) volatility, versus that which is implied (IVOL), all else equal.

Graphic: SPDR S&P 500 ETF Trust (NYSE: SPY) historical (orange) and implied (white) volatility via Interactive Brokers Group Inc’s (NASDAQ: IBKR) Trader Workstation.

Technical

As of 6:45 AM ET, Thursday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the middle part of a balanced overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher.

Any activity above the $3,859.00 overnight POC puts into play the $3,883.25 LVNode. Initiative trade beyond the LVNode could reach as high as the $3,909.25 MCPOC and $3,943.25 HVNode, or higher.

In the worst case, the S&P 500 trades lower.

Any activity below the $3,859.00 overnight POC puts into play the $3,831.00 VPOC. Initiative trade beyond the VPOC could reach as low as the $3,800.25 LVNode and $3,774.75 HVNode, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Graphic: 65-minute profile chart of the Micro E-mini S&P 500 Futures.

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.