The Daily Brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 200+ that read this report daily, below!

What Happened

Equity index futures were lower on some hawkish commentary from the Federal Reserve.

Ahead is data on jobless claims and trade deficit (8:30 AM ET), the ISM services index, factory orders, and core capital goods orders (10:00 AM ET), as well as Fed-speak (1:15 PM ET).

What To Expect

Fundamental: Yesterday, participants were provided further clarity around the Federal Reserve’s intent to hike interest rates and taper the pace of asset buying.

“At first blush, the December FOMC minutes read hawkish, and the market reaction supports this,” said Cliff Hodge, chief investment officer for Cornerstone Wealth.

“The fact that FOMC participants are discussing faster and more aggressive rate hikes, alongside a faster pace of balance sheet normalization than the last hiking, indicate that the Fed put for the stock market has been repriced lower.”

The news coincided with a fast move higher in Treasury yields and weakness in the growth- and innovation-heavy Nasdaq-100.

This is as higher rates have the potential to decrease the present value of future earnings making stocks, especially those that are high growth, less attractive.

Recall yesterday’s commentary touching on the implications of tight monetary frameworks and less liquidity, so to speak.

In short, easy monetary frameworks pushed participants out the risk curve.

As a result, removal of liquidity, in the face of increased exposure to risk across different assets, can result in “hedging and de-leveraging cascades that affect the stability of all markets,” as well put in one article I recently wrote.

“These derivatives are incredibly embedded in how the tail reacts and there’s not enough liquidity, given the leverage, if the Fed were to taper,” is one way to put it, additionally.

Positioning: Wednesday’s session unwound some of the single-stock bullishness that fed into S&P 500, itself.

Recall that Monday saw the selling of upside (call) and downside (put) protection. Tuesday saw more of the former, and that promoted some of the reversion, for lack of better phrasing.

Heading into Wednesday, volatility continued compressing. This is all the while the counterparty to the aforementioned trade was taking on more exposure to positive delta.

Why? Well, with any price rise, gamma (or how an option’s delta is expected to change given a change in the underlying) is added to the delta.

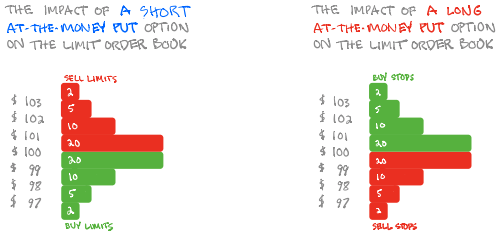

Counterparties are to offset gamma by adding liquidity (as can be approximated with thickening of book depth, below) to the market (i.e., buy dips, sell rips).

Therefore, as stated, yesterday, the continued compression of volatility would serve to bolster any price rise as “hedging vanna and charm flows, and whatnot will push the markets higher.”

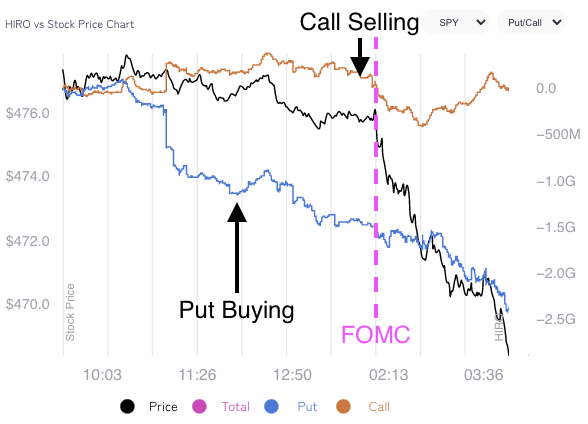

The tone changed, however. According to SpotGamma data (click here to learn more about access), customers sold upside (call) and bought downside (put) protection. The demand for puts accelerated after the release of FOMC minutes as can be seen via the chart, below.

That demand for protection coincided with an expansion in volatility; all else equal, higher implied volatility marks up options delta (exposure to direction).

With put buying, for instance, customers are indirectly taking liquidity and destabilizing the market as the market maker short the put will sell underlying to neutralize directional risk.

Higher implied volatility, higher delta, more selling. Hedging exacerbated weakness at the index and single-stock level, yesterday.

Taking into account the aforementioned positioning, versus buying pressure (measured via short sales or liquidity provision on the market-making side), positioning metrics remain positively skewed, better than before.

Though the dip lower and demand for protection may serve to prime the market for upside (when volatility starts to compress again and counterparties unwind hedges thus supporting any attempt higher), markets will tend toward instability so long as volatility is heightened and the market remains in short-gamma territory.

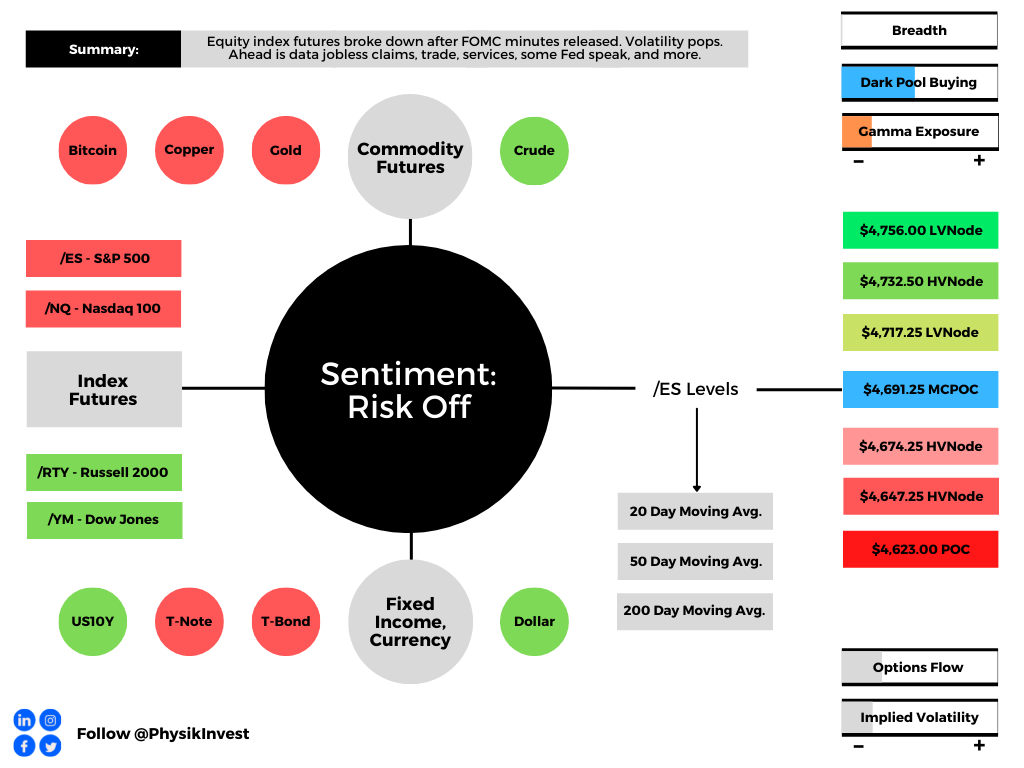

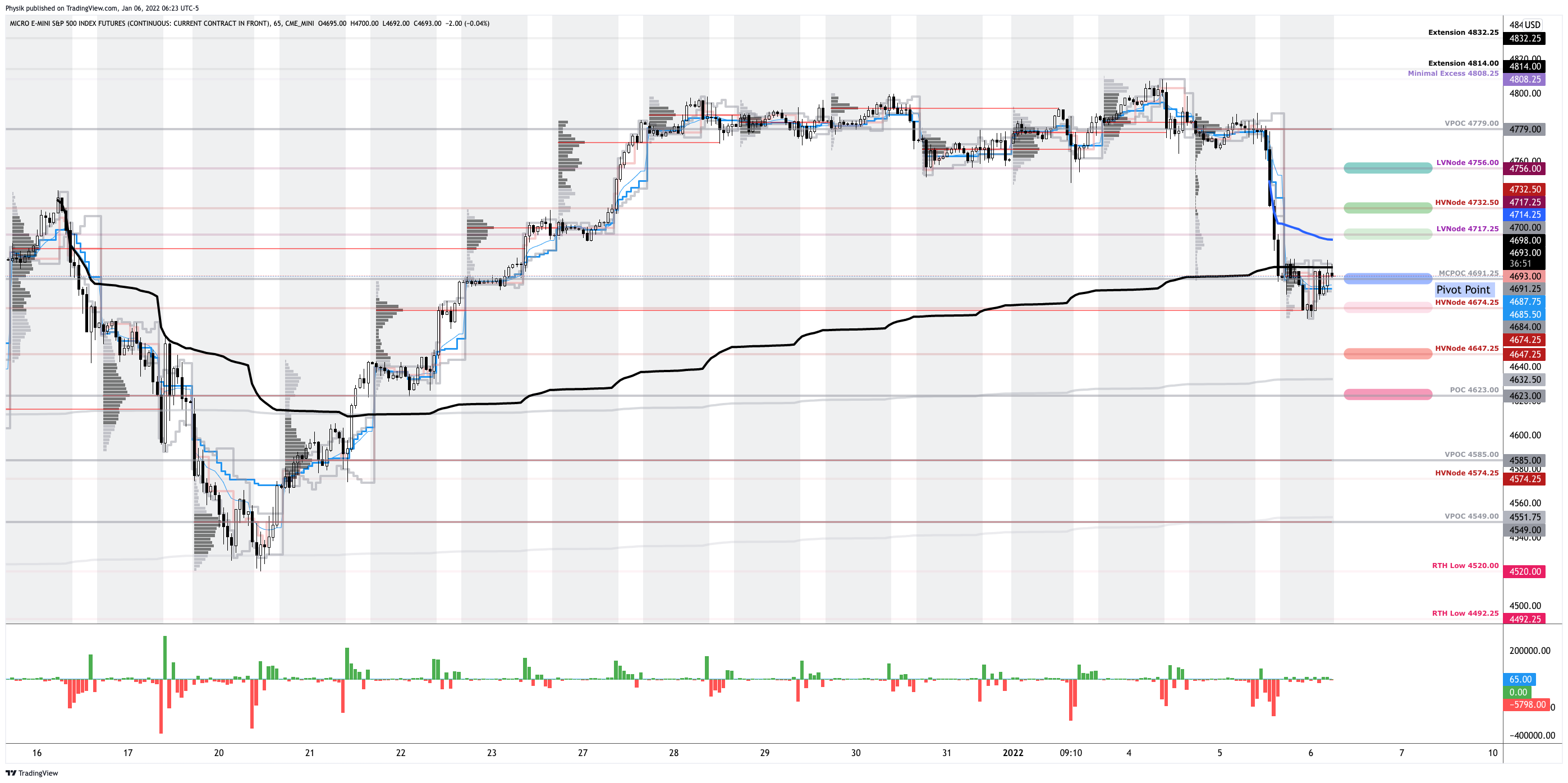

Technical: As of 6:30 AM ET, Thursday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the middle part of a negatively skewed overnight inventory, just outside of prior-range and -value, suggesting a potential for immediate directional opportunity.

Spike Scenario In Play: Spike’s mark the beginning of a break from value. Spikes higher (lower) are validated by trade at or above (below) the spike base (i.e., the origin of the spike). Spike base is at $4,761.25. Above, bullish. Below, bearish.

In the best case, the S&P 500 trades higher; activity above the $4,691.25 micro composite point of control (MCPOC) puts in play the $4,717.25 low volume area (LVNode). Initiative trade beyond the LVNode could reach as high as the $4,732.50 high volume area (HVNode) and $4,756.00 LVNode, or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,691.25 MCPOC puts in play the $4,674.25 HVNode. Initiative trade beyond the latter could reach as low as the $4,647.25 HVNode and $4,623.00 point of control (POC), or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

What People Are Saying

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

DIX: For every buyer is a seller (usually a market maker). Using DIX — which is derived from short sales (i.e., liquidity provision on the market-making side) — we can measure buying pressure.

Gamma: Gamma is the sensitivity of an option to changes in the underlying price. Dealers that take the other side of options trades hedge their exposure to risk by buying and selling the underlying. When dealers are short-gamma, they hedge by buying into strength and selling into weakness. When dealers are long-gamma, they hedge by selling into strength and buying into weakness. The former exacerbates volatility. The latter calms volatility.

Vanna: The rate at which the delta of an option changes with respect to volatility.

Charm: The rate at which the delta of an option changes with respect to time.

Options: If an option buyer was short (long) stock, he or she would buy a call (put) to hedge upside (downside) exposure. Option buyers can also use options as an efficient way to gain directional exposure.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj is also a Benzinga finance and technology reporter interviewing the likes of Shark Tank’s Kevin O’Leary, JC2 Ventures’ John Chambers, FTX’s Sam Bankman-Fried, and ARK Invest’s Catherine Wood, as well as a SpotGamma contributor developing insights around impactful options market dynamics.

Disclaimer

Physik Invest does not carry the right to provide advice.

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.