What Happened

Overnight, equity index futures auctioned higher. Ahead is data on Markit Manufacturing PMI (9:45 AM ET) and Construction Spending (10:00 AM ET).

What To Expect

Technicals: Given the Monday gap, the S&P 500, based on its relation to Thursday’s failed balance breakout and end-of-week liquidation, is positioned for sideways-to-higher.

To note, however, the persistence of responses to technical levels, weaker-handed participants (which seldom bear the wherewithal to defend retests) carry a heavier hand in recent discovery.

Via volume profile analysis, we see a plethora of low-volume pockets – voids – that likely hold virgin tests. Successful penetration often portends follow-through as the participants that were most active at those levels (quickly run for the exits when wrong).

Fundamental: The aforementioned trade is happening in the context of higher valuations, interest rates, and tax rates, according to Morgan Stanley (NYSE: MS).

These themes serve as a headwind.

To elaborate, as Nordea recently explained, the Fed will “accelerate its tapering process, and is now set to conclude net purchases already by mid-March vs mid-June with the earlier pace.”

“The dot plot was revised significantly higher, and the plot now shows three hikes for next year, a further three for 2023 and another two for 2024.”

At the same time, equity markets tend to rally into the first hike; Moody’s Corporation’s (NYSE: MCO) forecast aligns with that – “the Dow Jones Industrial Average increases this quarter and peaks in early 2022, … [followed by] steady decline through 2022.”

Why? Rising rates, among other factors, have the potential to decrease the present value of future earnings, thereby making stocks, especially those that are high growth, less attractive.

“Our view is that 2022 will be the year of a full global recovery, an end of the global pandemic, and a return to normal conditions we had prior to the Covid-19 outbreak,” JPMorgan Chase & Co (NYSE: JPM) noted.

“We believe this will produce a strong cyclical recovery, a return of global mobility, and strong growth in consumer and corporate spending, within the backdrop of still-easy monetary policy.”

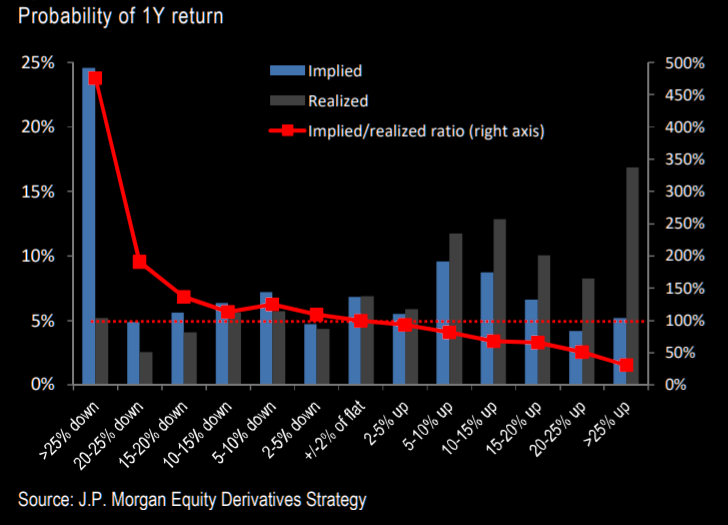

Positioning: According to JPMorgan Chase & Co, “S&P 500 skew overprices downside and underprices upside probabilities relative to historical returns.”

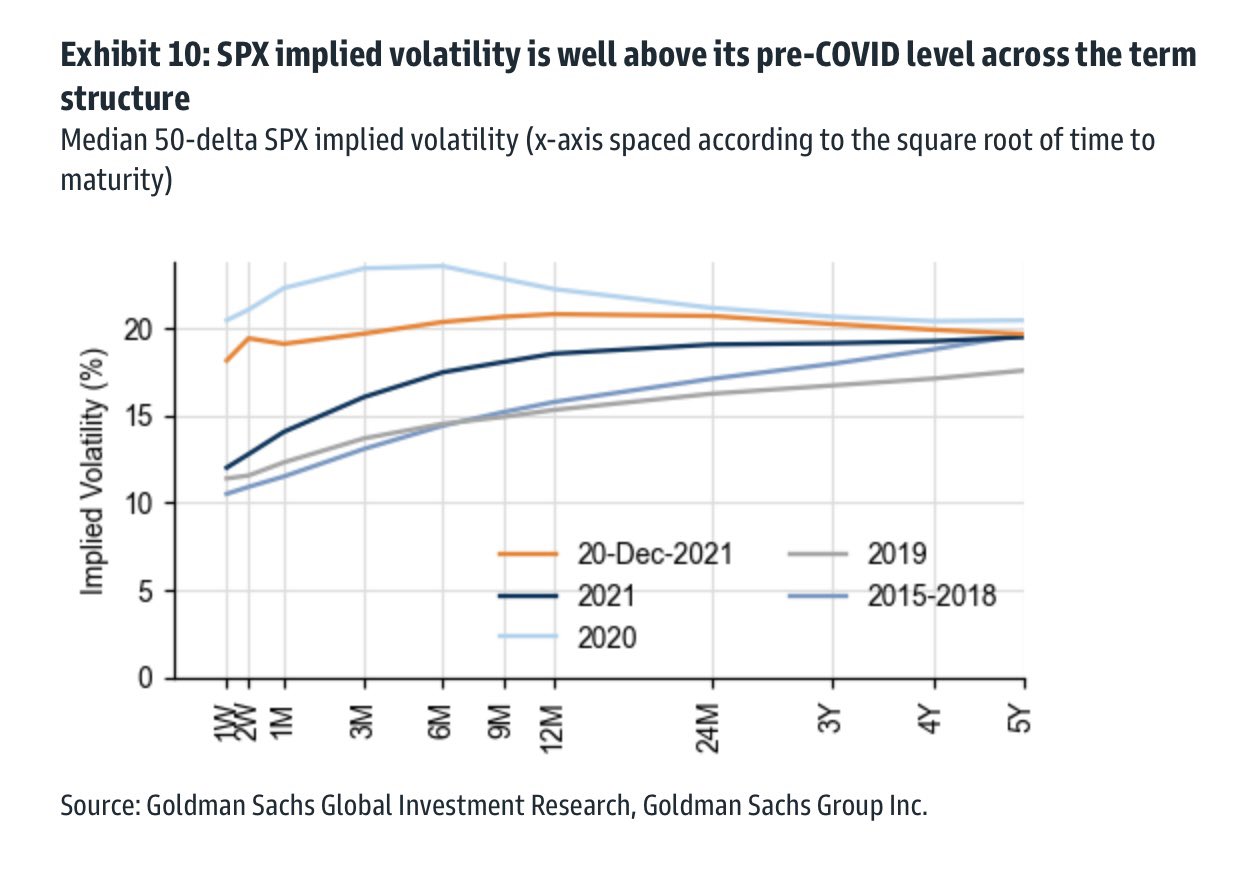

This is all the while the S&P 500’s implied volatility remains above pre-COVID levels.

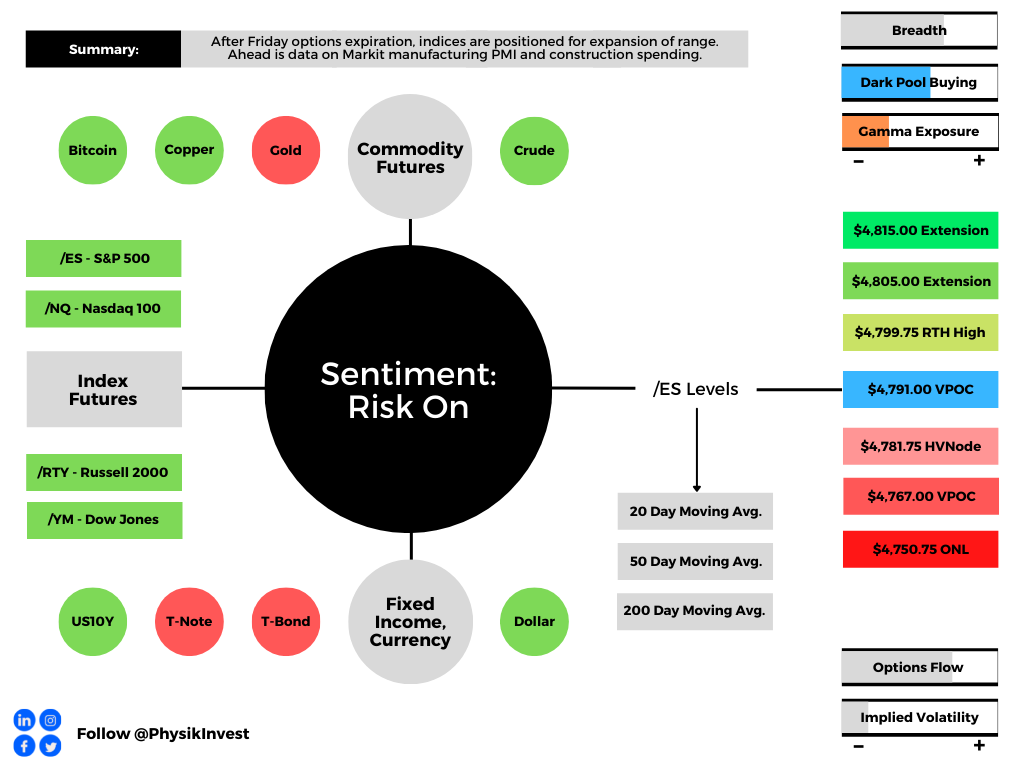

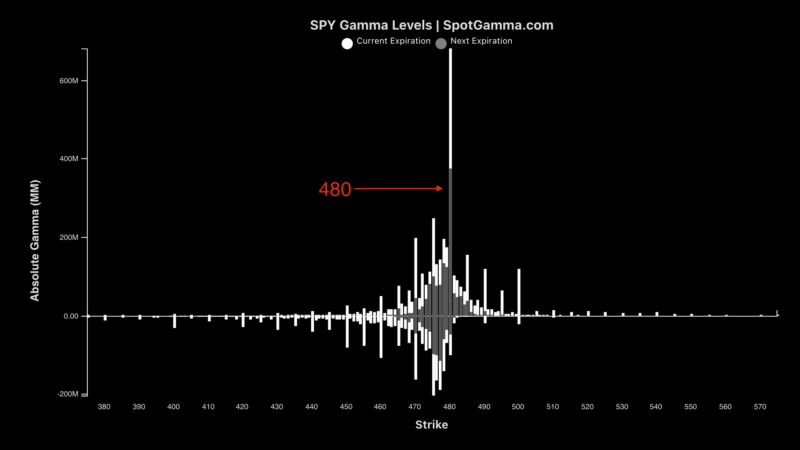

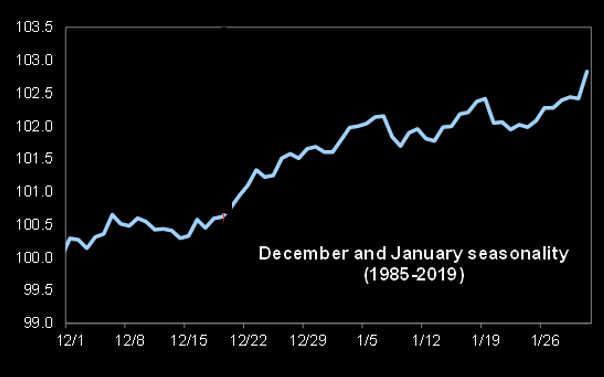

Taken together (in the face of last week’s options expiration which reduced the level of positive sticky options gamma concentrated mostly at the $4,800.00 level in the S&P 500), current options positioning and buying pressure supports a seasonally-aligned price rise in January.

Explanation: As a position’s delta rises with underlying price rises, gamma (or how an option’s delta is expected to change given a change in the underlying) is added to the delta. Counterparties are to offset gamma by adding liquidity to the market (i.e., buy dips, sell rips).

The continued compression of volatility will only serve to bolster any price rise as “hedging vanna and charm flows, and whatnot will push the markets higher.”

Should that thesis not pan out – meaning the removal of hedging pressures associated with “put-heavy” single stock options positions and an end to tax-loss harvesting, among other factors – indices likely succumb to the “stealth correction” of its lesser weighted constituents.

Were participants to reach for downside protection, the implications of this would be staggering. In such a case, markets will tend toward instability. At present, the metrics don’t point to this.

Expectations: As of 6:20 AM ET, Monday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the upper part of a positively skewed overnight inventory, outside of prior-range and -value, suggesting a potential for immediate directional opportunity.

Gap Scenarios: Gaps ought to fill quickly. Should they not, that’s a signal of strength; do not fade. Leaving value behind on a gap-fill or failing to fill a gap (i.e., remaining outside of the prior session’s range) is a go-with indicator. Auctioning and spending at least 1-hour of trade back in the prior range suggests a lack of conviction; in such a case, do not follow the direction of the most recent initiative activity.

In the best case, the S&P 500 trades higher; activity above the $4,791.00 untested point of control (VPOC) puts in play the $4,799.75 regular trade high (RTH High). Initiative trade beyond the RTH High could reach as high as the $4,805.00 and $4,815.00 extensions, or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,791.00 VPOC puts in play the $4,781.75 high volume area (HVNode). Initiative trade beyond the HVNode could reach as low as the $4,767.00 VPOC and $4,750.75 overnight low (ONL), or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

What People Are Saying

Definitions

Overnight Rally Highs (Lows): Typically, there is a low historical probability associated with overnight rally-highs (lows) ending the upside (downside) discovery process.

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

Gamma: Gamma is the sensitivity of an option to changes in the underlying price. Dealers that take the other side of options trades hedge their exposure to risk by buying and selling the underlying. When dealers are short-gamma, they hedge by buying into strength and selling into weakness. When dealers are long-gamma, they hedge by selling into strength and buying into weakness. The former exacerbates volatility. The latter calms volatility.

Vanna: The rate at which the delta of an option changes with respect to volatility.

Charm: The rate at which the delta of an option changes with respect to time.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

Options Expiration (OPEX): Traditionally, option expiries mark an end to pinning (i.e, the theory that market makers and institutions short options move stocks to the point where the greatest dollar value of contracts will expire) and the reduction dealer gamma exposure.

Excess: A proper end to price discovery; the market travels too far while advertising prices. Responsive, other-timeframe (OTF) participants aggressively enter the market, leaving tails or gaps which denote unfair prices.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj is also a Benzinga finance and technology reporter interviewing the likes of Shark Tank’s Kevin O’Leary, JC2 Ventures’ John Chambers, FTX’s Sam Bankman-Fried, and ARK Invest’s Catherine Wood, as well as a SpotGamma contributor developing insights around impactful options market dynamics.

Disclaimer

At this time, Physik Invest does not carry the right to provide advice.

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.