Market Commentary

Key Takeaways: After a short sell-off, volatility ebbs as equity index futures trade higher.

- Unpacking factors lending to the volatility.

- Jitters ahead of Federal Reserve meeting.

- Earnings outlook up. Priced to perfection?

- COVID-19 resurgence to not limit mobility.

- Analyzing tightening and the shift to fiscal.

What Happened: Last week’s violent trade came as inflation measures rose the largest since the Global Financial Crisis.

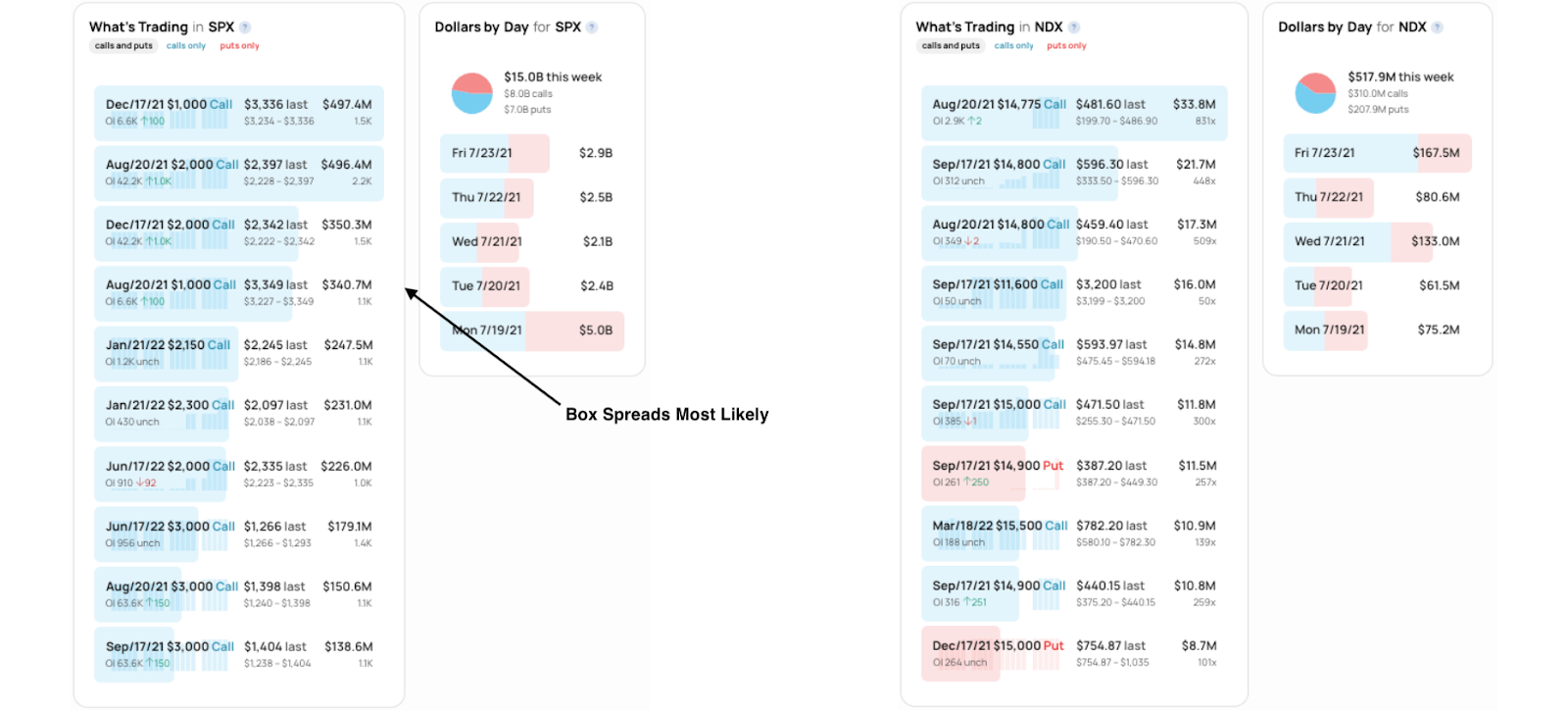

At and around the same time was a monthly options expiration (OPEX) which opened the window to fundamental dynamics (e.g., a shift in preferences from saving and investing to spending, monetary tightening, seasonality, COVID-19 resurgence) given a “reduction in large options positions, and the hedging associated with them,” according to SpotGamma, an authority in the space.

The subsequent sell-off then moved the market into short-gamma, an environment in which the opposing side of options trades hedge by buying into strength and selling into weakness, thereby exacerbating volatility.

To note, we’re discussing the implications of derivatives since option volumes are comparable to stock volumes and, as a result, related hedging flows can represent an increased share of volume in underlying stocks.

Further, the reversal caught many by surprise. Why? Downside risks were thought to have been compounded by equity, bond, and derivatives market positioning, among other factors.

For instance, some metrics implied froth with respect to the number of put options being sold to open, a potentially destabilizing force given associated hedging forces.

To note, put sales, which can be part of sophisticated volatility-based trading strategies, can imply confidence as market participants look to options for income, and not insurance.

Amidst the selling, though, some indicators suggested participants more so became interested in puts as downside protection.

Then, on July 19, the S&P 500 rebounded as near-term discovery reached a potential limit, based on market liquidity metrics and the inventory positioning of participants.

SpotGamma’s metrics confirmed; participants bought calls and sold puts suggesting confidence in the low.

In explaining the violent reversal and follow-through, it’s useful to point to three factors – the change in the underlying price (gamma), implied volatility (vanna), and time (charm) – known to impact an options exposure to directional risk or delta.

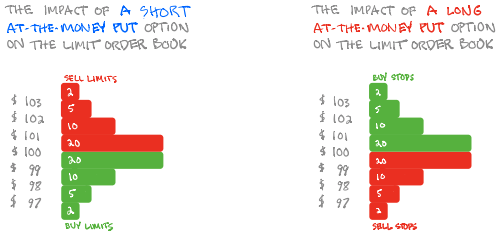

In short, in selling a put, for instance, customers indirectly add liquidity and stabilize the market.

How? The market maker long the put will buy (sell) the underlying to neutralize directional risk as price falls (rises).

On the other hand, as the market reverses and continues rising, volatility compresses, and any puts that were bought quickly lose value, thereby lowering the opposing side’s directional risk.

As a result, short hedges are bought back, adding fuel to the price rise.

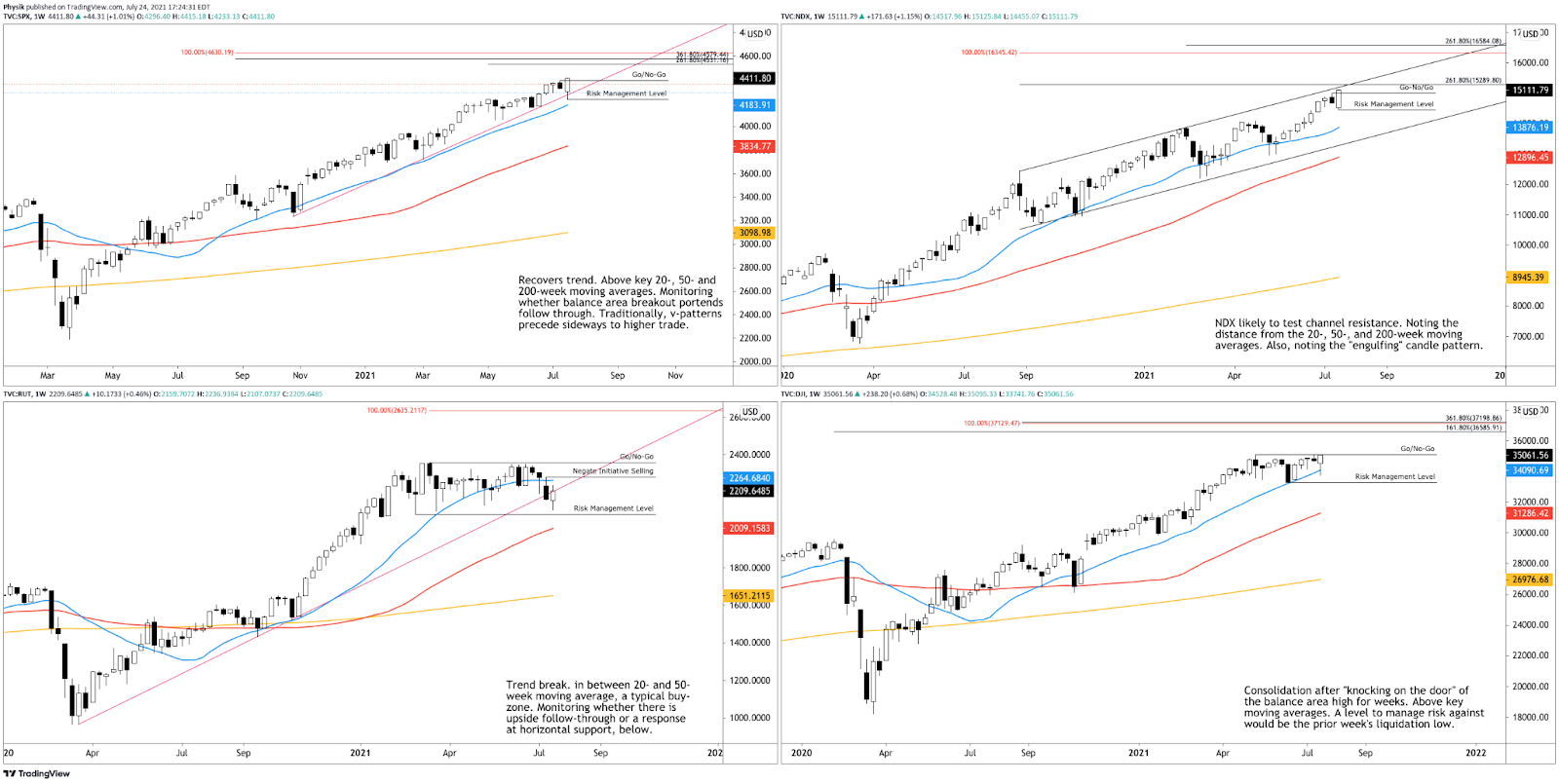

Considerations: The recession is over and the outlook for earnings is great.

That is reflected by heightened valuations, peak positioning, and S&P 500 price targets.

Also, in spite of extreme fear in the face of a COVID-19 resurgence, red states, where the risks of transmission are greater given lower vaccination rates, will likely not limit mobility while blue states are more so highly vaccinated and will remain mobile, according to Bloomberg.

That brings us to the topic of monetary policy.

The U.S. is in a different place from the rest of the world and is likely to eliminate its output gap this year which would call for a tightening in policy and dollar strengthening, helping douse inflation.

On that note, Moody’s strategists comment: “The impressive growth in value across many asset classes is projected to taper off within the next couple of years as supportive policy is unwound. The 10-year Treasury yield will rise above 2% by 2022 and the fiscal tailwinds will also have faded by then.”

When liquidity is removed, as policymakers look to fiscal policy to address inequality, for instance, corporations may have to worry about making money, again.

“That’s ultimately how we grow out of these valuations,” Kai Volatility’s Cem Karsan explained to me in an article Benzinga will release next week. “These cycles are a lot shorter than the monetary supply-side cycles but they tend to be very bad for multiples and great for economic growth.”

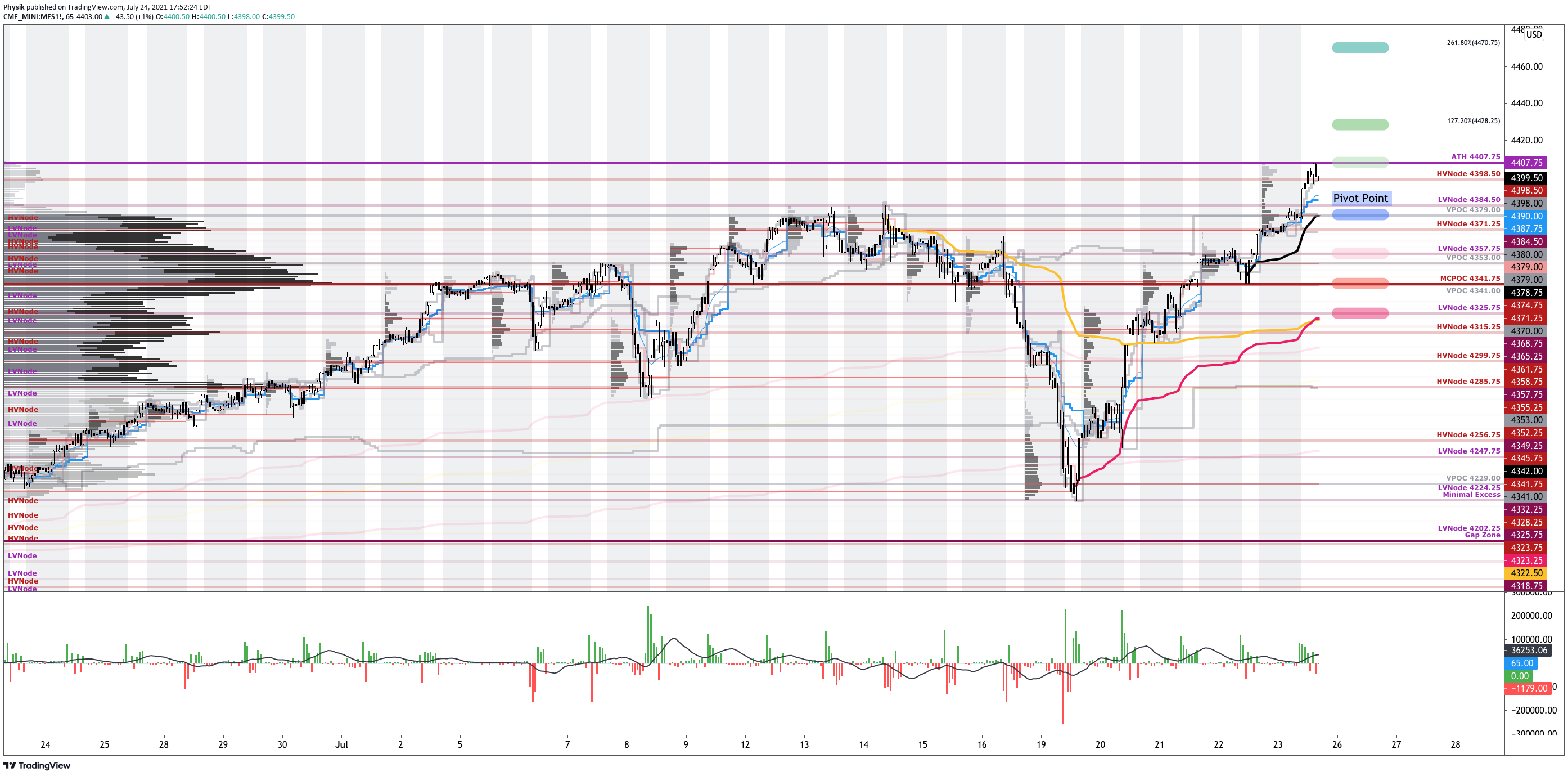

What To Expect: Ahead of the upcoming Federal Reserve meeting, participants will want to temper their expectations on future volatility and focus their attention on where the S&P 500 trades in relation to the $4,384.50 low volume area (LVNode) pivot, a prior all-time high (ATH).

In the best case, the S&P 500 trades sideways or higher; activity above the $4,384.50 LVNode puts in play the $4,407.75 ATH. Initiative trade beyond the ATH could reach as high as the $4,428.25 and $4,470.75 Fibonacci-derived price extensions.

In the worst case, the S&P 500 trades lower; activity below the $4,384.50 LVNode puts in play the $4,357.75 LVNode. Initiative trade beyond the $4,357.75 LVNode could reach as low as the $4,341.75 micro-composite Point of Control (MCPOC) and $4,325.75 LVNode.

Note also that the last key level corresponds with two key Volume Weighted Average Price (VWAP) levels, a metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

Volume Areas: A structurally sound market will build on past areas of high volume. Should the market trend for long periods of time, it will lack sound structure (identified as a low volume area which denotes directional conviction and ought to offer support on any test). If participants were to auction and find acceptance into areas of prior low volume, then future discovery ought to be volatile and quick as participants look to areas of high volume for favorable entry or exit. POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent. Participants will respond to future tests of value as they offer favorable entry and exit. Significance Of Prior ATHs, ATLs: Prices often encounter resistance (support) at prior highs (lows) due to the supply (demand) of old business. These areas take time to resolve. Breaking and establishing value (i.e., trading more than 30-minutes beyond this level) portends continuation.

About

After years of self-education, strategy development, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets. Additionally, Capelj is a finance and technology reporter. Some of his biggest works include interviews with leaders such as John Chambers, founder and CEO, JC2 Ventures, Kevin O’Leary, businessman and Shark Tank host, Catherine Wood, CEO and CIO, ARK Invest, among others.

Disclaimer

At this time, Physik Invest does not manage outside capital and is not licensed. In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.