The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 300+ that read this report daily, below!

What Happened

Overnight, equity index futures traded sideways-to-lower, keeping intact the bearish tone from yesterday. Commodities were mixed. Bonds, the dollar, and implied volatility were bid.

At a micro-level, the selling was not similar to that of past market turmoil events. Instead, stocks were sold, but on the back of tame and steady volumes. Adding, the market’s responsiveness to key visual areas may mean that participants with shorter time horizons are more active, pointing to the potential that those with larger horizons are waiting for better entry or more information.

In terms of the news, similar to yesterday, narratives remain uninspiring. The key is that there are signs that inflation may soon turn the corner, as discussed in yesterday morning’s letter. In accordance with that perspective are comments by trader and macro strategist Andy Constan, who this letter’s author spoke with last week and will share insights extracted, below.

Ahead is data on GDP (8:30 AM ET), as well as talks by Federal Reserve (Fed) and European Central Bank (ECB) officials (9:00 AM ET, 11:30 AM ET, and 1:05 PM ET).

What To Expect

Perspectives: This letter’s objective is to provide salient information one may use in developing a tradeable narrative. Today, we’re taking a different approach and adding some diversity to the format by threading important points from the conversation Physik Invest’s Renato Capelj had with trader and macro strategist Andy Constan, the CEO and CIO of Damped Spring Advisors.

Without further ado, here it is.

The University of Pennsylvania alumnus had his start in finance in the 1980s when he joined Salomon Brothers. There, he excelled quickly and was the “go-to for questions.”

At one point, Salomon tapped Constan for his assistance with the 1987 stock market crash where he learned more about self-reinforcing market strains and how dynamic hedging processes may manifest market volatility.

Constan, later, managed Salomon’s derivatives operations, as well as the sale of those services. He said a lot of his success, in those years, was owed to making “everything systematic” and “operat[ing] with a framework.”

He, then, spent some time at Ray Dalio’s Bridgewater Associates where he was key in the firm’s research on volatility as an asset class. The lesson Bridgewater instilled was to “spend time finding the persistent trade,” parameterizing and executing, accordingly.

The alpha stream from the capture of that systemic edge is an asset itself.

Through the decades of experience, Constan eventually pivoted after recognizing that edges built on top of relative value (RV) – “the capture of inefficiencies generated from some form of concentrated positioning that pushes assets out of whack” – would fail on macro happenings.

Most noteworthy were Constan’s comments on the market’s de-rate.

As we’ve talked about in this letter in the past, for decades monetary policies were the go-to instrument for stimulation. This money stocked a technological revolution, bolstered the supply of goods, and, by that token, promoted deflation, which was kept at bay by rising asset prices.

Trends in the geopolitical climate, a focus on fiscal stimulation, as well as supply chokepoints, have stoked goods and services inflation. The commitment to addressing inequality, as well as misallocations of capital through a tightening of liquidity and credit has consequences on the economy and asset prices, which are highly connected given multi-decade trends.

Stemming inflation, via supply-side economics, alone, is folly, as explained in the article. Trends like de-globalization are destructive to prosperity.

“The most destructive things to future prosperity are the tendencies that have developed over the last five years, like Brexit, the border wall, and the war in Ukraine. Comparative advantages, which globalization is essential for, generates uninsured supply chains and now we’re spending money on insurance.”

As the article explains, at its core, prices are set by the equilibrium between the supply and demand for goods. Both are not in line, and the stimulative monetary policies that helped keep the supply-side in check are not on the table, all the while supply chain replication is not adding to production.

Though that’s inflationary, political gridlock is a dampener on the trend.

What about the more pressing matter? Are we in a recession?

The simple answer is yes, and 2022 is likely to be a 1% total GDP year with a 4% inflation rate. That said, an equity market recovery is not off the table.

“We’re in a recession — a period of modestly to significantly below-trend growth — and the fiscal side would have to not force the Fed to do more by having a large spending bill which would hurt markets in a meaningful way.”

On the expression of opinions, Constan’s preferred method is to use defined risk options trades structured around his macro theses two to four months out in maturity.

If volatility is rich, he will lean on selling credit. If volatility is cheap, he will opt to buy spreads.

“I want deltas and leverage. My macro indicators give me an edge on price and in the worst case, the loss is limited to 10%, if everything has to go against me all at once. I can be 100% invested and only risk 10%.”

Read Full-Text: Former Bridgewater Associate Talks Recession Odds, Capturing A Macro Edge

Follow Andy Constan on Twitter, here.

Positioning: Little has changed. The volatility that the markets are realizing (RVOL) is high and, at times, in excess of that implied (IVOL).

To cut to the chase, there’s a “higher starting point” in IVOL, and a still-present right-tail (from the positioning for a bear market rally).

Both make it so we may, for zero or no cost, trade short-dated structures with asymmetric payouts.

Read: Trading Volatility, Correlation, Term Structure and Skew by Colin Bennett et al. Originally sourced via Academia.edu.

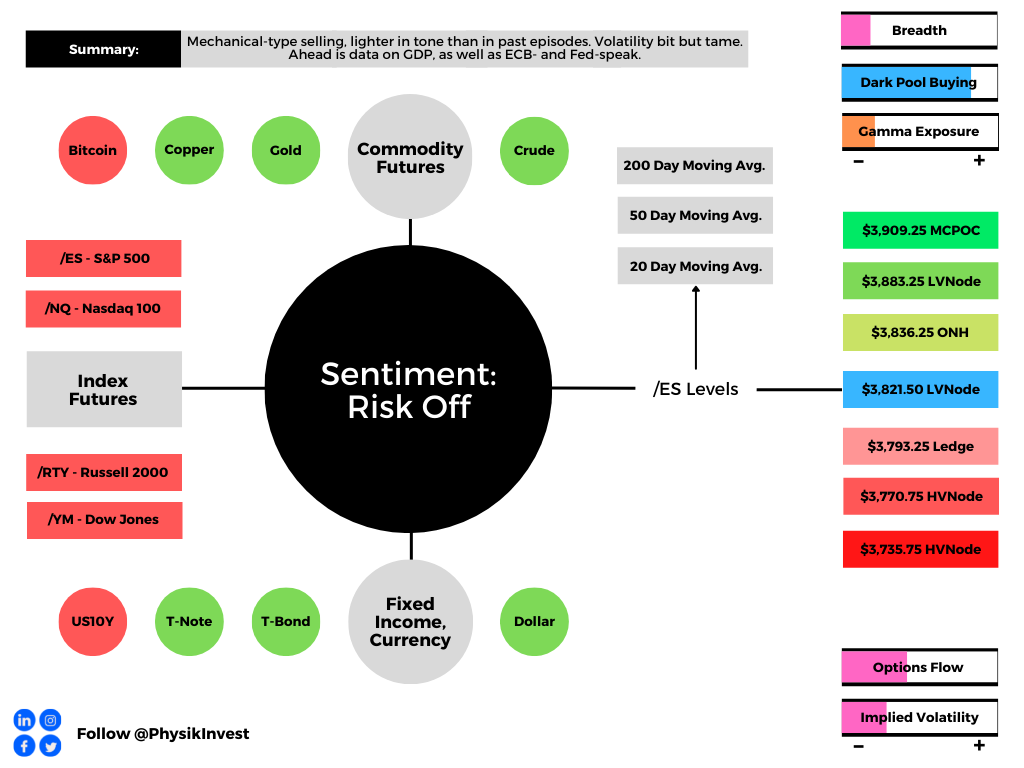

Technical: As of 6:30 AM ET, Wednesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the lower part of a negatively skewed overnight inventory, outside of prior-range and -value, suggesting a potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher; activity above the $3,821.50 LVNode puts in play the $3,836.25 ONH. Initiative trade beyond the ONH could reach as high as the $3,883.25 LVNode and $3,909.25 MCPOC, or higher.

In the worst case, the S&P 500 trades lower; activity below the $3,821.50 LVNode puts in play the $3,793.25 Ledge. Initiative trade beyond the Ledge could reach as low as the $3,770.75 and $3,735.75 HVNode, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Considerations: Push-and-pull (responsiveness) near key-technical areas (that are discernable visually on a chart), suggests technically-driven traders with short time horizons are very active.

Such traders often lack the wherewithal to defend retests and, additionally, the type of trade may be indicative of the other time frame participants waiting for more information to initiate trades.

What People Are Saying

Definitions

Overnight Rally Highs (Lows): Typically, there is a low historical probability associated with overnight rally-highs (lows) ending the upside (downside) discovery process.

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

Some of his works include conversations with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, FTX’s Sam Bankman-Fried, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, among many others.

Disclaimer

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.