The Daily Brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 200+ that read this report daily, below!

What Happened

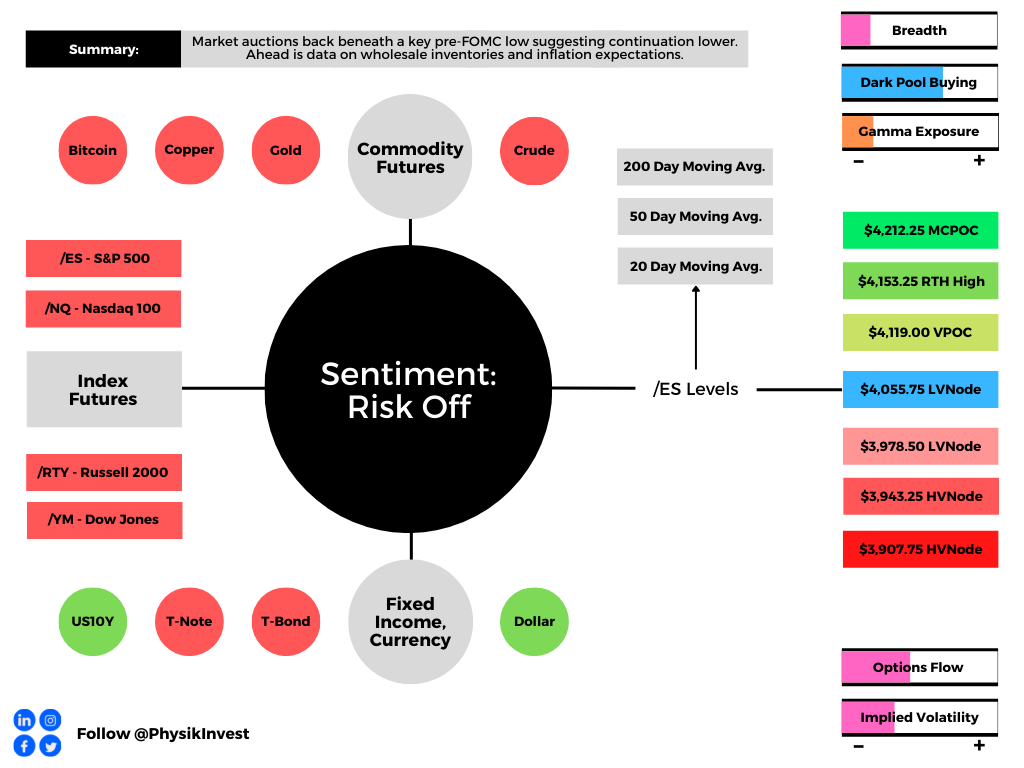

Overnight, equity index, commodity, and bond futures were all lower while yields, and implied volatility metrics we monitor were bid.

This is as new fundamental data did little to disrupt the Federal Reserve’s (Fed’s) course to hike rates and reduce the size of its balance sheet, as well as the odds of further slowing as a result of actions to curb the spread of COVID-19 abroad, and geopolitical conflict.

Goldman Sachs Group Inc (NYSE: GS), among others, cut their equity market forecasts. Presently, they see an economic contraction playing into the S&P 500’s test of $3,600.00.

Notable is the market’s retest of a very key technical area ($4,055.75 in the E-mini S&P 500). This area, last week, likely solicited responsive buying by technically-driven market participants who often lack the wherewithal to defend retests, just days before the Fed’s decision on policy.

Now, the market is set to open below those key technical areas and that is the worst outcome.

Ahead is data on wholesale inventories (10:00 AM ET), as well as inflation (11:00 AM ET).

What To Expect

Positioning: Last week’s letters went in-depth on the implications of volatility divergences, the post-Fed rally, responses to key technical levels, and beyond.

On Friday, May 6, 2022, this letter essentially remarked the following:

Based on stretched positioning, equity markets are positioned for upside. Notwithstanding, the potential for large negative outliers, remains. In the case of an outlier, the consequent repricing of volatility may increase the reward, relative to the risk, for selling options.

How do you know whether the risk is worth the reward?

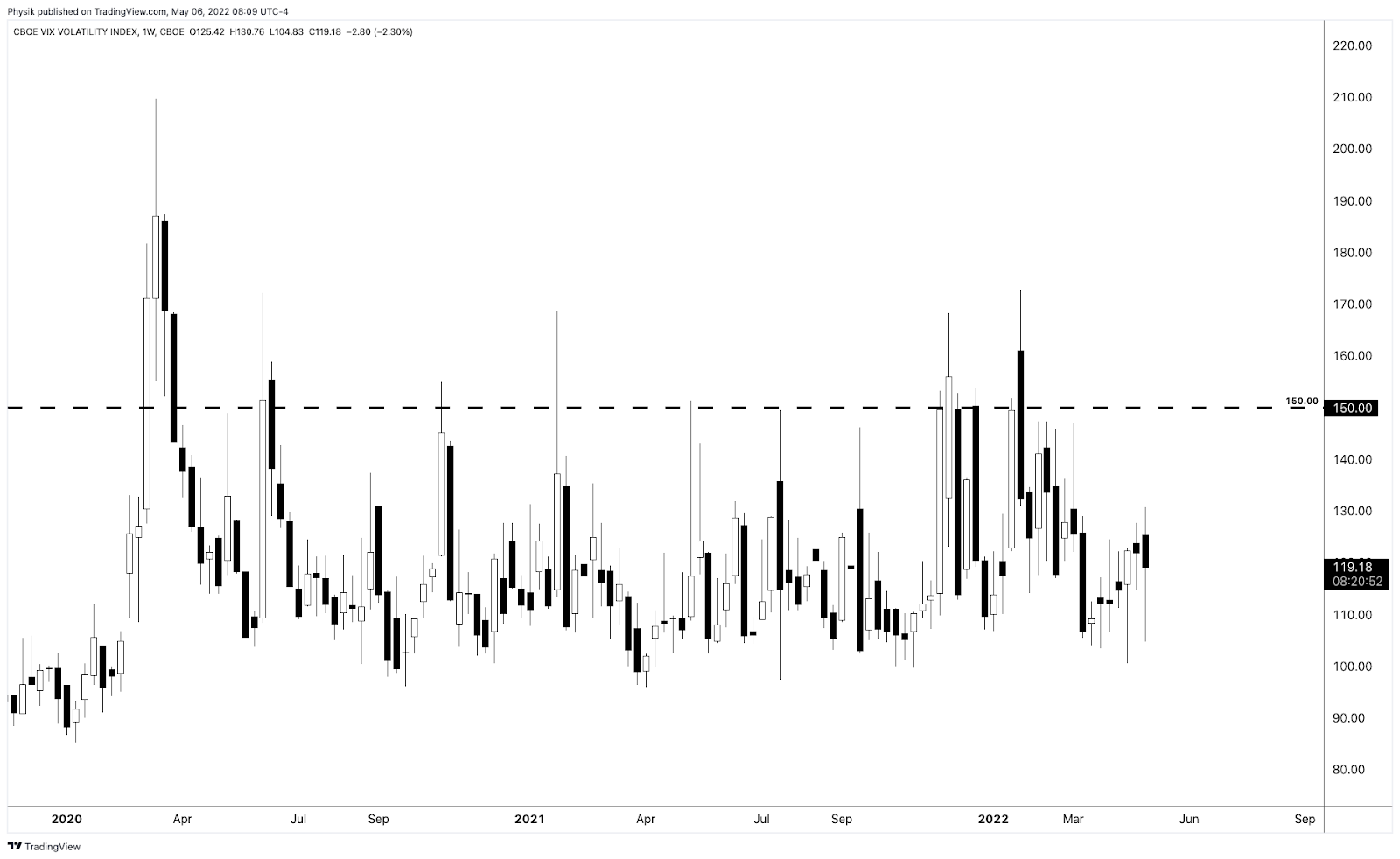

A naive measure like the Cboe VVIX Index (INDEX: VVIX), which measures the volatility of volatility, has a mean below 100 and a high correlation with the Cboe Volatility Index (INDEX: VIX) during times of stress.

When realized volatility is as high as it is, today, the VVIX typically trades closer to 150.

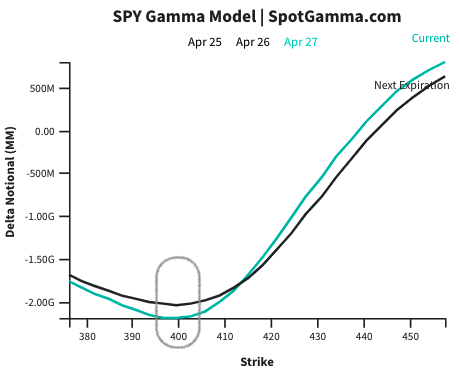

We’re not there yet and the market remains well-hedged, as SpotGamma explains well:

“From an options perspective, participants would have to demand en masse protection (buy puts, sell calls) for liquidity providers to further take from market liquidity (sell into weakness) and that volatility skew to, essentially, blowout (e.g., Corona crisis, Meme mania, and the like).”

Pursuant to those remarks, SpotGamma sees markets reaching a lower limit near the $4,000.00 SPX area. At that juncture, the rate at which liquidity providers add pressure in their hedging activities flattens as they, too, have hedges.

“In turn, dealers may be able to advantageously reduce delta hedging (sell less), and supply markets with more liquidity (buy more stock). This could serve to reduce volatility.”

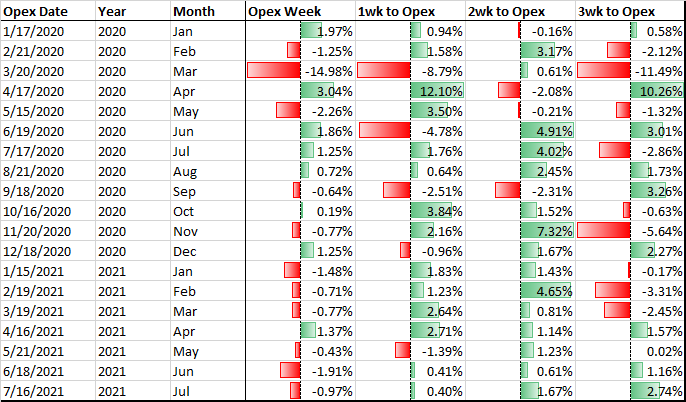

Noting, later this month is a large options expiration (OPEX), and expected is the roll-off of a large amount of put-heavy negative gamma.

Per Pat Hennessy of IPS Strategic Capital, returns one to two weeks prior are skewed bullish.

This is amid what is a front-running of the bullish flow associated with the delta decay of options with respect to changes in volatility (vanna) and time (charm), among other factors.

In other words, it is participants’ increased awareness of the implications of options and OPEX that has resulted in a front running. According to SqueezeMetrics, “People didn’t know about the OpEx week effect (in this case, largely charm). Now everyone and their mother knows about it.’”

So what?

Charm is a measure of an options delta’s change with respect to the passage of time. As time passes, delta “bleeds” as options decay.

As most participants, at least at the index level, own protection, the counterparties to this trade are short protection. These counterparties, therefore, have positive exposure to delta (i.e., as index falls [rises], position loses [makes] money) and negative exposure to gamma, or delta (directional) sensitivity to underlying price changes (i.e., as the index moves against short option exposure, losses are multiplied).

Moreover, given the growth of options volumes, participants’ heavy demand for protection matters more, to put simply. Counterparties, in light of this recent drop, pressured markets with their hedging. The decay (and eventual expiry) of this protection marks options deltas down.

To re-hedge, counterparties buy back short stock and futures hedges. This supportive action is what has been front-run. The bullishness of the event can happen in the days and weeks prior.

Technical: As of 6:35 AM ET, Monday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the lower part of a negatively skewed overnight inventory, outside of prior-range and -value, suggesting a potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher; activity above the $4,055.75 low volume area (LVNode/gap boundary) puts in play the $4,119.00 untested point of control (VPOC). Initiative trade beyond the VPOC could reach as high as the $4,153.25 regular trade high (RTH High) and $4,212.25 micro composite point of control (MCPOC), or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,055.75 LVNode/gap boundary puts in play the $3,978.50 LVNode/gap boundary. Initiative trade beyond the LVNode/gap boundary could reach as low as the $3,943.25 and $3,907.75 high volume areas (HVNodes), or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

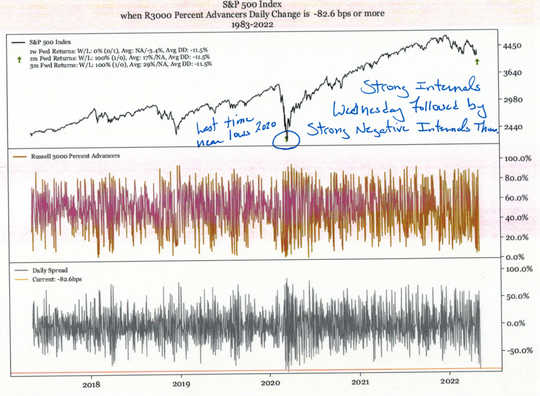

Considerations: Last Tuesday, we discussed the response to a key technical level ($4,055.75).

Specifically, the E-mini S&P 500 probed $4,056.00 before staging a sharp reversal and closing higher. This was noteworthy as it told us a lot about who was gaining the upper hand.

Push-and-pull, as well as responsiveness near key-technical areas (discernable visually on a chart), suggests technically-driven traders with shorter time horizons are (becoming) active.

Such traders often lack the wherewithal to defend retests.

Moreover, heading into last week’s Federal Open Market Committee (FOMC) event, large participants (who often move by committee) de-grossed and hedged resulting in poor reliability of our technical levels.

In the days leading up to the event, these larger had little to do with respect to repositioning.

The market’s tests of key technical areas solicited responsive buying by these short-term traders, and this played into a rally that continued through FOMC. Post-FOMC, the market quickly succumbed to the initiative selling by longer time frame participants.

All else equal, Monday’s regular trade is expected to start somewhere below a key technical area that solicited strong responsive buying by shorter timeframes.

Given capital constraints and tolerances, shorter timeframes may fuel an acceleration of the prevailing downtrend.

What People Are Saying

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

Some of his works include conversations with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, FTX’s Sam Bankman-Fried, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, among many others.

Disclaimer

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.