Editor’s Note: The Daily Brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 200+ that read this report daily, below!

What Happened

Overnight, equity index futures were divergent and weighed by the tech- and growth-heavy Nasdaq 100. Most commodity and bond products were much weaker, also.

This stocks down, bonds down dynamic points to a continued deleveraging.

Notwithstanding, sideways after a fast move lower, is not a bad thing. It’s one of the better cases to have given certain mechanics with respect to the options market, for instance.

Ahead is data on international trade (8:30 AM ET) and real household debt (11:00 AM ET).

What To Expect

Fundamental: Ranges, at the index level, have tightened markedly since the January sell-off culminating in a cross-market deleveraging cascade.

The situation is different at the single-stock level. There are a couple of factors behind this.

For one, ARK Invest’s Catherine Wood recently made an interesting point suggesting events of today are the exact opposite of the events leading into the tech-and-telecom bust.

“During the tech-and-telecom bubble, … investors were falling all over each other, trying to one-up each other, to get a bigger tech position, because tech in the indexes had moved to 35%. We saw many portfolios with 40%, 50% tech.”

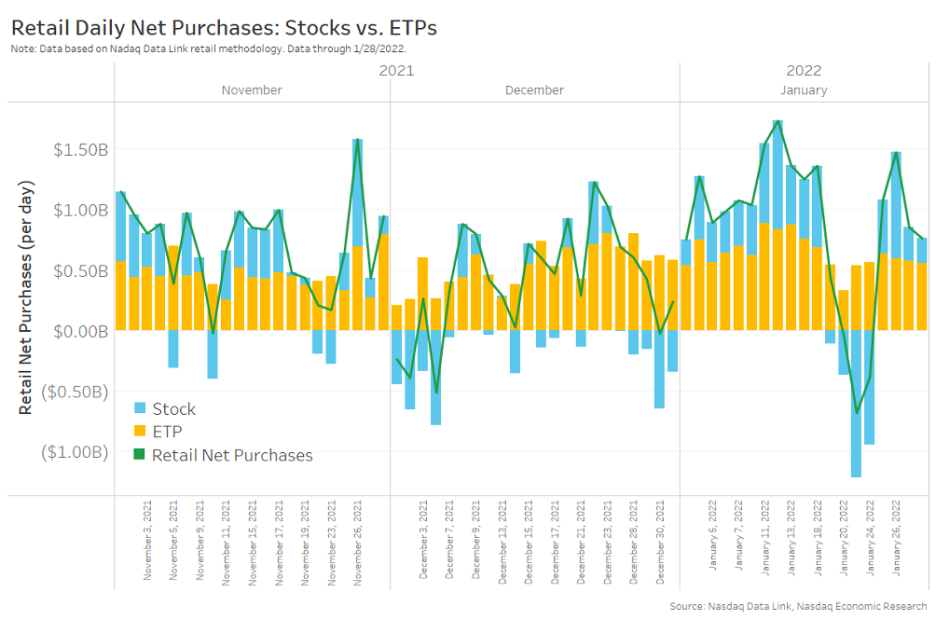

Basically, Wood thinks that investors are dumping single-stocks for index exposure. The below data supports this.

“We think that decision is going to prove to be just as incorrect as the decision to move en masse in the late 90s.”

There is also the increasing demand for positive delta (long) exposure in the indexes as participants hedge their negative delta (short) exposure in the single stocks.

Then, there is also the supply and demand for options protection, at the index level.

Mainly, the indexes are where the world will hedge and so the effects of dealers re-hedging their risks to decaying options protection provide markets a sort of passive buying support.

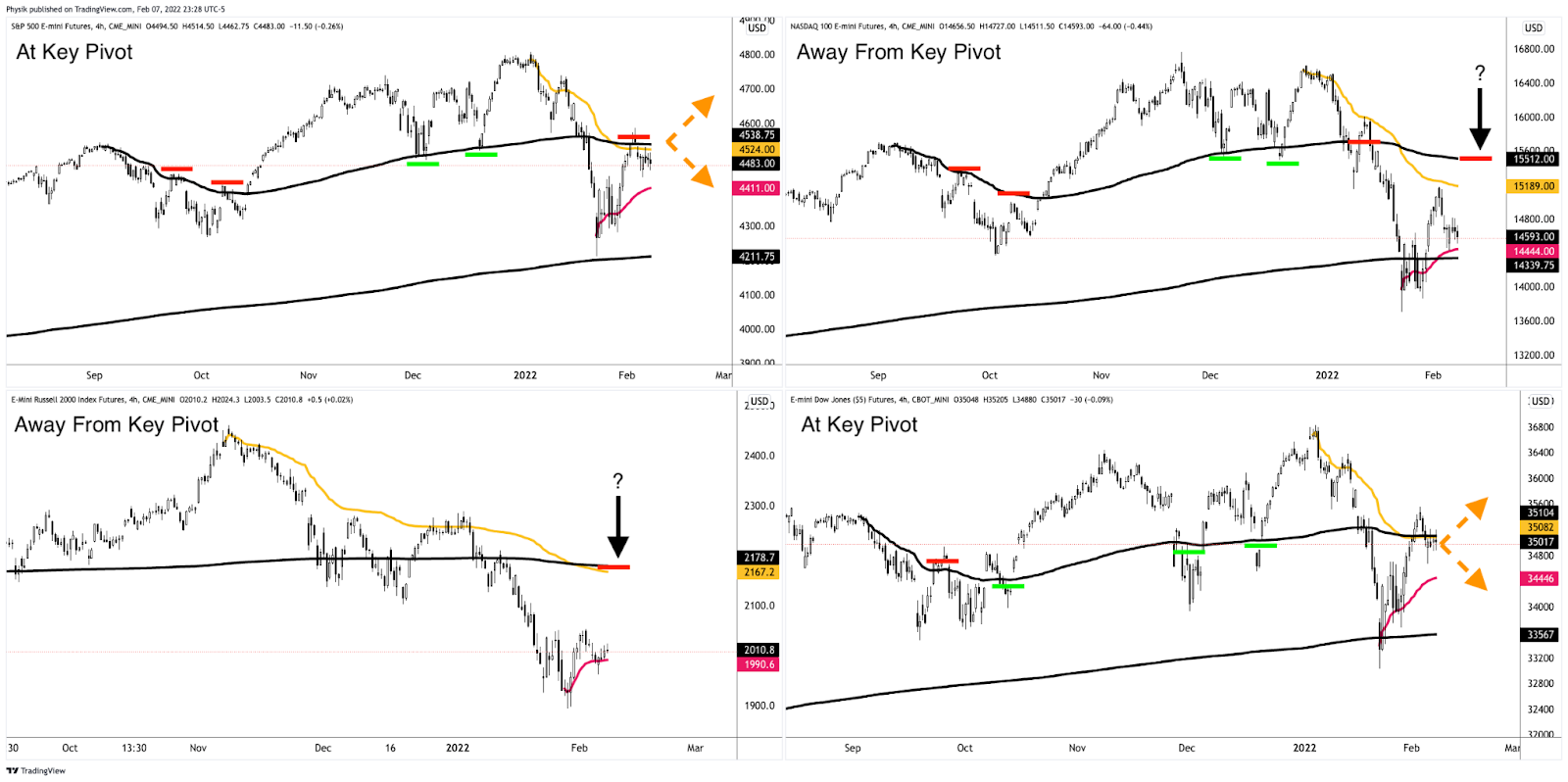

The S&P 500, which carries a more liquid derivatives complex and less exposure to tech- and growth-heavy constituents (when compared to the Nasdaq 100 and Russell 2000), appears stronger, but not as strong as the Dow Jones Industrial Average, a clear beneficiary of the rotation out of growth- and innovation-names to value- and cyclical-type stocks.

All the last-mentioned point is trying to make is the following: try hard enough and you’ll find an explanation for anything.

Sometimes, though, a focus on the simplest of explanations (e.g., demand for assets that perform better in higher rate environments) may suffice in navigating volatility.

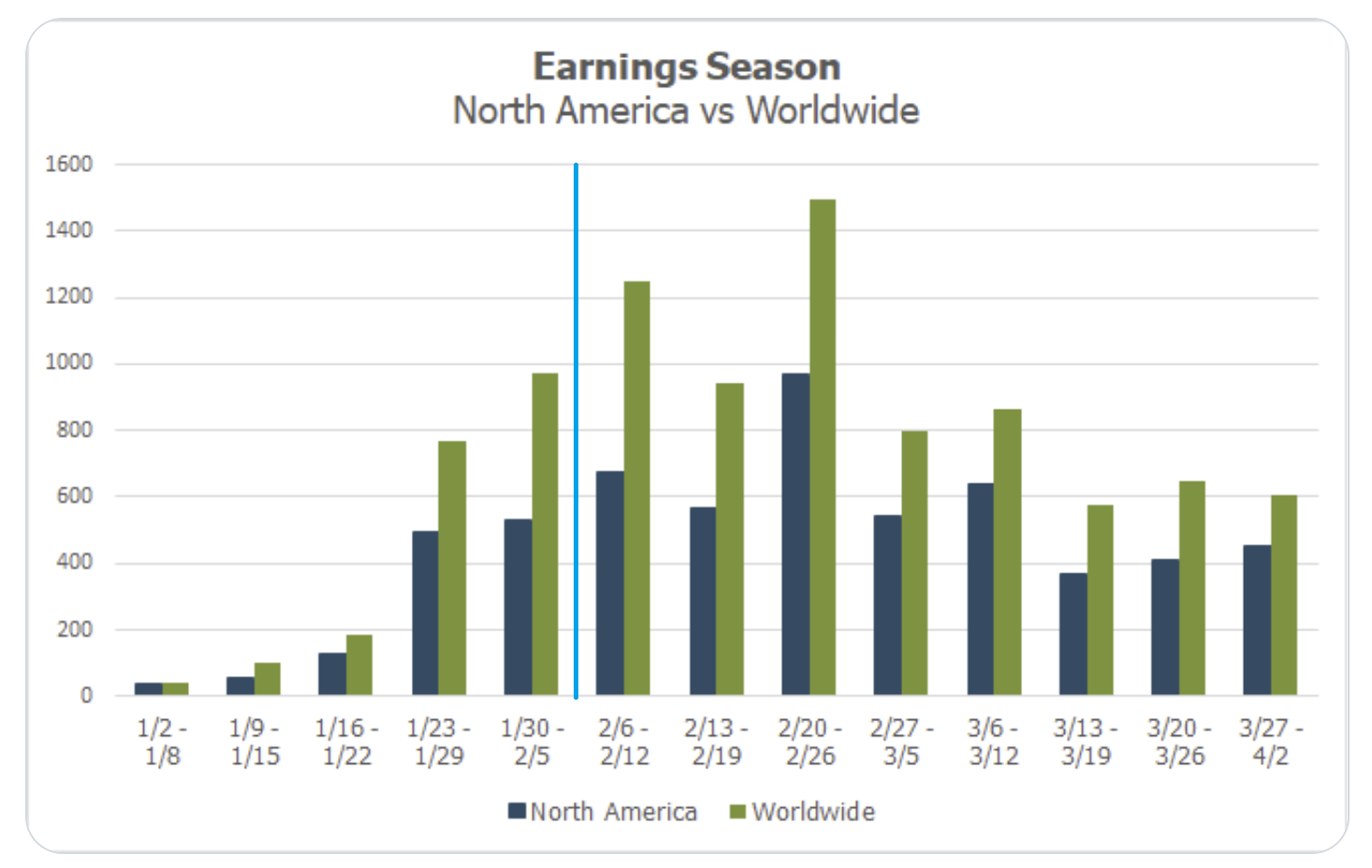

Going forward, despite many index heavy-weights reporting, the earnings season is set to accelerate over the coming weeks, and equity index futures traders have positioned themselves (as evidenced by tight, sideways trade) to react to new information accordingly.

Per JPMorgan Chase & Co (NYSE: JPM) strategists, the bull thesis remains intact.

The pace of economic growth is to stabilize in 2022 and the Federal Reserve is unlikely to move further into the hawkish territory.

We’re “Continuously seeing gains for earnings. Consensus projections for 2022 will most likely prove too low again,” JPM explains. “P/E multiples are elevated, but not equity yields vs credit & bond yields. We expect further, mild and benign, P/E compression in 2022. Overall, the picture is favorable, post the recent de-risking.”

Positioning: Though markets will tend toward instability so long as volatility is heightened and products (especially the index constituents) remain in negative gamma, the dip lower and demand for protection may serve to prime the market for upside (when volatility starts to compress again and counterparties unwind hedges thus supporting any attempt higher).

“Failure to expand the range, lower, on the index level, at least, likely invokes supportive dealer hedging flows with respect to time (‘charm’) and volatility (‘vanna’),” SpotGamma adds.

Taking into account options positioning, versus buying pressure (measured via short sales or liquidity provision on the market-making side), metrics point to “[m]odest bullishness on the 1-month timeframe.”

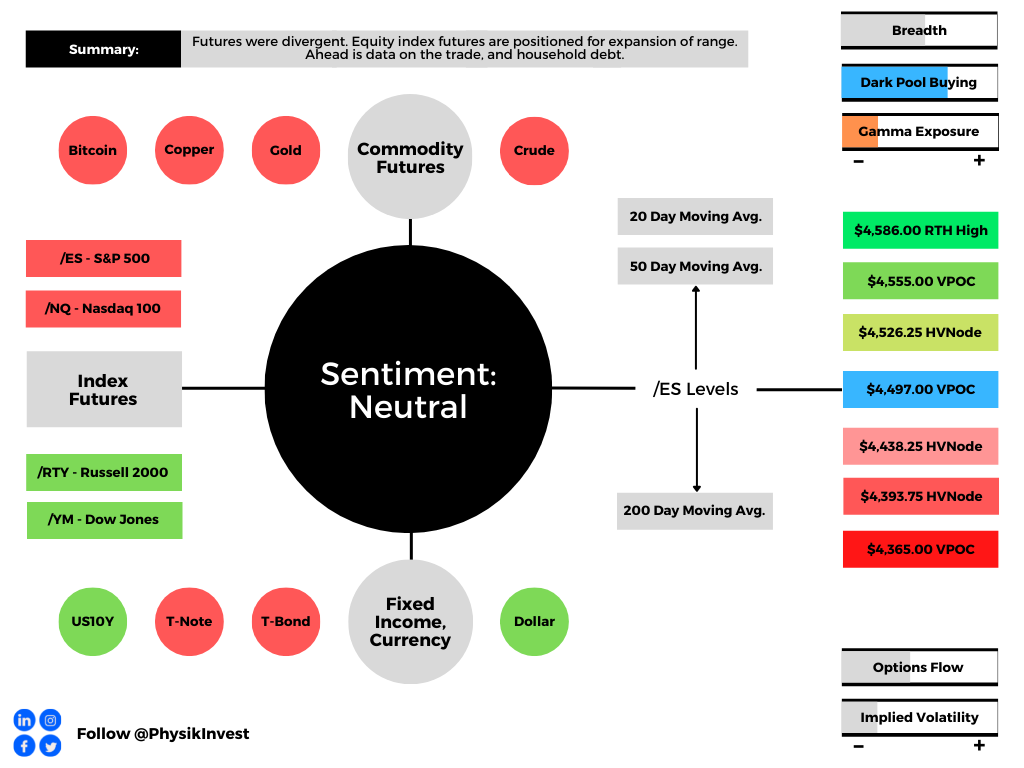

Technical: As of 6:20 AM ET, Tuesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the lower part of a negatively skewed overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

Balance-Break Scenarios: A change in the market (i.e., the transition from two-time frame trade, or balance, to one-time frame trade, or trend) may soon occur. Monitor for acceptance (i.e., more than 1-hour of trade) outside of the balance area. Rejection (i.e., return inside of balance) portends a move to the opposite end of the balance.

In the best case, the S&P 500 trades higher; activity above the $4,497.00 untested point of control (VPOC) puts in play the $4,526.25 high volume area (HVNode). Initiative trade beyond the HVNode could reach as high as the $4,555.00 VPOC and $4,586.00 RTH High (regular trade high), or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,497.00 VPOC puts in play the $4,438.25 HVNode. Initiative trade beyond the $4,438.25 HVNode could reach as low as the $4,393.75 HVNode and $4,365.00 VPOC, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj is also a Benzinga finance and technology reporter interviewing the likes of Shark Tank’s Kevin O’Leary, JC2 Ventures’ John Chambers, FTX’s Sam Bankman-Fried, and ARK Invest’s Catherine Wood, as well as a SpotGamma contributor developing insights around impactful options market dynamics.

Disclaimer

Physik Invest does not carry the right to provide advice.

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.