Abstract

Equity index futures higher. Commodities mixed. Bonds lower. Volatility expanded.

Ahead is a light day of economic releases, in the face of fundamental narratives and positioning metrics that promote less intraday volatility into FOMC.

What Happened

Overnight, equity index futures auctioned sideways to higher as participants seek clarity on the Federal Reserve’s intent to taper asset purchases and hike interest rates.

Ahead is data on Markit manufacturing PMI (9:45 AM ET), as well as the ISM manufacturing index and construction spending (10:00 AM ET).

What To Expect

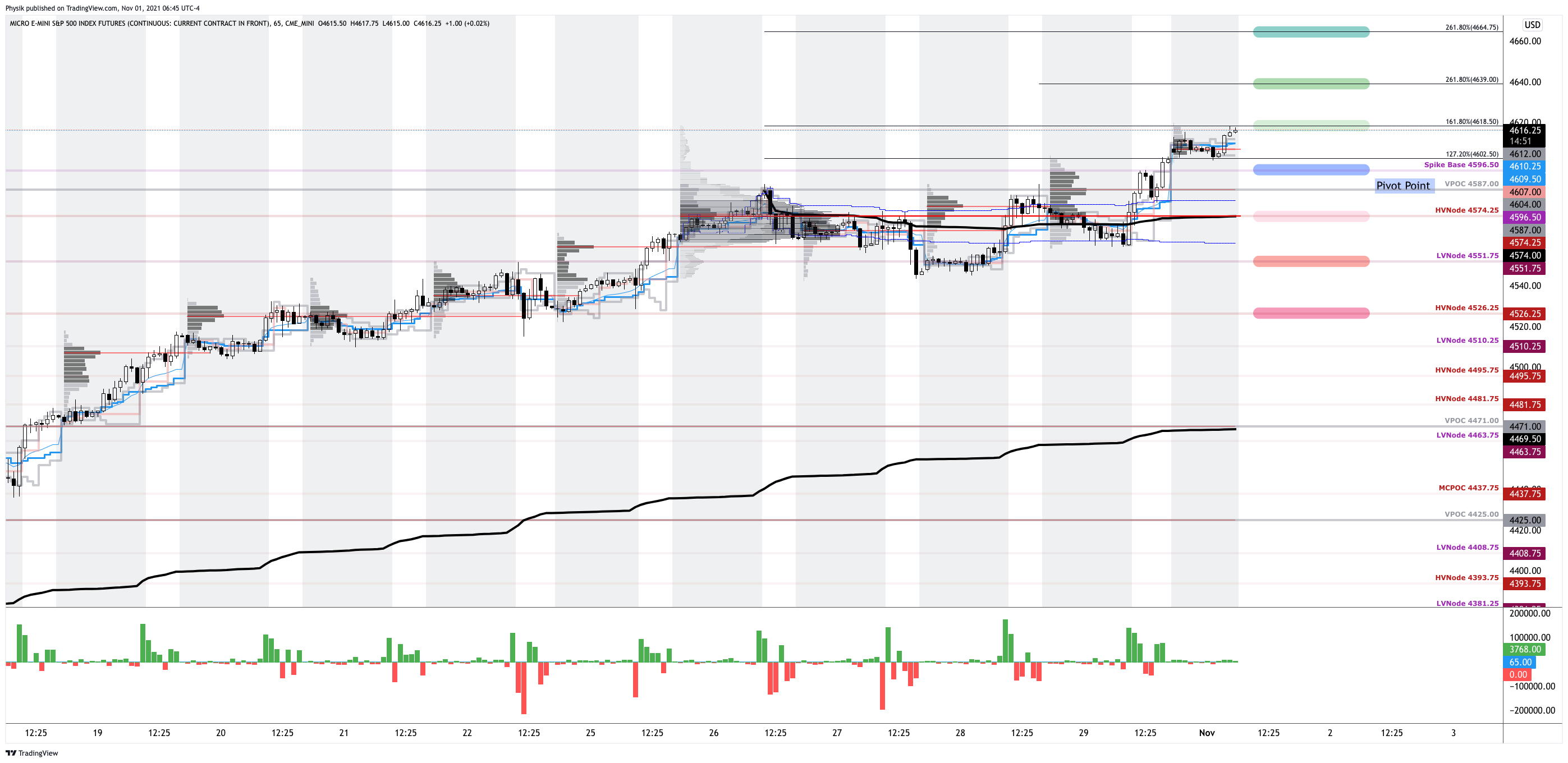

Action: On divergent intraday breadth and market liquidity metrics, the best case outcome occurred, evidenced by a spike away from value in the S&P 500 (INDEX: SPX) (ETF: SPY) (FUTURE: /ES).

Intent: The spike (and overnight gap, out of balance) mark a willingness to continue the trend.

Validation: Sideways to higher trade (above the $4,596.50 spike base) validates the market’s prevailing intent to markup prices ahead of impactful events like this week’s meeting of the Federal Open Market Committee (FOMC).

Consideration: Poor structure left behind prior initiative trade adds to technical instability.

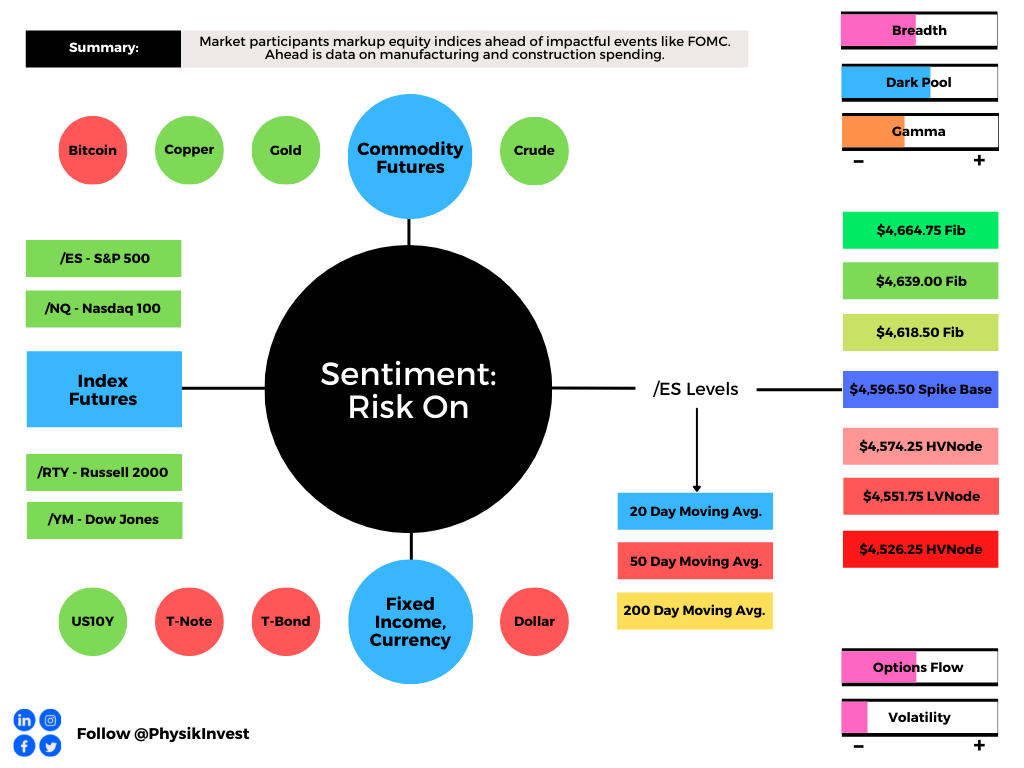

Context: On no substantial change in volume and expansion of range, we see the Nasdaq 100 (INDEX: NDX) (ETF: QQQ) (FUTURE: /NQ) trading strong, relative to its peers.

Given where the S&P 500’s price is in relation to the yellow volume-weighted average price (VWAP) anchored from 9/2/2021, the average buyer, since that date, is in a winning position.

Generally speaking, sideways to higher trade, above the yellow VWAP, puts in play the Fibonacci resistances overhead.

Further, the aforementioned trade is happening in the context of peak growth, in the face of inflation, uncertainty around fiscal policy (with respect to dynamics like the debt ceiling), and increased prospects of tapering to Federal Reserve (Fed) asset purchases.

The implications of these themes on price are contradictory.

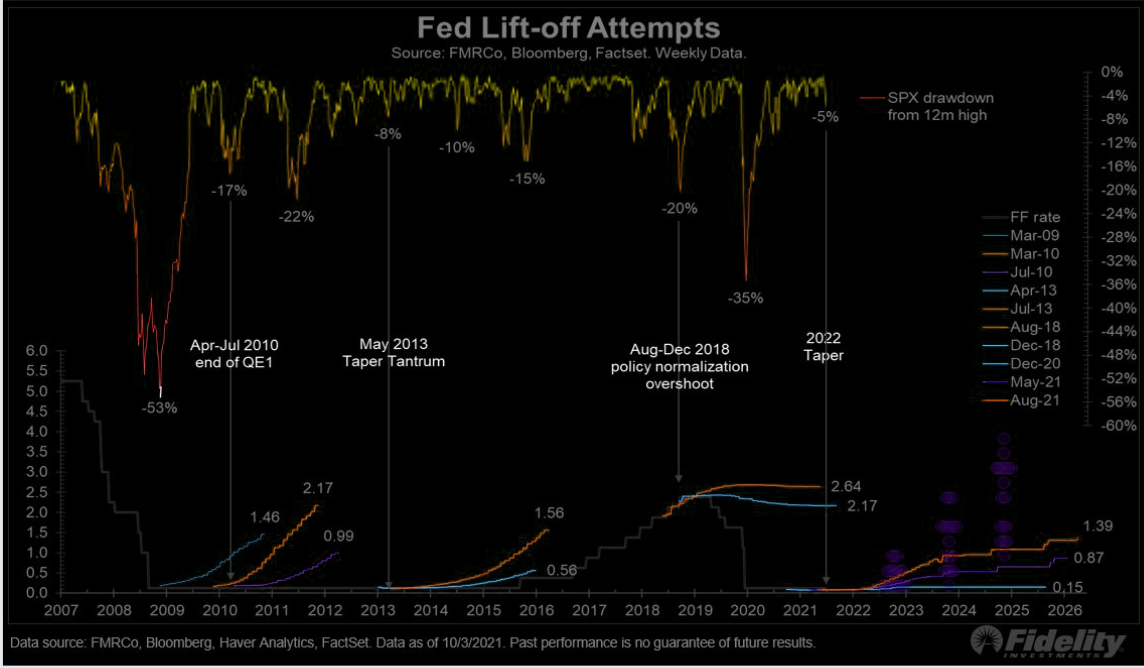

To elaborate, Moody’s expects the Fed to taper its asset purchases in December by $15 billion.

Every single month after, the Fed will continue to reduce purchases by $15 billion with the tapering process expected to be done by mid-2022. Proceeds from maturing assets will be reinvested to prevent balance sheet contraction and rate hikes ought to start in early 2023.

Moody’s notes: “Tapering won’t impact inflation. Though tapering won’t be disinflationary, it could help keep market-based measures of inflation expectations anchored, since tapering is the preamble to the Fed beginning to tighten monetary policy either by allowing its balance sheet to decline and/or by increasing the target range for the fed funds rate.”

In terms of positioning, according to SqueezeMetrics, “middling dark pool sentiment and middling gamma exposure [portends] … 1-month negative returns.”

At the same time, SpotGamma models forecast hedging (by dealers who warehouse options risk) may promote tighter ranges as dealers sell into strength, increasingly. Until event volatility leaves the market, post-FOMC, odds of directional resolve will continue to be limited as higher implied volatility takes away from important dynamics that bolster movement.

Couple that with the intent to normalize policy, the environment “creates a little bit of a challenge for [the] equity market because it does change the drivers of equity performance,” says HSBC Holdings Plc’s (NYSE: HSBC) Joseph Little.

Expectations: As of 6:30 AM ET, Monday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the upper part of a positively skewed overnight inventory, outside of prior-range and -value. This suggests a potential for immediate directional opportunity.

Gap Scenarios: Gaps ought to fill quickly. Should they not, that’s a signal of strength; do not fade. Leaving value behind on a gap-fill or failing to fill a gap (i.e., remaining outside of the prior session’s range) is a go-with indicator. Auctioning and spending at least 1-hour of trade back in the prior range suggests a lack of conviction; in such a case, do not follow the direction of the most recent initiative activity.

In the best case, the S&P 500 trades sideways or higher; activity above the $4,596.50 spike base puts in play the $4,618.50 Fibonacci resistance. Initiative trade beyond $4,618.50 could reach as high as the $4,639.00 and $4,664.75 Fibonacci resistances, or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,596.50 spike base puts in play the $4,574.25 high volume area (HVNode). Initiative trade beyond the HVNode could reach as low as the $4,551.75 low volume area (LVNode) and $4,526.25 HVNode, or lower.

Click here to load today’s updated key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

What People Are Saying

Definitions

Spikes: Spike’s mark the beginning of a break from value. Spikes higher (lower) are validated by trade at or above (below) the spike base (i.e., the origin of the spike).

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

Gamma: Gamma is the sensitivity of an option to changes in the underlying price. Dealers that take the other side of options trades hedge their exposure to risk by buying and selling the underlying. When dealers are short-gamma, they hedge by buying into strength and selling into weakness. When dealers are long-gamma, they hedge by selling into strength and buying into weakness. The former exacerbates volatility. The latter calms volatility.

Balance-Break Scenarios: A change in the market (i.e., the transition from two-time frame trade, or balance, to one-time frame trade, or trend) is occurring.

Monitor for acceptance (i.e., more than 1-hour of trade) outside of the balance area. Rejection (i.e., return inside of balance) portends a move to the opposite end of the balance.

Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

About

After years of self-education, strategy development, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Additionally, Capelj is a Benzinga finance and technology reporter interviewing the likes of Shark Tank’s Kevin O’Leary, JC2 Ventures’ John Chambers, and ARK Invest’s Catherine Wood, as well as a SpotGamma contributor, developing insights around impactful options market dynamics.

Disclaimer

At this time, Physik Invest does not manage outside capital and is not licensed. In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.