Abstract

In sync with bonds, equity index futures were sideways to lower. Commodities were mixed. Volatility expanded.

- Economic growth rate slows 2%.

- Fed may not follow counterparts.

- Increased prospects for volatility.

What Happened

U.S. stock index futures auctioned sideways to lower overnight, within the prior day’s range, as investors looked to price in emerging dynamics with respect to slower growth and inflation, as well as the risks of a taper in asset purchases and a hike in interest rates.

Ahead is data on income, consumer spending, core inflation, and the employment cost index (8:30 AM ET), as well as Chicago PMI (9:45 AM ET), consumer sentiment, and inflation expectations (10:00 AM ET).

What To Expect

Action: During the prior day’s regular trade, on supportive intraday breadth and market liquidity metrics, the best case outcome occurred, evidenced by a spike above current S&P 500 (INDEX: SPX) (ETF: SPY) (FUTURE: /ES) prices.

Intent: The spike marked a willingness to continue the trend.

Validation: Overnight, Thursday’s end-of-day price discovery, away from value, was not validated; after two weeks of markup, participants are likely basing ahead of new information.

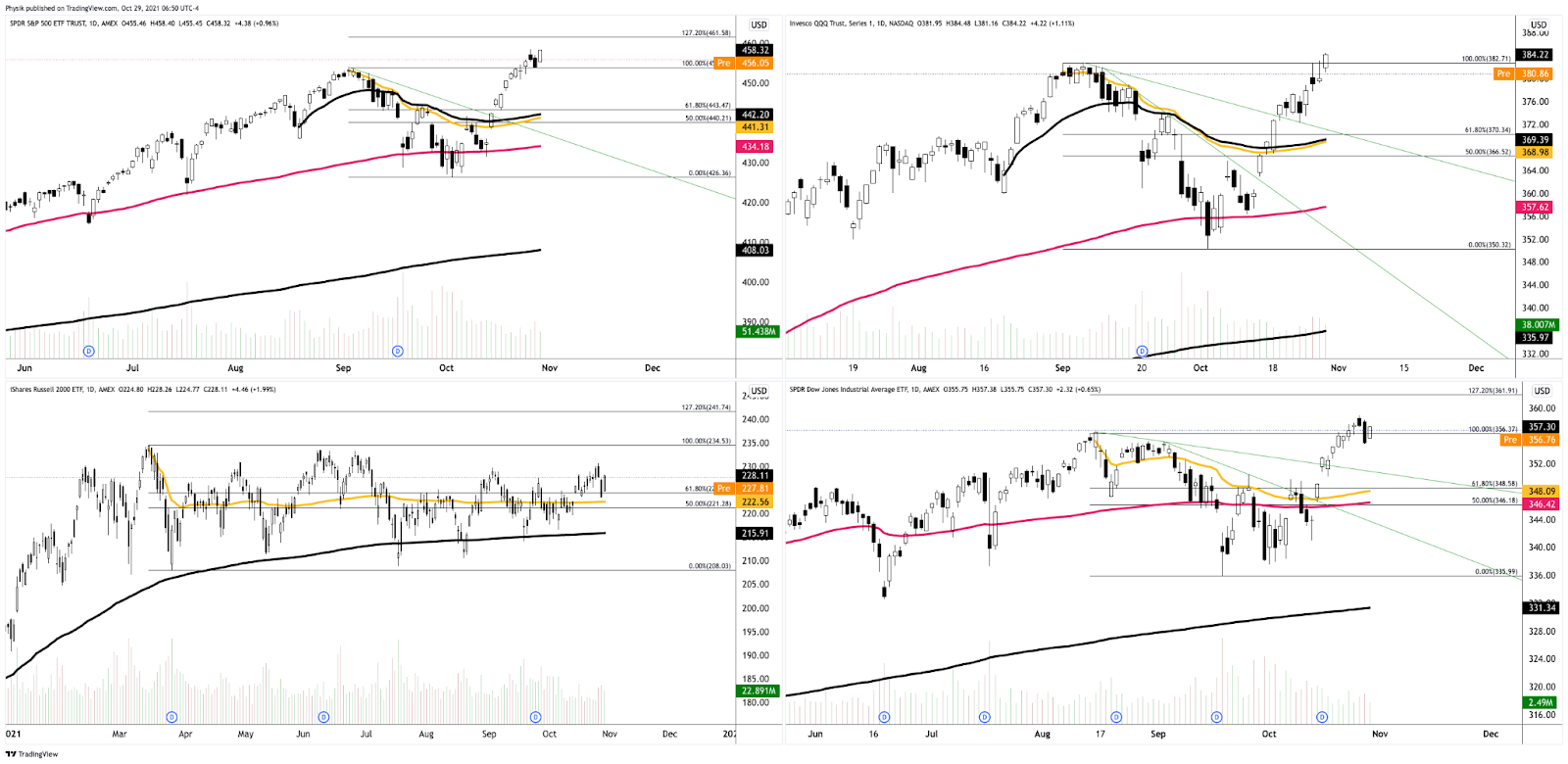

Context: After unimpressive earnings results by Amazon Inc (NASDAQ: AMZN) and Apple Inc (NASDAQ: AAPL), on no substantial change in volume and minimal expansion of range, we see the Nasdaq 100 (INDEX: NDX) (ETF: QQQ) (FUTURE: /NQ) trading weak, relative to its peers.

This comes as three of the major indices (pictured below) struggle to maintain prices above their September peaks.

Still, as evidenced by where the indices are in relation to their yellow volume-weighted average price (VWAP) indicators, the average buyer, since the last major peak, is in a profitable position.

Should indices snap lower, those VWAPs ought to serve as dynamic support levels.

Further, the aforementioned trade is happening in the context of slowing growth, as well as the risks of a taper in asset purchases and a hike in interest rates.

According to a note by The Market Ear, however, JPMorgan Chase & Co’s (NYSE: JPM) Jay Barry believes “Inflation developments have been global in nature and inflation is indeed proving to be less transitory than previously expected.”

“Our understanding of the Fed’s reaction function, as well as our view on likely compositional changes on the FOMC, leads us to believe that the Fed is unlikely to follow its British and Canadian counterparts in raising rates too early simply on inflation concerns.”

In terms of positioning, the CBOE Volatility Index (INDEX: VIX) was higher, while the VIX futures term structure settled in contango, shifting a tad higher across the entire curve. That dynamic, coupled with the long-gamma environment, signals a potential for very near-term stability.

On the other hand, according to SqueezeMetrics analyses, “middling dark pool sentiment and middling gamma exposure [portends] … 1-month negative returns.”

That’s in line with what SpotGamma sees as a potential window for volatility – given OPEX – into next week’s Federal Open Market Committee (FOMC) meeting.

“It’s likely that traders will not look to sell volatility on Monday/Tuesday (pre-Fed) which could bring a pause to this market rise.”

Expectations: As of 7:00 AM ET, Friday’s regular session (9:30 AM – 4:00 PM ET) in the S&P 500 will likely open in the lower part of a negatively skewed overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

Balance-Break Scenarios: A change in the market (i.e., the transition from two-time frame trade, or balance, to one-time frame trade, or trend) may occur. Monitor for acceptance (i.e., more than 1-hour of trade) outside of the balance area. Rejection (i.e., return inside of balance) portends a move to the opposite end of the balance.

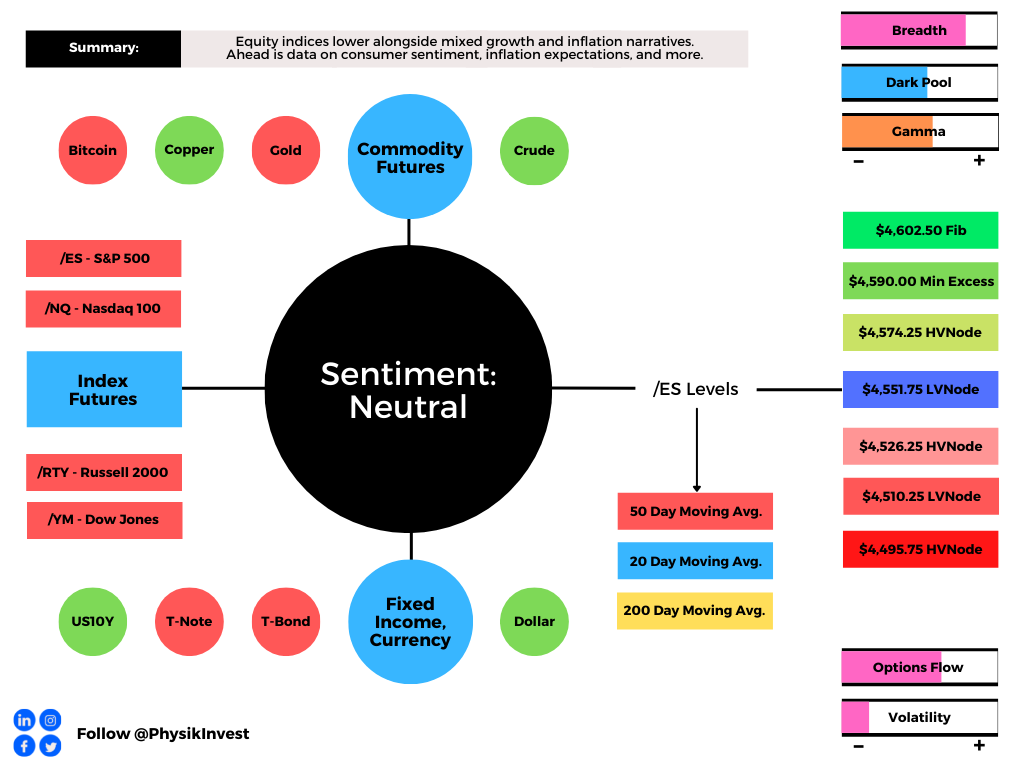

In the best case, the S&P 500 trades sideways or higher; activity above the $4,551.75 low volume area (LVNode) puts in play the $4,574.25 high volume area (HVNode). Initiative trade beyond the $4,574.25 HVNode could reach as high as the $4,590.00 minimal excess high and $4,602.50 Fibonacci extension, or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,551.75 LVNode puts in play the $4,526.25 HVNode. Initiative trade beyond the $4,526.25 HVNode could reach as low as the $4,510.25 LVNode and $4,495.75 HVNode, or lower.

Click here to load today’s updated key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

What People Are Saying

Definitions

Spikes: Spike’s mark the beginning of a break from value. Spikes higher (lower) are validated by trade at or above (below) the spike base (i.e., the origin of the spike).

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

Gamma: Gamma is the sensitivity of an option to changes in the underlying price. Dealers that take the other side of options trades hedge their exposure to risk by buying and selling the underlying. When dealers are short-gamma, they hedge by buying into strength and selling into weakness. When dealers are long-gamma, they hedge by selling into strength and buying into weakness. The former exacerbates volatility. The latter calms volatility.

Options Expiration (OPEX): Traditionally, option expiries mark an end to pinning (i.e, the theory that market makers and institutions short options move stocks to the point where the greatest dollar value of contracts will expire) and the reduction dealer gamma exposure. In recent history, this reset in dealer positioning has been front-run; prior, there was an increase in volatility after the removal of large options positions and associated hedging.

Excess: A proper end to price discovery; the market travels too far while advertising prices. Responsive, other-timeframe (OTF) participants aggressively enter the market, leaving tails or gaps which denote unfair prices.

Volume-Weighted Average Prices (VWAPs): A metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

About

After years of self-education, strategy development, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Additionally, Capelj is a finance and technology reporter. Some of his biggest works include interviews with leaders such as John Chambers, founder and CEO, JC2 Ventures, Kevin O’Leary, businessman and Shark Tank host, Catherine Wood, CEO and CIO, ARK Invest, among others.

Disclaimer

At this time, Physik Invest does not manage outside capital and is not licensed. In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.