The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 300+ that read this report daily, below!

What Happened

Update: Technicals section now reflects the proper overnight inventory stat.

After a week-long or so de-rate to reflect the impact of higher inflation and harsher monetary policies, equity index futures are trading in a responsive fashion.

The S&P 500, in particular, lies pinned against the $3,700.00 high options open interest strike. The large June monthly options expiration has implications on the expansion of the range, as noted in prior letters.

The newsflow remains depressing. Taken alone, you’d think the Federal Reserve (Fed) would be “soft[ly] landing” us into a depression, just in time for WWIII to help us get out of it.

Kidding. The utmost sympathy for those negatively affected by war and economic hardship.

The distinction between the economy and the market is blurred and the drop is the recession. The equity markets are a mechanism pricing the implications of all the points we talk about, in real-time, months (6-12) in advance.

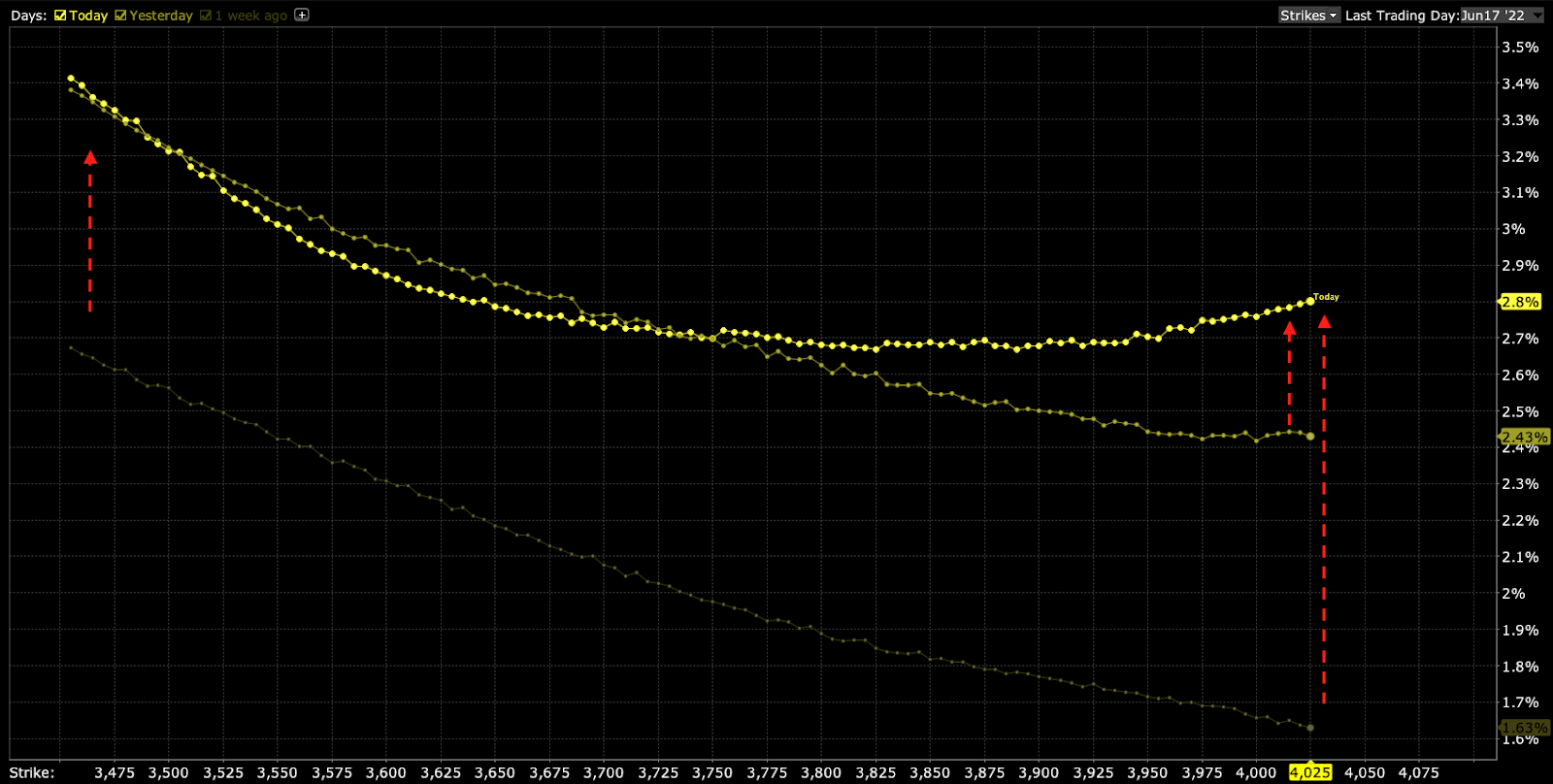

Given that, there are better measures to assess whether a de-rate has played out, fully. In the last session, information, generated by the market – internals, volatility measures, and the like – suggested to us that more selling was in store, all the while there was a definite change in tone in the non-linear strength of volatility and skew with respect to linear changes in price of assets.

Should you care for the narratives in news, then here it is:

The Bank of England (BOE) pointed to the potential for a more aggressive rate hike schedule if data were to reflect a wage spiral. The Swiss National Bank (SNB) upped rates an unexpected 50 basis points. The White House weighed fuel-export limits. Both residential permitting and housing starts plummeted with the 30-year fixed-rate breaching 6.00%.

Adding, U.S. junk bond spreads topped 500 basis points for the first time since 2020, and China, also, launched its third most modern aircraft carrier.

Ahead, Fed Chair Jerome Powell speaks at 8:45 AM ET. Then updates on industrial production and capacity utilization (9:15 AM ET), as well as leading economic indicators (10:00 AM ET).

What To Expect

Team. We’re going to have to keep it a bit shorter, today, and leave out the fundamentals section. Sorry!

Read: Daily Brief for June 16, 2022, on monetary updates and the implications of positioning.

In a nutshell, and this is borrowing from a past post-Federal Open Market Committee (FOMC) event letter, as well put forth by Kai Volatility’s Cem Karsan, on a Fed day, “the first move tends to be structural. A function of the inevitable rebalancing of dealer inventory post-event.”

“The second move and final resolution, if you wait for it, is usually tied to the incremental effects on liquidity (QE/QT).”

Essentially, the baseline bear trend held because, essentially, the Fed is, indeed, expected to continue raising rates and withdrawing liquidity. This will prompt a continued de-rate with QT being “a direct flow of capital to capital markets.”

Great, moving on. What’s next?

Essentially, with the June monthly options expiration (OPEX), expected is a roll-off of a large amount of customer negative delta exposure (via put options they own). Taken in a vacuum, with expiration, liquidity providers (who are short put options and short underlying to hedge) will re-hedge (buyback static short-delta, among other things), and this is taken as bullish.

However, this is definitely discounting the impact on delta from participants rolling forward their bets on direction.

As talked about yesterday, we were to gauge the delta impact by how far below the high open interest strikes the equity indexes were to travel. As stated, these options, have little time to expiry and, thus, their gamma (the sensitivity of the option to change indirection) grows rather large, at near-the-money strikes.

As the time to expiry narrows, above the strike in question delta decays, and counterparts buy back their static delta hedges.

As the time to expiry narrows, below the strike in question delta expands and counterparts sell more static delta to hedge.

This means that if far below these high-interest strikes, associated hedging, less any new reach for protection would keep markets pressured. If above, hedging, less new sales of protection, would bolster markets higher.

Ultimately, if lower, all else equal, the June 17 OPEX will coincide with the removal of the in-the-money options exposures in question. Negating the rollover of exposures and leaving the door open to some delta imbalance (need to buy to re-hedge exposure) suggests that after this expiration, markets may have less pressure to rally against.

“The SPX index quarterly option notional is higher than usual, but the market is below the concentration of risk given the recent selloff,” Tanvir Sandhu, chief global derivatives strategist at Bloomberg Intelligence, wrote in a note. “Price action will reflect the economic context, but flows from expiring in-the-money hedges may support the market.”

What do you do with this information?

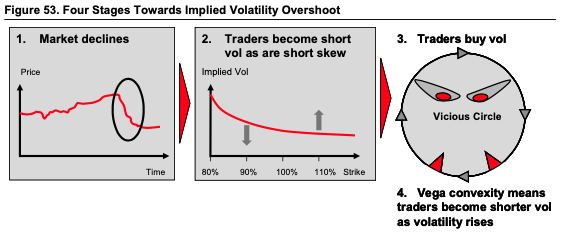

Well, recall that we’ve talked ad nauseam about the supply and demand of volatility, as well as how that impacted the volatility realized (RVOL) and implied (IVOL) by the market.

Essentially there was an “absolute slamming” (i.e., sale of options), particularly in shorter-dated tenors and this played into the generally poor performance in skew, hence our comments on the benefit to buying into implied skew convexity should volatility reprice.

Basically, participants are hedged and volatility remains well-supplied.

To hedge or capitalize on a potential reach for protection, amid forced selling or demand for protection by a greater share of the market in ways not recently seen, then the repricing in those structures would be a boon to those that own them.

To quote Benn Eifert of QVR Advisors: “Skew goes up if vol outperforms the skew curve a lot on a selloff.”

And, as touched on in this morning’s introduction, there was a definite change in tone in the non-linear strength of volatility and skew with respect to linear changes in the price of assets.

Personally, I, along with a partner who I trade closely with, saw increases in the prices of ratio structures (long or short one option near-the-money, short or long two or more further out-of-the-money) by hundreds of percent for only a few basis points of change in the indexes.

As Karsan explained online, there was “a spike in short-dated -sticky skew, [the] first we’ve seen since [the] secular decline began and it hints [at] a potentially critical change in dealer positioning [and] the distribution of underlying outcomes.”

“We’re transitioning to a fat left tail, right-based distribution.”

So why does any of this matter?

This is a validation of our perspectives on how one should position, given what the supply and demand of volatility looked like prior.

Options have a “non-zero second-order price sensitivity (or convexity) to a change in volatility,” as Mohamed Bouzoubaa et al explain well in the book Exotic Options and Hybrids.

“ATM vanillas are [not] convex in the underlying’s price, … but OTM vanillas do have vega convexity … [so], when the holder of an option is long vega convexity, we say she is long vol-of-vol.”

In other words, by owning that protection, you are positioned to monetize on a continued non-linear repricing of volatility. However, doing this in a manner that cuts decay (when nothing happens) is the difficult part.

Read: Trading Volatility, Correlation, Term Structure and Skew by Colin Bennett et al. Originally sourced via Academia.edu.

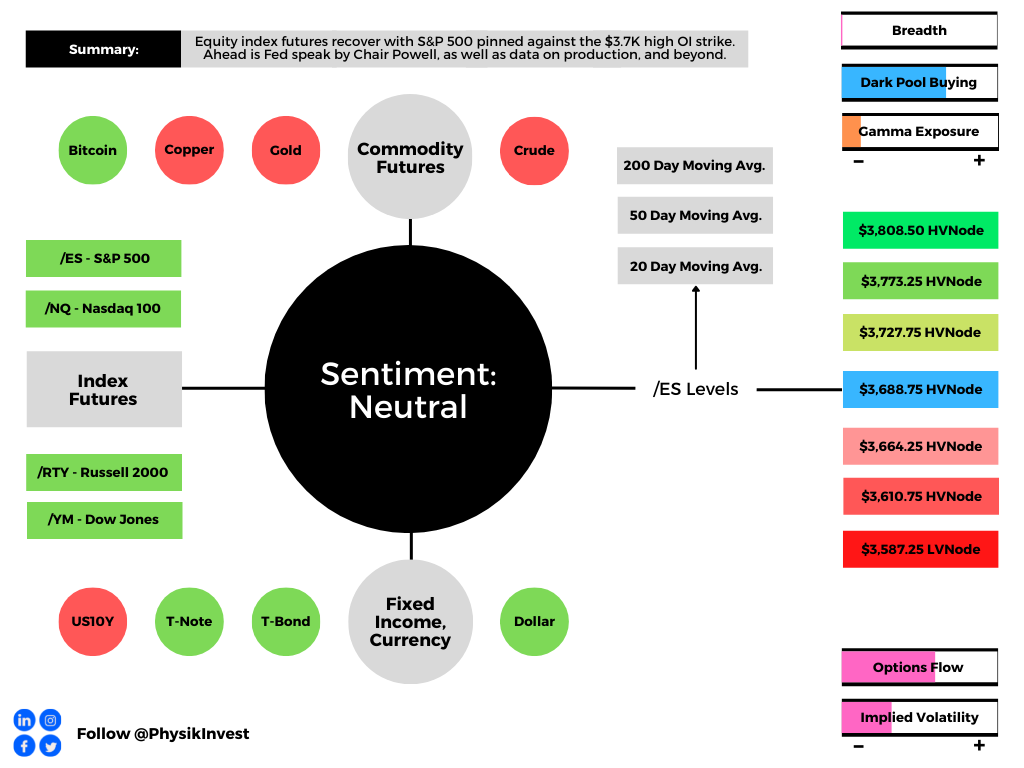

Technical: As of 6:30 AM ET, Friday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the lower part of a positively skewed overnight inventory, inside of prior-range and -value, suggesting a potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher; activity above the $3,688.75 HVNode puts in play the $3,727.75 HVNode. Initiative trade beyond the $3,727.75 HVNode could reach as high as the $3,773.25 HVNode and $3,808.50 HVNode, or higher.

In the worst case, the S&P 500 trades lower; activity below the $3,688.75 HVNode puts in play the $3,664.25 HVNode. Initiative trade beyond the $3,664.25 HVNode could reach as low as the $3,610.75 HVNode and $3,587.25 LVNode, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Definitions

Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

Some of his works include conversations with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, FTX’s Sam Bankman-Fried, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, among many others.

Disclaimer

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.

2 replies on “Daily Brief For June 17, 2022”

[…] Detailed was Friday, June 17’s commentary that honed in on some of the implications of pre- and post-Federal Reserve meeting […]

[…] Positioning: To preface, I encourage everyone to check out the Daily Brief for June 17, 2022. […]