The Daily Brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 200+ that read this report daily, below!

What Happened

Overnight, equity index futures diverged during participants’ attempt to discover higher prices.

Commodities were mixed while bonds extended their slump; central bank authorities, in an effort to rein in inflation amid rising prices, are focused on implementing tighter monetary policies.

For a moment, the (5-30) Treasury curve dropped below zero for the first time since 2006. This is after the Federal Reserve’s (Fed) Jerome Powell said last week the central bank was committed to upping borrowing costs and would hike by 50 basis points if needed.

What To Expect

Fundamental: Keeping it short, today.

Last week, we discussed monetary policy and the impact of quantitative tightening (QT) in the face of revisions in global growth expectations. You can check that out, here.

On the belief that the “Fed hiking cycle and balance sheet drain are now priced” as the market enters a seasonally favorable period, strategists like JPMorgan Chase & Co’s (NYSE: JPM) Marko Kolanovic favor risk in high-beta.

“While the commodity supercycle will persist,” Kolanovic said, “the correction in bubble sectors is now likely finished, and geopolitical risk will likely start abating in a few weeks’ time (while a comprehensive resolution may take a few months).”

Complicating Kolanovic’s outlook is uncertainty with respect to the Fed’s decision to hike and pare asset holdings as financial conditions tighten.

In the coming weeks, the thesis that a de-rate (or pricing in of uncertainties) has played out will be put to the test as the Fed reveals its template for QT. Final plans are likely to be unveiled in an announcement at the beginning of May.

Damped Spring Advisors’ Andy Constan explains well his perspectives on what comes next in the below video. Check it out.

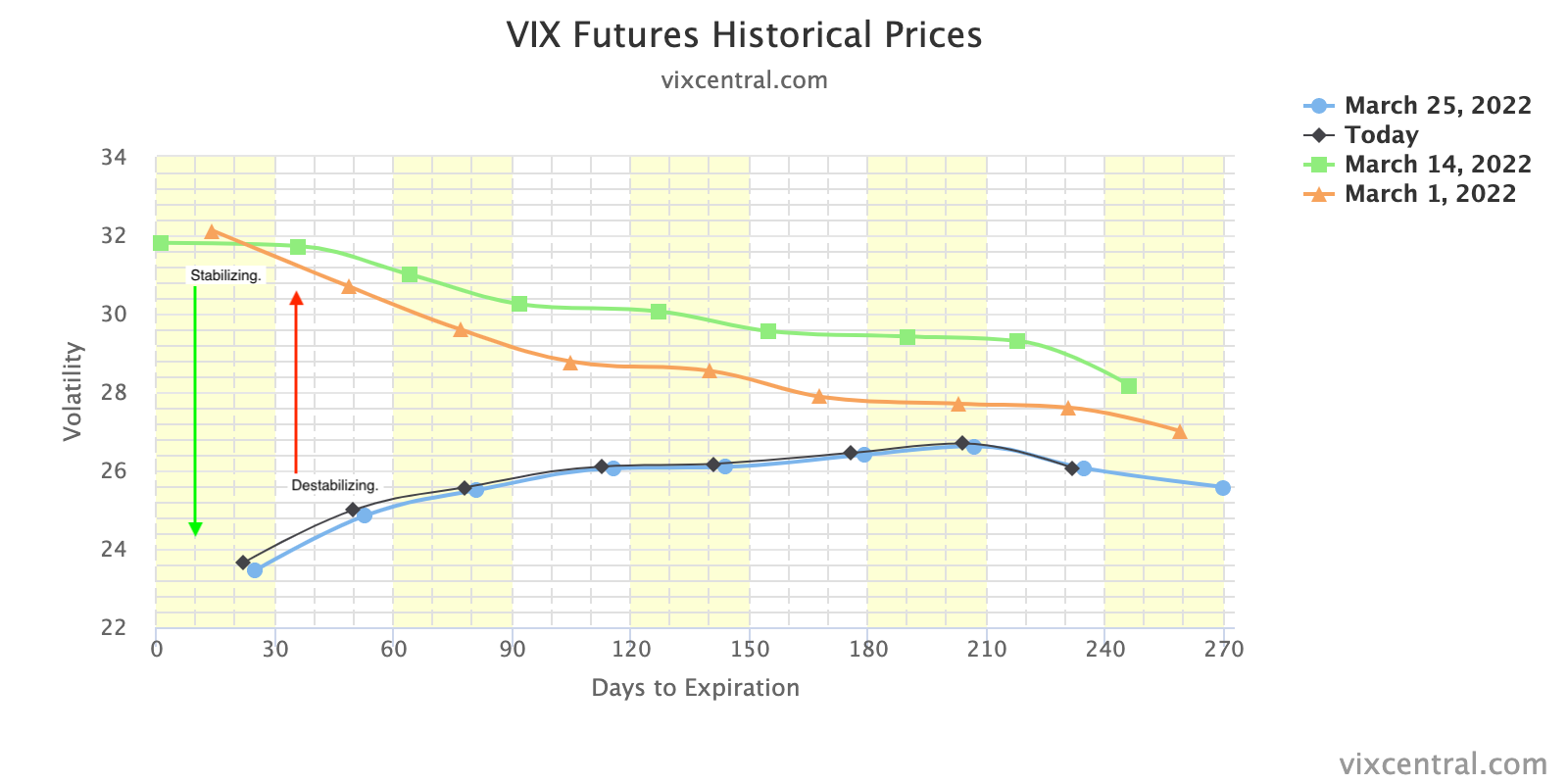

Positioning: The CBOE Volatility Index (INDEX: VIX), a measure of participants’ demand for protection, so to speak, appears to have hit a lower bound around 20.00. This is as the VIX term structure steepened, dramatically, over the last weeks, particularly at the front end of the curve.

After a long period during which options market participants concentrated their activity on bets on lower prices (negative delta trades that payout in case of movement lower), markets jolted higher as that protection was monetized (and decay ensued).

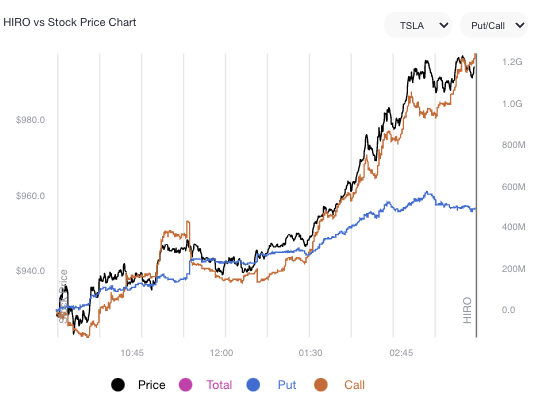

Alongside this collapse in implied volatility was speculative demand in index heavy-weights like Tesla Inc (NASDAQ: TSLA). Participants bought stock while selling puts (bets on the downside) and buying calls (bets on the upside).

As this speculative demand cools, counterparties to these levered bets on the upside unwind their hedges and this has the effect of pressuring attempts higher.

According to SpotGamma, this is as, heading into this week’s expiration of quarterly options, there’s a “potential for more ‘pinning’ action as close-to-the-money bets concentrated in that expiry near the end of their lifecycle.” You can learn more about this, here.

Why? As time and volatility trend toward zero, the rate of change of options delta (gamma) of near-the-money options increases.

“This happens because the range of spot prices across which option deltas shift from near-zero to near-100% becomes very narrow as options approach maturity (and at maturity, options on one side of the settlement value have zero delta and the other side have 100% delta).”

With, at least at the index level, bets on lower volatility dominating (put and call selling), as the gamma of these near-the-money options increases, counterparties add liquidity, buying (selling) into weakness (strength) as positive delta exposure falls (rises).

Moreover, the odds point to sideways trade, rather than a fast move higher or lower.

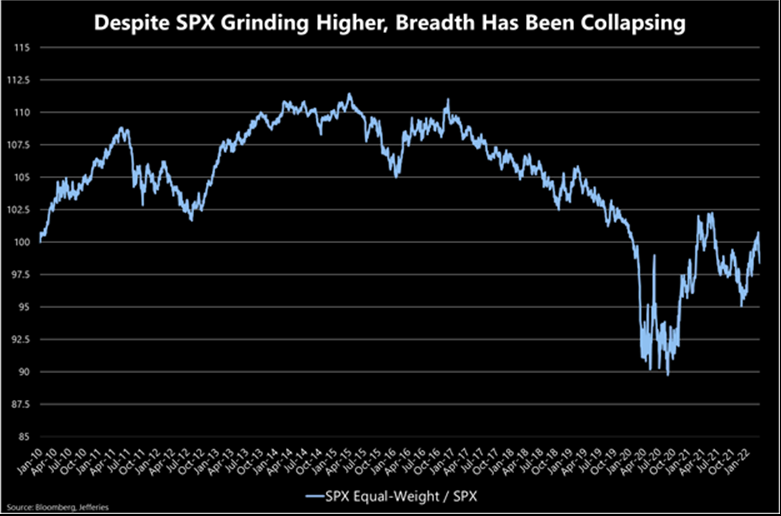

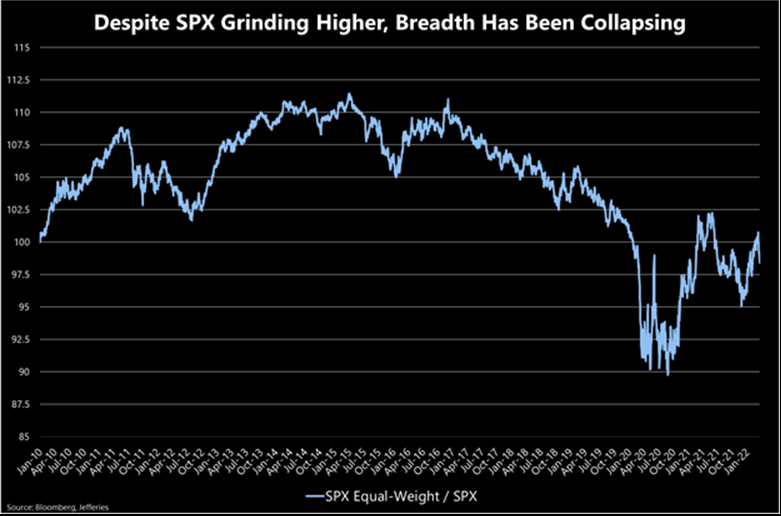

However, after this expiry, it’s likely that the market succumbs to underlying forces. At present, despite the S&P 500 and its peers trading higher, underlying breadth is collapsing.

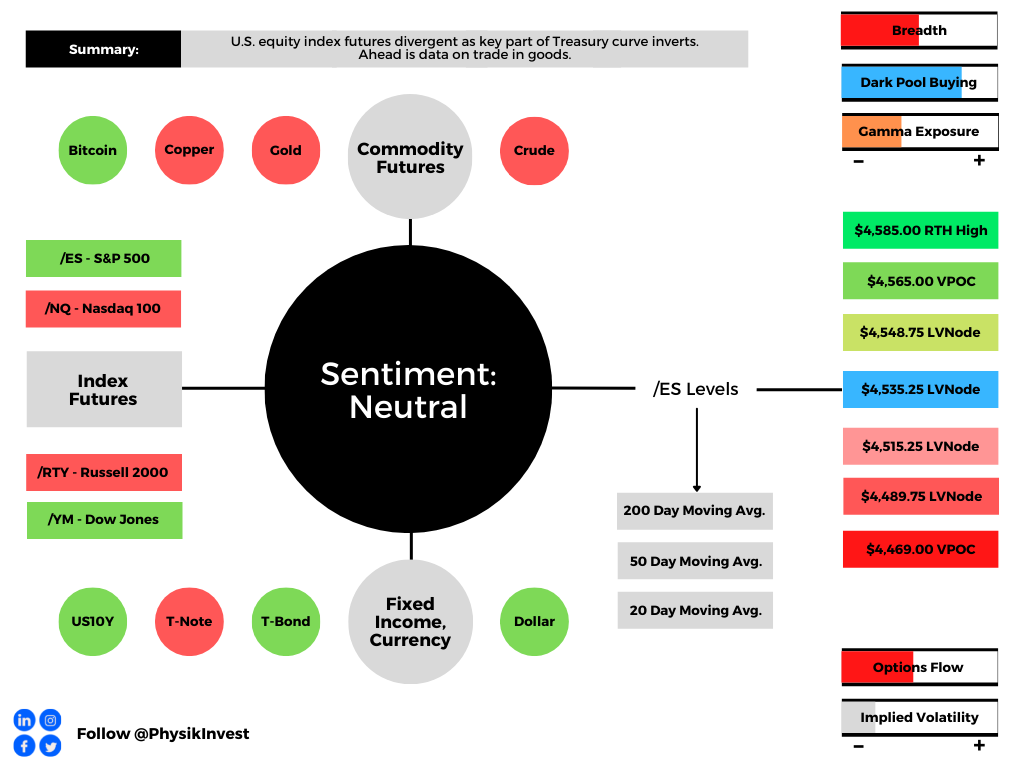

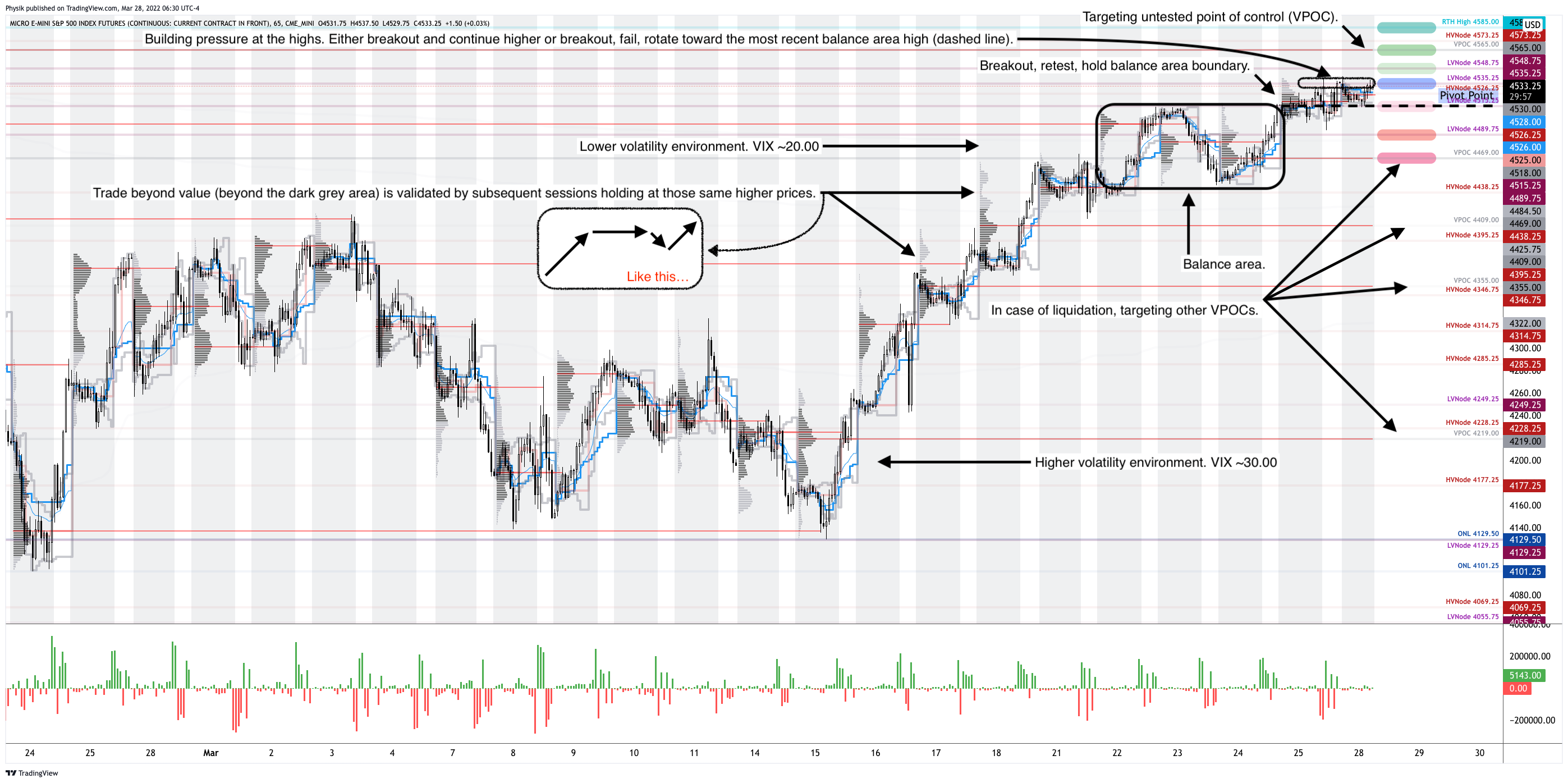

Technical: As of 6:40 AM ET, Monday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the upper part of a balanced overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher; activity above the $4,535.25 low volume area (LVNode) puts in play the $4,548.75 LVNode. Initiative trade beyond the $4,548.75 LVNode could reach as high as the $4,565.00 untested point of control (VPOC) and $4,585.00 regular trade high (RTH High), or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,535.25 LVNode puts in play the $4,515.25 LVNode. Initiative trade beyond the $4,515.25 LVNode could reach as low as the $4,489.75 LVNode and $4,469.00 VPOC, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

What People Are Saying

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

Balance (Two-Timeframe Or Bracket): Rotational trade that denotes current prices offer favorable entry and exit. Balance areas make it easy to spot a change in the market (i.e., the transition from two-time frame trade, or balance, to one-time frame trade, or trend).

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

Some of his works include conversations with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, FTX’s Sam Bankman-Fried, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, among many others.

Disclaimer

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.