Physik Invest’s Daily Brief is read by thousands of subscribers. You, too, can join this community to learn about the fundamental and technical drivers of markets.

Fundamental

Apologies for the delayed send. Please be subscribed to our Substack to receive updates sooner every day!

Last week, we added to our discussion on the “non-linear shocks” keeping inflation above target. In short, these shifts are not good for portfolio constructions like 60/40.

Moreover, in a January 6 Credit Suisse (NYSE: CS) follow-up, Zoltan Pozsar provided what he thinks may be a more optimal portfolio construction: 20% cash, 40% stocks, 20% bonds, and 20% commodities.

“[T]his ain’t your parents’ global macro environment,” Pozsar put forth, adding that some of the crises impacting the stability of money stem from the crisis of inflation “driven by mother nature and geopolitics.” Consequently, central banks’ responses may not be good for risk assets.

Amid a re-shaping of global flows (i.e., lower demands for the US dollar and Treasury securities), the Federal Reserve (Fed) may focus on backstopping bonds; if the usual marginal buyer won’t buy, in the context of geopolitical events, Treasuries may be at risk of tailing in auctions, which could, then, drive volatility in equities, credit, and EM.

By the end of 2023, the solution may be quantitative easing (QE) under the guise of yield curve control (YCC); QE will happen in the context of dysfunction in the Treasury markets, and seek to “police swap spreads at high levels of interest rates, not depress yields [and] inflate risk assets.”

Technical

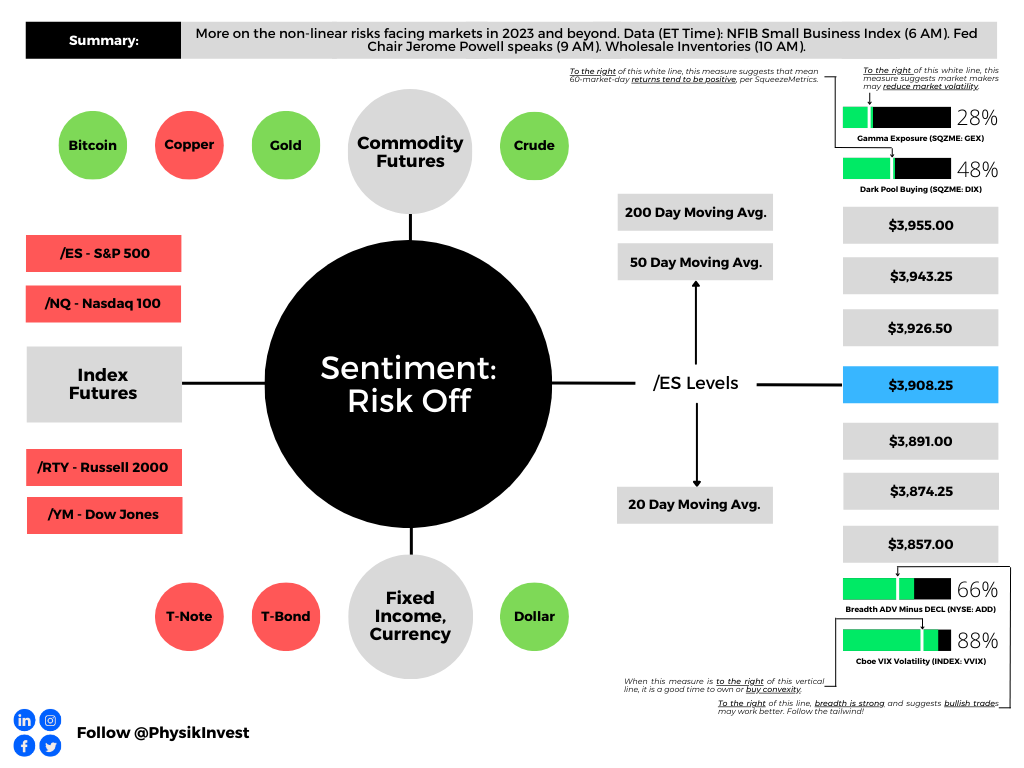

As of 6:45 AM ET, Tuesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the lower part of a negatively skewed overnight inventory, outside of prior-range and -value, suggesting a potential for immediate directional opportunity.

Our S&P 500 pivot for today is $3,908.25.

Key levels to the upside include $3,926.50, $3,943.25, and $3,955.00.

Key levels to the downside include $3,891.00, $3,874.25, and $3,857.00.

Click here to load today’s key levels into the web-based TradingView platform. All levels are derived using the 65-minute timeframe. New links are produced, daily.

As a disclaimer, the S&P 500 could trade beyond the levels quoted in the letter. Therefore, you should load the above link on your browser for more relevant levels.

Definitions

Volume Areas: Markets will build on areas of high-volume (HVNodes). Should the market trend for long periods of time, it will be identified by low-volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants auction and find acceptance in an area of a prior LVNode, then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: Denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: Denote areas where two-sided trade was most prevalent over numerous sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

About

In short, an economics graduate working in finance and journalism.

Capelj spends most of his time as the founder of Physik Invest through which he invests and publishes daily analyses to subscribers, some of whom represent well-known institutions.

Separately, Capelj is an equity options analyst at SpotGamma and an accredited journalist interviewing global leaders in business, government, and finance.

Past works include conversations with investor Kevin O’Leary, ARK Invest’s Catherine Wood, FTX’s Sam Bankman-Fried, Lithuania’s Minister of Economy and Innovation Aušrinė Armonaitė, former Cisco chairman and CEO John Chambers, and persons at the Clinton Global Initiative.

Contact

Direct queries to renato@physikinvest.com or Renato Capelj#8625 on Discord.

Calendar

You may view this letter’s content calendar at this link.

Disclaimer

Do not construe this newsletter as advice. All content is for informational purposes.