Physik Invest’s Daily Brief is read by thousands of subscribers. You, too, can join this community to learn about the fundamental and technical drivers of markets.

Administrative

On December 23, 2022, issued was an in-depth trade recap. Check it out here. Adding, in that recap, shortly after release, your letter writer found he made a mistake in the ~11th paragraph. The incorrect greeks were listed, and that issue has been fixed online. Apologies.

Fundamental

Last week, the Bank of Japan’s (BoJ) Governor Haruhiko Kuroda sparked a rise in the yen and a fall in domestic US bonds, potentially ahead of some policy normalization.

Japanese government bond yields can rise 0.5% versus 0.25% after a change to the BoJ’s yield-curve control policy, a tool used to fight the persistent “stagnation,” per Andreas Steno Larsen’s letter.

“Whatever the BOJ calls this, it is a step toward an exit,” said Masamichi Adachi, chief Japan economist at UBS Group AG (NYSE: UBS) Securities. “This opens a door for a possible rate hike in 2023,” and no more negative interest rates.

This development is not that good for so-called carry trades, as Bloomberg explained, “in which investors borrow in cheaper currencies to finance purchases of higher-yielding peers,” or, even, equities and other risk assets.

The yen was a popular funding currency. It may not be any longer if this “is the first step towards tightening,” wrote Brown Brothers Harriman strategists, though the BoJ said, yesterday, this was “definitely not a step toward an exit,” with Steno Larsen adding QE “actually increased by 25%.”

Though “higher yields at home [in Japan] could mean less investment” from Japan, Bloomberg said, US stock and bond flows after the news hit suggest the carry trade may not be as impactful, to add.

Some, like Steno Larsen, conclude concerns, albeit warranted, may be overblown; in mid-2023, global inflation pressures likely “fade[] sufficiently to allow BoJ to resume its dovish stance,” all the while on recession fears, a “Fed pause or pivot is ultimately what will bring the Japanese lifers and pension funds back to the US Treasury table and a reversal of the USDJPY trade.”

So what?

Liquidity, though appearing positive amid an “empty[ing of] the TGA (Treasury General Account) … ahead of the debt ceiling [cross]-over,” is on a downward trajectory into the second and third quarters, after which “a pivot from the Fed [prompts] … a disinflation rally.”

So, per Steno Larsen, markets go sideways to higher to start the year and, then, down. Therefore, favor “having some equity beta” heading into 2023.

Position in “sectors that can swallow a simultaneous drop in the ISM and CPI on a relative basis … [include] utilities, health care, and staples.”

Technical

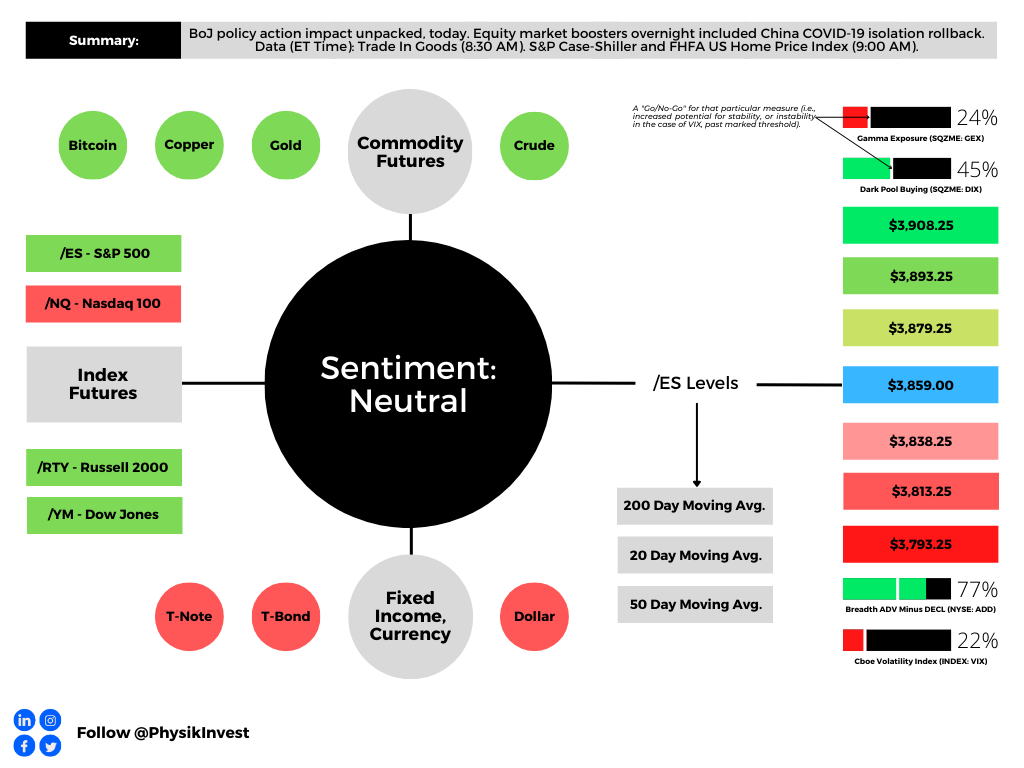

As of 8:55 AM ET, Tuesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the lower part of a balanced overnight inventory, just inside of the prior-range and -value, suggesting a limited potential for immediate directional opportunity.

Our S&P 500 pivot for today is $3,859.00.

Key levels to the upside include $3,879.25, $3,893.75, and $3,908.25.

Key levels to the downside include $3,838.25, $3,813.25, and $3,793.25.

Click here to load today’s key levels into the web-based TradingView platform. All levels are derived using the 65-minute timeframe. New links are produced, daily.

Definitions

Volume Areas: Markets will build on areas of high-volume (HVNodes). Should the market trend for long periods of time, it will be identified by low-volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants auction and find acceptance in an area of a prior LVNode, then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: Denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: Denote areas where two-sided trade was most prevalent over numerous sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

Definitions

Volume Areas: Markets will build on areas of high-volume (HVNodes). Should the market trend for long periods of time, it will be identified by low-volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants auction and find acceptance in an area of a prior LVNode, then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: Denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: Denote areas where two-sided trade was most prevalent over numerous sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

About

In short, an economics graduate working in finance and journalism.

Capelj spends most of his time as the founder of Physik Invest through which he invests and publishes daily analyses to subscribers, some of whom represent well-known institutions.

Separately, Capelj is an equity options analyst at SpotGamma and an accredited journalist interviewing global leaders in business, government, and finance.

Past works include conversations with investor Kevin O’Leary, ARK Invest’s Catherine Wood, FTX’s Sam Bankman-Fried, Lithuania’s Minister of Economy and Innovation Aušrinė Armonaitė, former Cisco chairman and CEO John Chambers, and persons at the Clinton Global Initiative.

Contact

Direct queries to renato@physikinvest.com or Renato Capelj#8625 on Discord.

Calendar

You may view this letter’s content calendar at this link.

Disclaimer

Do not construe this newsletter as advice. All content is for informational purposes.