Physik Invest’s Daily Brief is read by thousands of subscribers. You, too, can join this community to learn about the fundamental and technical drivers of markets.

Technical

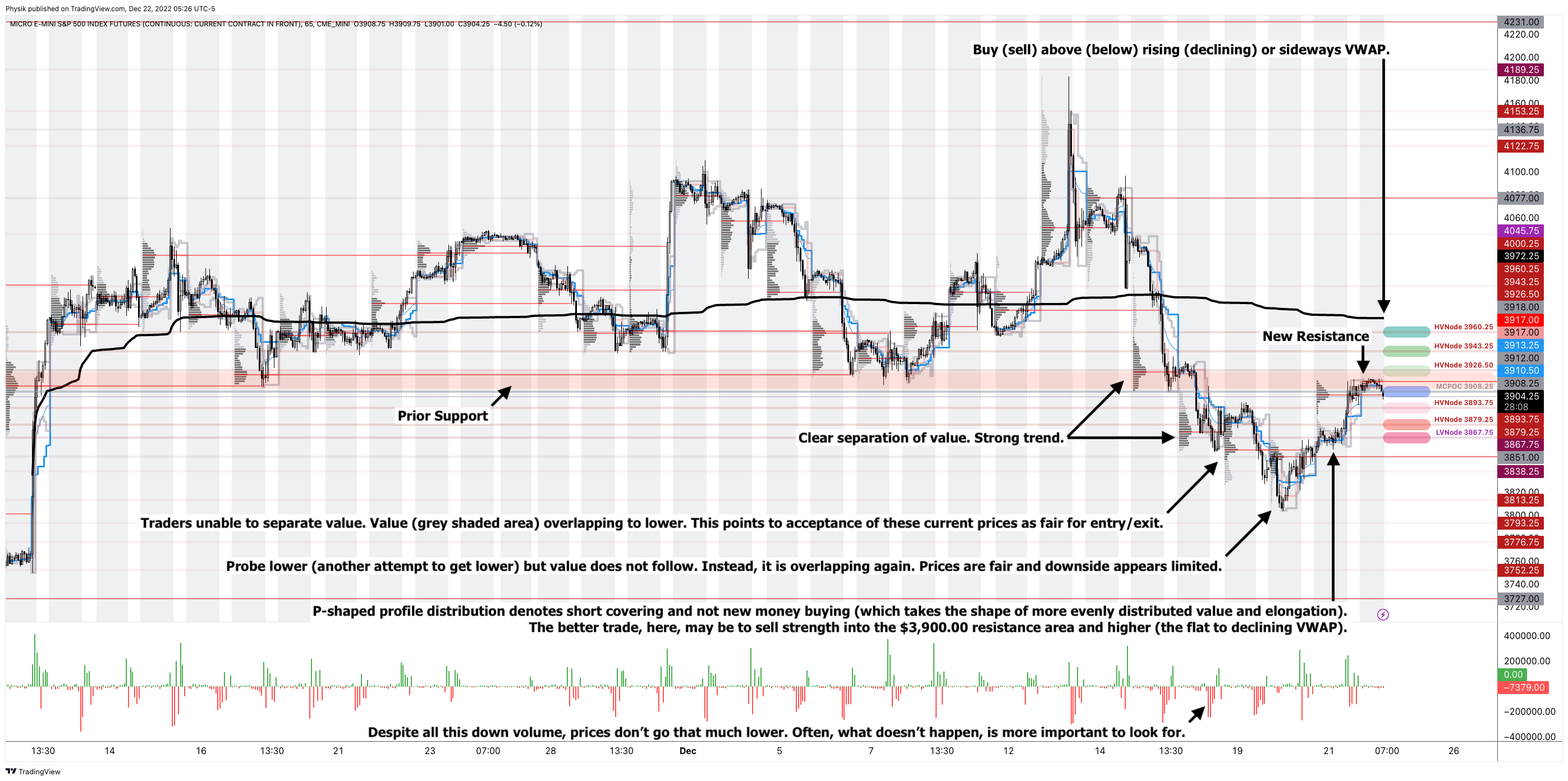

As of 5:30 AM ET, Thursday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the lower part of a balanced overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

Our S&P 500 pivot for today is $3,908.25.

Key levels to the upside include $3,926.50, $3,943.25, and $3,960.25.

Key levels to the downside include $3,893.75, $3,879.25, and $3,867.75.

Click here to load today’s key levels into the web-based TradingView platform. All levels are derived using the 65-minute timeframe. New links are produced, daily.

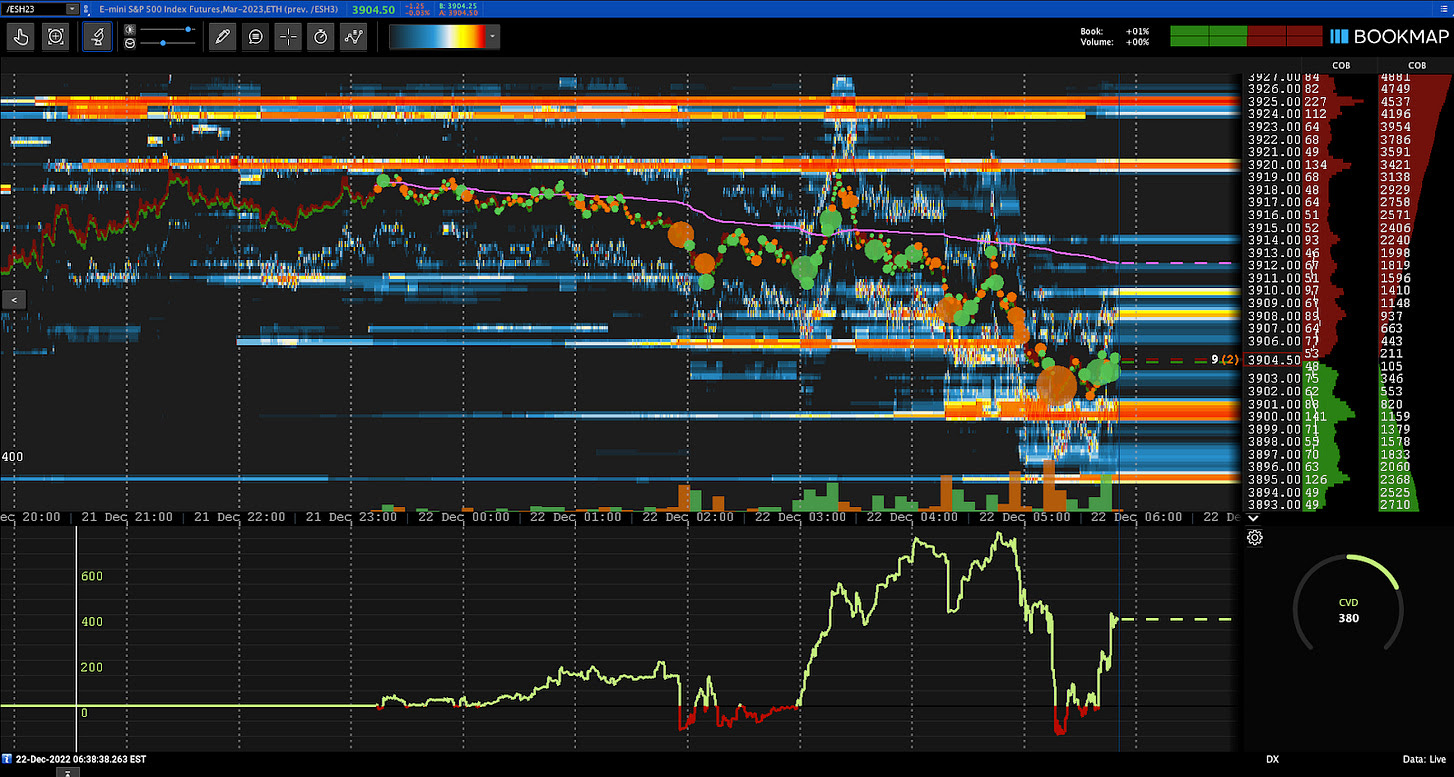

Checking Bookmap, a tool that allows us to visualize market liquidity, today, we see orders near the $3,920.00 – $3,925.00 area in the E-mini S&P 500 (FUTURE: /ES). These are orders to enter or exit trades at the resistance area highlighted in the 65-minute profile chart above.

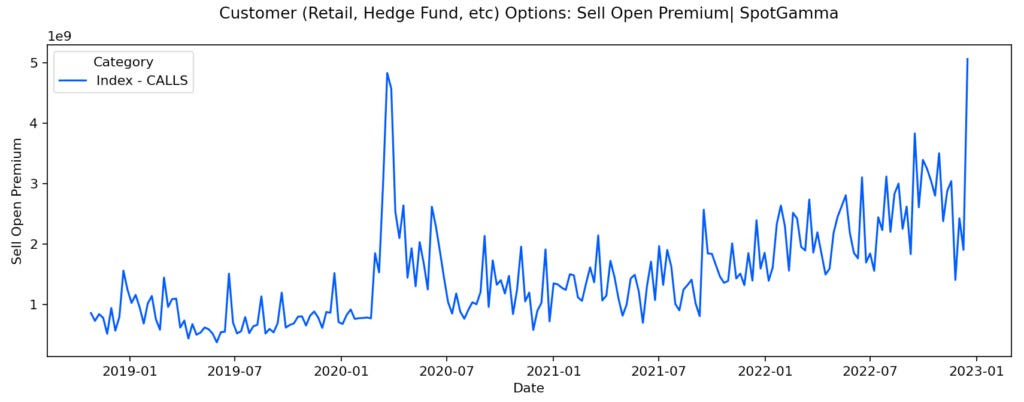

Considerations: Traders may have noticed responsiveness near key-technical areas visually discernable on a chart. In the Daily Brief for December 21, we discussed the positioning contexts to blame for this. After big events last week, an absence of the unexpected (i.e., what traders sought to hedge and/or bet on) prompted the sale of options protection, a pressure on options prices.

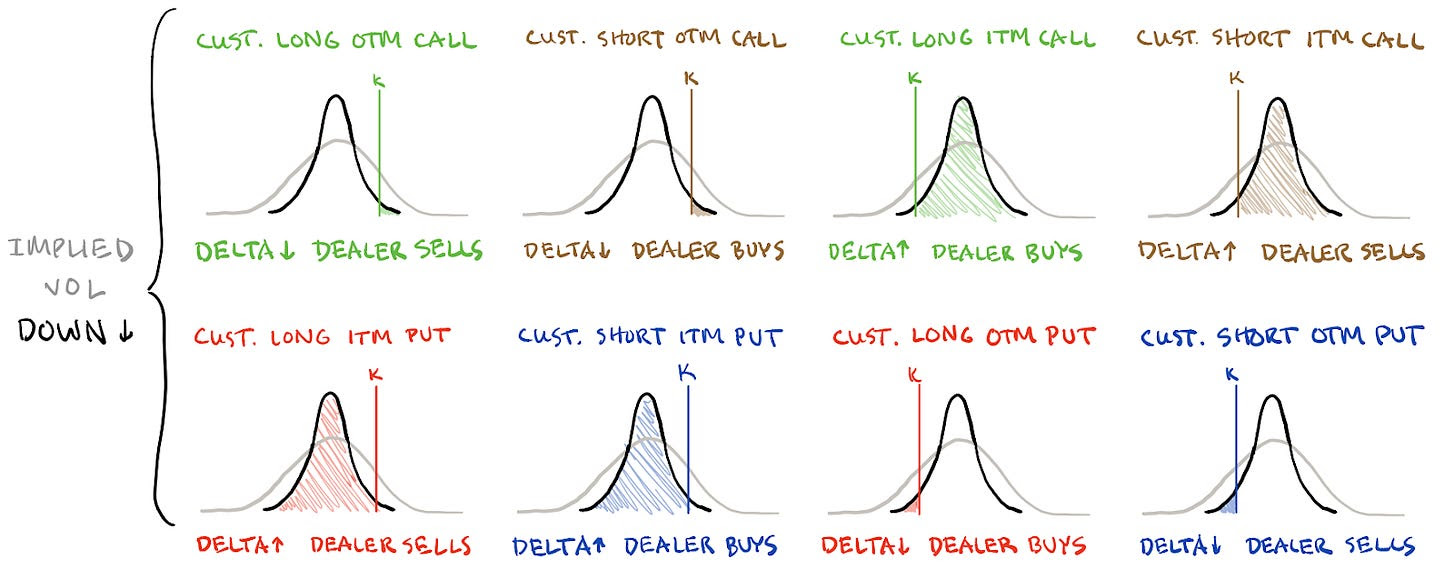

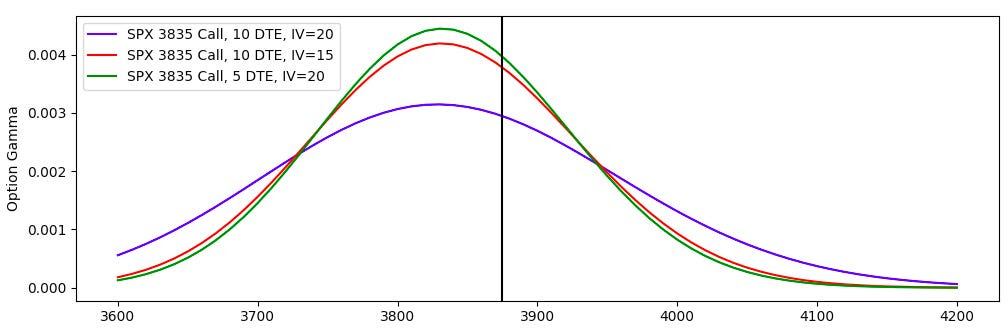

As a result, the S&P 500 is sliding into lower levels of fixed-strike and top-line implied volatility (IVOL) measures. Given the current positioning, when IVOL is on a downward trajectory, counterparties sell strength and buy weakness. For instance, there is a ton of short-call open interest at the $3,835.00 strike. Customers are (mainly) short these calls. Dealers (on the other side) sell underlying to re-hedge their rising positive Delta exposure from the in-the-money call. This mutes movement.

This more positive Delta is a consequence of IVOL falling and Gamma (sensitivity to movement) rising. A higher Gamma implies a more variable Delta and, hence, less stable directional risk.

Basically, as IVOL falls, the extrinsic or time value (theta) of the option falls and, given that in this case, the option is in the money, its intrinsic value (Delta) rises.

While this is happening (i.e., orderly index selling and lower IVOL), big constituents like Tesla Inc (NASDAQ: TSLA) are swinging far more amid traders’ uneasiness and bets, there.

Weakness under the hood, relative to the indexes, and responsiveness to very minute technical levels won’t last; yes, in the interim, you may lean on these levels provided. Again, however, don’t expect that to last.

IVOL is performing poorly and that’s resulted in investors moving to better-performing strategies including short volatility. As a consequence, the broader market is in a less-well-hedged position. Coupled with the removal of the index-level support contexts (i.e., positioning that’s promoting responses to key areas) and some exogenous catalysts, we could see higher realized volatility (RVOL) and less immunity from the weaknesses happening under the hood in single stocks, in the new year.

Definitions

Volume Areas: Markets will build on areas of high-volume (HVNodes). Should the market trend for long periods of time, it will be identified by low-volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants auction and find acceptance in an area of a prior LVNode, then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

MCPOCs: Denote areas where two-sided trade was most prevalent over numerous sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

About

In short, an economics graduate working in finance and journalism.

Capelj spends most of his time as the founder of Physik Invest through which he invests and publishes daily analyses to subscribers, some of whom represent well-known institutions.

Separately, Capelj is an equity options analyst at SpotGamma and an accredited journalist interviewing global leaders in business, government, and finance.

Past works include conversations with investor Kevin O’Leary, ARK Invest’s Catherine Wood, FTX’s Sam Bankman-Fried, Lithuania’s Minister of Economy and Innovation Aušrinė Armonaitė, former Cisco chairman and CEO John Chambers, and persons at the Clinton Global Initiative.

Contact

Direct queries to renato@physikinvest.com or Renato Capelj#8625 on Discord.

Calendar

You may view this letter’s content calendar at this link.

Disclaimer

Do not construe this newsletter as advice. All content is for informational purposes.