The Daily Brief is a free market report read by over 1,200 people.

Administrative

Setting the stage for what we will unpack further later this week. Mainly key talking points, today, coupled with a few aesthetic changes, if you have not noticed already (e.g., graphic above).

Fundamental

A less eventful couple of days, albeit uncertainty remains. On the geopolitical front, an easing of conflict appeared with Biden and Xi stressing their need to get ties back on track. That is adding to Russia’s withdrawal from Kherson, Ukraine.

Regarding crypto, a focus for some of last week’s letters, the happenings are awing. Allegedly FTX “transferred billions of dollars in customer assets to their trading firm Alameda,” Substack newsletter Market Sentiment had written.

“Of the $16 billion that customers had deposited into FTX, close to $10 billion was transferred over to Alameda … using its own coin FTT as collateral for borrowing the real coins deposited by customers, … [and this meant that the scheme] heavily depended on the value of FTT.”

As a an aside, we will soon feature a conversation with a former emerging FX and yields trader at Goldman Sachs Group Inc (NYSE: GS) who now works in DeFi. We will unpack the recent volatility, its driver, and follow-on implications.

Here’s one quote:

“For example, look at what happened in the UK with the pension funds and margin calls. That is a classic DeFi strategy. You take your bonds and borrow cash against them. Then, you put it back into bonds and loop it a couple of times. That way, you have a leveraged interest rate exposure. That’s the same principle of lending staked ETH, borrowing ETH, and doing it a couple of times.”

It was allegations about the firms’ relationship, as well as allegations by competitors, that ultimately incited an implosion and bankruptcy. In short, per his posts on betting and Kelly criterion, founder Sam Bankman-Fried (SBF) showed a risk tolerance “far outside” the normal.

For more on the debacle, check out the Daily Brief published on November 10, 2022, as well as the letter published on November 9, 2022.

The aforementioned is in light of liquidity being “sucked out of the market,” said Fabian Wintersberger; a continued “withdrawal of liquidity might lead to a real, systemic crisis in conventional financial markets,” which we’ve pondered before.”

Positioning

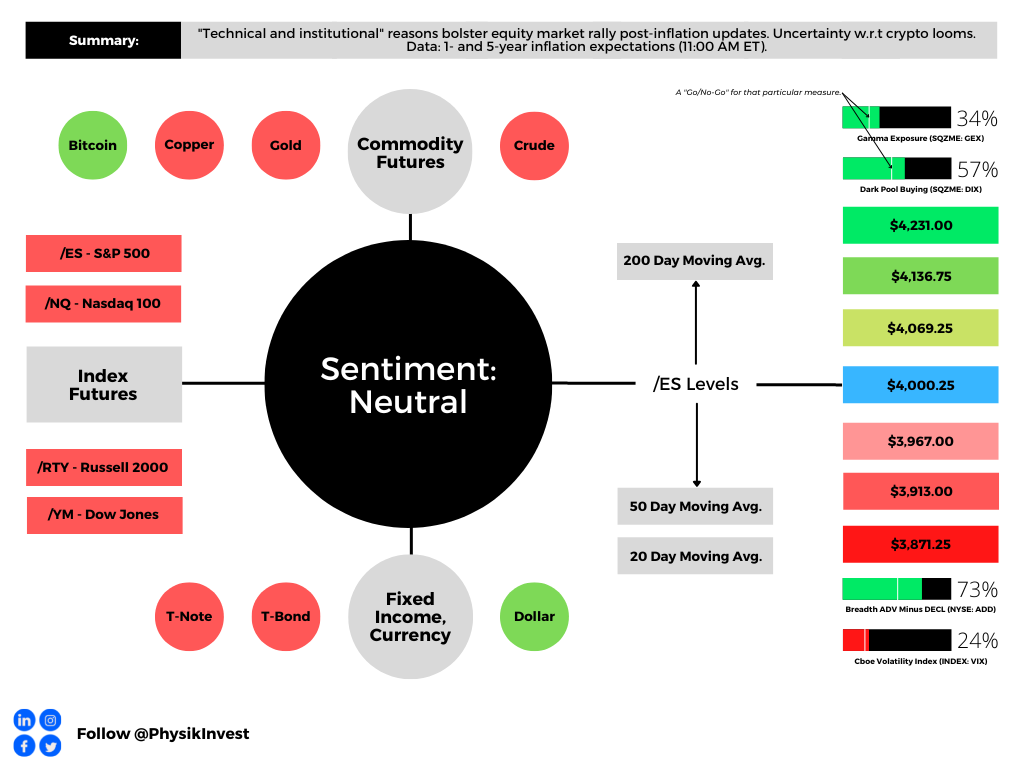

Markets have rallied, recently. In short, as we talked about before and, now, fellow letter writers, including Alfonso Peccatiello of The Macro Compass, confirm, the pace of the market’s rally is, in part, the result of “technical and institutional reasons.”

In our letters last week, we said the compression of implied volatility, evidenced by a shift lower in the volatility term structure, particularly at the front end where options are most sensitive, was to add to any macro-type repositioning, with follow-on buying support coming from the reach for “Deltas and leverage” to the upside (call options).

Peccatiello offers an interesting explanation: “[A]t this point of the year incentive schemes drive people to be much more willing to pay and chase upside.” Preferred are the “convex structures” that would benefit from “outsized” rallies. In traders’ monetization of put protection they owned, as well as reach for upside calls (to not miss out on a potential reversal), skew is at lows and, if the assumption is that “further tightening monetary policy and draining liquidity off the market might cause some problems down the road,” per Wintersberger, bets that pay when markets trade lower are attractive.

Adding, a big takeaway, though not discussed explicitly above (but in past letters), we’ll see a loss of structural support from hedging flows; ultimately, the very poor hedging that’s going on, heading into the next rally, is going to set the stage for a large tail. Traders, who aren’t as well hedged, will seek protection and this will pressure markets, adding to any macro-type selling.

In the coming letters, we’ll go into more detail and discuss how to structure a new trade on this information, such as the one unpacked in a recent case study of ours.

Technical

As of 7:45 AM ET, Monday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the middle part of a balanced overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

Our S&P 500 pivot for today is $4,000.25.

Key levels to the upside include $4,069.25, $4,136.75, and $4,231.00.

Key levels to the downside include $3,967.00, $3,913.00, and $3,871.25.

Click here to load today’s key levels into the web-based TradingView platform. All levels are derived using the 65-minute timeframe. New links are produced, daily.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga journalist.

His works include private discussions with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, the infamous Sam Bankman-Fried of FTX, ex-Bridgewater Associate Andy Constan, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, the Lithuanian Delegation’s Aušrinė Armonaitė, among many others.

Contact

Please direct your queries to renato@physikinvest.com or Renato Capelj#8625 on Discord.

Disclaimer

Do not construe the materials herein as advice. All content is for informational purposes only.