What Happened

Equity index futures auctioned sideways alongside no new fundamental catalysts.

Ahead is data on retail sales and import prices (8:30 AM ET), industrial production and capacity utilization (9:15 AM ET), the NAHB home builders’ index, and business inventories (10:00 AM ET), as well as Fed-speak at 12:00 and 2:30 PM ET.

What To Expect

On minimally divergent intraday breadth and unsupportive market liquidity metrics, the best case outcome occurred, evidenced by the balance and overlap of value areas in the S&P 500.

This activity, which marks a potential willingness to continue balance, is adding strength to poor structure, a dynamic that is helping clear the market of technical instabilities.

Context: According to Morgan Stanley (NYSE: MS), the S&P 500 ought to be weighed down by slower earnings growth and rising yields. The firm’s chief U.S. equity strategist explains that risk and reward for broad indices look unattractive.

“[W]e think 2022 will finally bring the multiple compression we incorrectly forecasted for 2H 2021. Our 12-month target P/E of 18x is 15% below current levels but in line with the 5-year average and the top quintile for the past 30 years.”

“The risk of de-rating has been deferred, not avoided, and makes our 12-month S&P 500 Bear/Base/Bull targets of 3900/4400/5000 unexciting.”

This comes alongside expectations that inflation – a product of strong demand – is likely to worsen but not disrupt deflationary trends, such as increased moneyness of nonmonetary assets, innovation, and the like.

Moreover, in terms of positioning, the CBOE Volatility Index (INDEX: VIX) was a touch higher, while demand came in across the front area of the VIX futures term structure.

Obviously, the tone has changed a bit since last week; customer demand and exposure to very short-dated put protection declined. This was most noticeable in how the VIX term structure behaved over the past sessions. After shifting outward (mostly) in the front, a sign of demand for short-dated protection, the curve shifted back down, late last week.

So, while the initial pop (and hedging on the part of those dealers that warehouse customer options orders) was destabilizing, the term structure slid back into line and the removal of that short-dated protection had the effect of leading dealers to buy back short stock/futures hedges.

This stabilized the market.

Thereafter, the market drifted back up to the level at which positive options gamma is highest, ahead of a fast-approaching monthly options expiration (OPEX). Into OPEX, dealers’ positive exposure to the risks of price movement, based on predominant positioning in the S&P, ought to increase. In hedging this exposure, dealers ought to supply the market with liquidity (i.e., sell stock/futures) which ought to dampen upside volatility.

So, presently, we’re in a bind and things ought to loosen after OPEX, allowing fundamental catalysts to play a bigger role in price discovery.

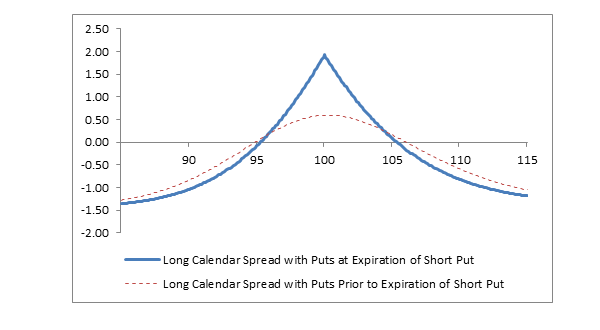

A way to play this dynamic is to structure some sort of options spread that applies the proceeds from a short option (which capitalizes on pinning and the rapid decay of soon-to-expire options) toward a long option further out in time. Learn about basic Calendar Spreads or see below.

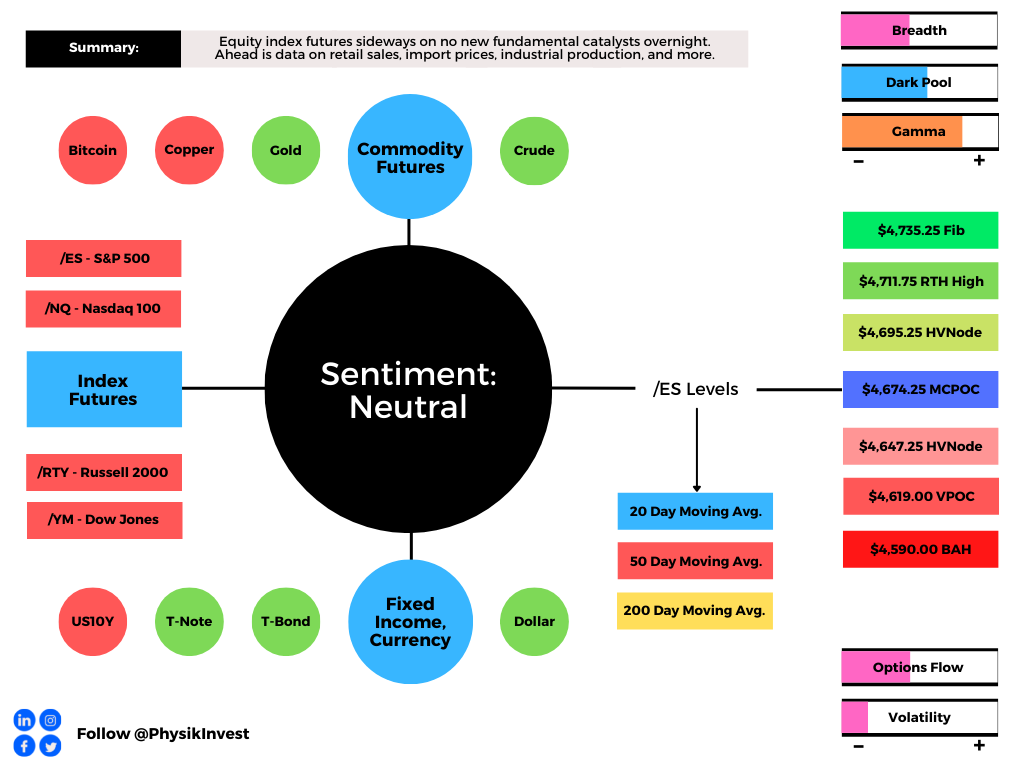

Expectations: As of 6:00 AM ET, Tuesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the lower part of a negatively skewed overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades sideways or higher; activity above the $4,674.25 micro composite point of control (MCPOC) puts in play the $4,695.25 high volume area (HVNode). Initiative trade beyond the HVNode could reach as high as the $4,711.75 all-time high and $4,735.25 Fibonacci, or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,674.25 MCPOC puts in play the $4,647.25 HVNode. Initiative trade beyond the HVNode could reach as low as the $4,619.00 VPOC and $4,590.00 balance area boundary (BAH), or lower.

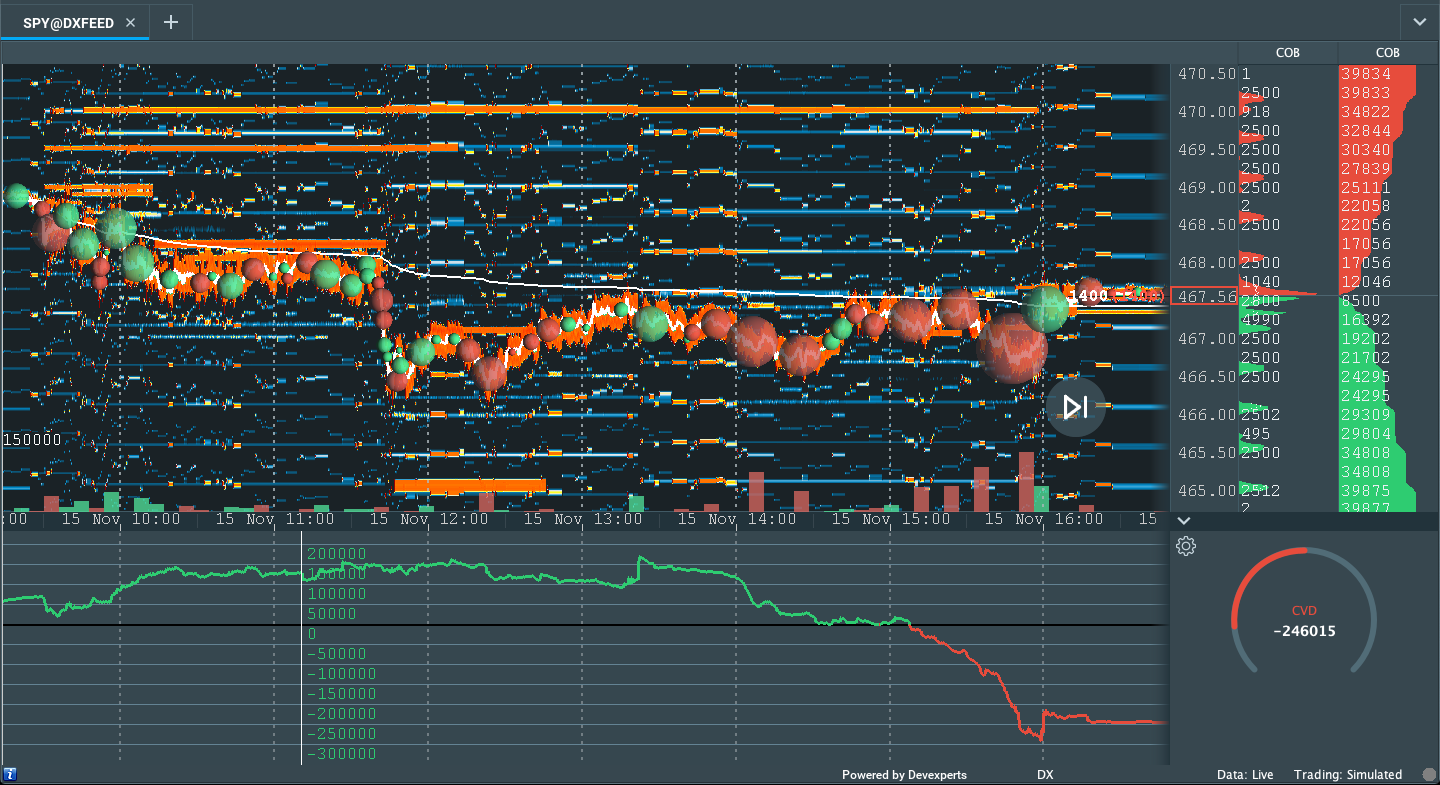

As an aside, participants reclaimed the volume-weighted average price (VWAP) anchored from the all-time high and recent Federal Open Market Committee (FOMC) meeting.

This is a metric highly regarded by chief investment officers, among other participants, for quality of trade. Additionally, liquidity algorithms are benchmarked and programmed to buy and sell around VWAPs.

Further, given that this development suggests the average buyer, since the all-time high, is in a winning position, who does this dynamic embolden? The buyer or seller?

Click here to load today’s updated key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

A Quick Guide To Options

Options offer an efficient way to gain directional exposure.

If an option buyer was short (long) stock, he or she could buy a call (put) to hedge upside (downside) exposure. Additionally, one can spread, or buy (+) and sell (-) options together, strategically.

Commonly discussed spreads include credit, debit, ratio, back, and calendar.

- Credit: Sell -1 option closer to the money. Buy +1 option farther out of the money.

- Debit: Buy +1 option closer to the money. Sell -1 option farther out of the money.

- Ratio: Buy +1 option closer to the money. Sell -2 options farther out of the money.

- Back: Sell -1 option closer to the money. Buy +2 options farther out of the money.

- Calendar: Sell -1 option. Buy +1 option farther out in time, at the same strike.

Typically, if bullish (bearish), sell at-the-money put (call) credit spread and/or buy a call (put) debit/ratio spread structured around target price. Alternatively, if the expected directional move is great (small), opt for a back spread (calendar spread). Also, if credit spread, capture 50-75% of the premium collected. If debit spread, capture 2-300% of the premium paid.

Be cognizant of risk exposure to direction (delta), time (theta), and volatility (vega).

- Negative (positive) delta = synthetic short (long).

- Negative (positive) theta = time decay hurts (helps).

- Negative (positive) vega = volatility hurts (helps).

What People Are Saying

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

Significance Of Prior ATHs, ATLs: Prices often encounter resistance (support) at prior highs (lows) due to the supply (demand) of old business. These areas take time to resolve. Breaking and establishing value (i.e., trading more than 30-minutes beyond this level) portends continuation.

Value-Area Placement: Perception of value unchanged if value overlapping (i.e., inside day). Perception of value has changed if value not overlapping (i.e., outside day). Delay trade in the former case.

About

After years of self-education, strategy development, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Additionally, Capelj is a Benzinga finance and technology reporter interviewing the likes of Shark Tank’s Kevin O’Leary, JC2 Ventures’ John Chambers, and ARK Invest’s Catherine Wood, as well as a SpotGamma contributor, developing insights around impactful options market dynamics.

Disclaimer

At this time, Physik Invest does not manage outside capital and is not licensed. In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.