Physik Invest’s Daily Brief is read by thousands of subscribers. You, too, can join this community to learn about the fundamental and technical drivers of markets.

Administrative

A quick letter today, apologies.

Given the large, post-CPI movement, the above dashboard may be out of date!

Separately, your letter writer will be heading to Davos, Switzerland during next week’s World Economic Forum. Let me know if you’ll be in town. Take care!

Fundamental

Today, market participants received data that appears in line with estimates.

Expected was a 6.5% rise year-over-year (YoY) and a 0.1% fall month-over-month (MoM). These numbers were +7.1% and +0.1% the release prior.

Mattering most is core inflation, which the Fed has more control over. The expectation was that core CPI rose 5.7% YoY and 0.3% MoM. In the release prior, these numbers were 6.0% and 0.2%, respectively.

Overall, the view that inflation is trending in the right direction is supported.

We often unpack the implications, but we will save that for a coming analysis.

Positioning

We saw meaningful outperformance in realized volatility (RVOL). This was, in part, a result of increased demand for short-dated exposures to movements (i.e., gamma), as well as a supply of farther-dated volatility (i.e., +gamma worked, +vega did not).

The trends, as your letter writer explained in recent write-ups, and in a Benzinga article, may eventually exhaust; measures like the VVIX, which is the volatility of the VIX or the volatility of the S&P 500’s volatility, are printing at levels seen in 2017.

According to Kai Volatility’s Cem Karsan, markets are in a transition period and what’s worked in 2022 may not work as well in 2023; trades are becoming crowded and S&P 500 volatility skews have hit a lower bound of sorts. That was echoed by The Ambrus Group’s Kris Sidial who said that “we can get cheap exposure to convexity while a lot of people are worried.”

Since the start of the year, the skew shifted meaningfully higher while the S&P 500 and VIX have moved higher in sync, as well. Some, like SpotGamma, have their own explanation (e.g., the fear of missing out on a move higher results in call buying that bids volatility), expressing that this may be a trend that persists through events like Thursday’s consumer price update.

This letter’s takeaway is as follows. Markets can experience more of the same. As history has shown, the right trade may turn out to be short volatility across longer time horizons, and long/own volatility across shorter time horizons, for longer (i.e., current trends promoting realized volatility outperformance may persist longer).

However, should current trends persist, the market is likely to become far less well-hedged, as Karsan said in the video. If a catalyst arises, there may be a repricing in volatility which traders would not want to be on the wrong side of. Notwithstanding, as Sidial says, “[if] you’re trading volatility, let there be an underlying catalyst for doing so.” Don’t just buy it because it is cheap, or sell it because it is expensive.

We’ll go through the charts and implications in far more detail over the coming sessions. Your letter writer is stretched for time this morning. Take care!

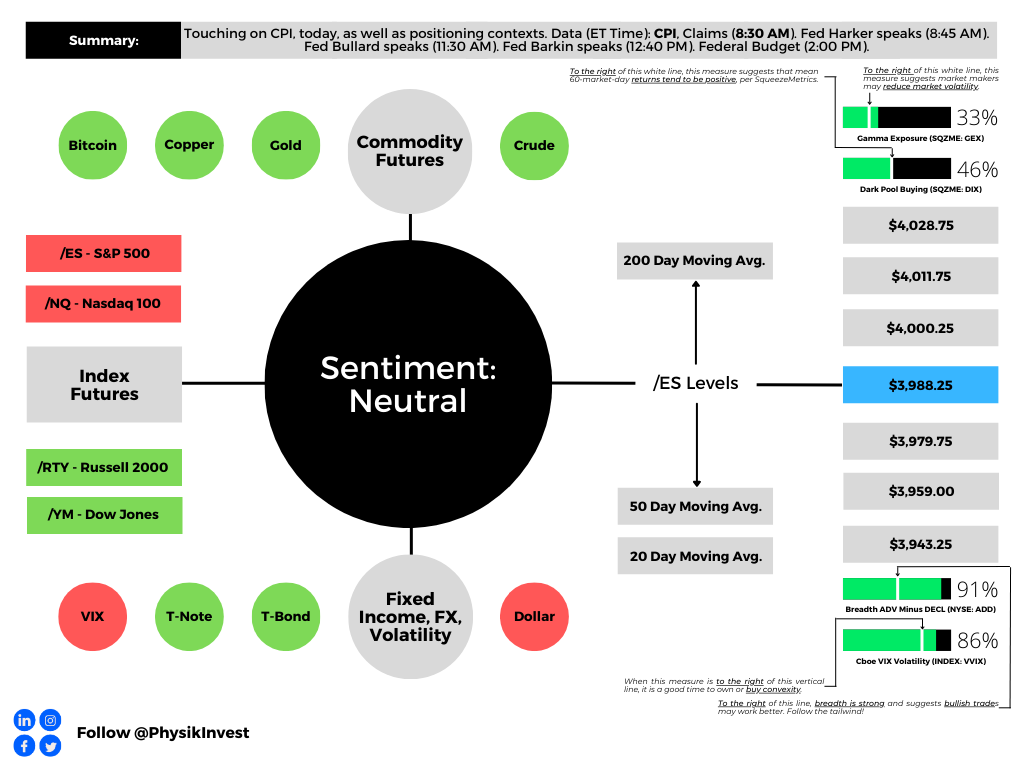

Technical

As of 7:30 AM ET, Thursday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the upper part of a positively skewed overnight inventory, outside of prior-range and -value, suggesting a potential for immediate directional opportunity.

Our S&P 500 pivot for today is $3,988.25 HVNode.

Key levels to the upside include $4,000.25, $4,011.75, and $4,028.75.

Key levels to the downside include $3,979.75, $3,959.00, and $3,943.25.

Click here to load today’s key levels into the web-based TradingView platform. All levels are derived using the 65-minute timeframe. New links are produced, daily.

As a disclaimer, the S&P 500 could trade beyond the levels quoted in the letter. Therefore, you should load the above link on your browser for more relevant levels.

Definitions

Volume Areas: Markets will build on areas of high-volume (HVNodes). Should the market trend for long periods of time, it will be identified by low-volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants auction and find acceptance in an area of a prior LVNode, then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: Denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: Denote areas where two-sided trade was most prevalent over numerous sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

About

In short, an economics graduate working in finance and journalism.

Capelj spends most of his time as the founder of Physik Invest through which he invests and publishes daily analyses to subscribers, some of whom represent well-known institutions.

Separately, Capelj is an equity options analyst at SpotGamma and an accredited journalist interviewing global leaders in business, government, and finance.

Past works include conversations with investor Kevin O’Leary, ARK Invest’s Catherine Wood, FTX’s Sam Bankman-Fried, Lithuania’s Minister of Economy and Innovation Aušrinė Armonaitė, former Cisco chairman and CEO John Chambers, and persons at the Clinton Global Initiative.

Contact

Direct queries to renato@physikinvest.com or Renato Capelj#8625 on Discord.

Calendar

You may view this letter’s content calendar at this link.

Disclaimer

Do not construe this newsletter as advice. All content is for informational purposes.