Physik Invest’s Daily Brief is read by thousands of subscribers. You, too, can join this community to learn about the fundamental and technical drivers of markets.

Fundamental

Please note the following conversation gives us very little edge. Rather, this text simply keeps our view of markets well-rounded. Read on for more.

Our past letters explored the contexts for long-lasting and/or double-dip inflation. As explained by the Credit Suisse Group AG’s (NYSE: CS) Zoltan Pozsar, there were a series of “non-linear shocks” (e.g., pandemic and the response to it, supply chain issues and shortages in labor, as well as the Ukraine conflict), and those shocks prompted a shift away from “generating demand structurally to soak up an excess supply of cheap stuff, to curbing demand structurally to adjust to shortages.”

Consequently, the economy is on an L-shaped trajectory (i.e., drop in activity via recession, and flatline for a period of time as rates remain higher for longer to prevent another rise in inflation).

In Pozsar’s recent updates, he added “the next set of non-linear shocks that will keep inflation above target, forcing central banks to hike interest rates above 5% and keep them high as they ‘clean up’ the inflation mess caused by … geopolitics, resource nationalism, and BRICS,” have yet to be priced by the market. At stake is the future of the dollar and US Treasury liquidity.

“I don’t think five-year forward five-year rates are pricing the future correctly,” he said, using his knowledge that pricing is the result of “central banks’ inflation targets” and liquidity.

“If investors read only the speeches of central bankers but not statesmen, they will be even more behind the curve” as the world shifts “from unipolar to multipolar, … built not by G7 heads of state but by the ‘G7 of the East’ (the BRICS heads of state),” representative of about ~40% of the global population and ~25% of the world’s GDP.

What’s Pozsar’s support for this thesis?

It is the start of alliances as powerful as those struck in 1945 between the US and the Middle East which resulted in the petrodollar (i.e., the US’s import of oil in exchange for dollars that Saudi Arabia spent on US Treasuries, arms, and deposits in US banks).

“President Xi [Jinping’s] visit with Saudi and GCC leaders marks the birth of the petroyuan and a leap in China’s growing encumbrance of OPEC+’s oil and gas reserves,” which is inflationary for the West (i.e., the US and beyond).

Xi Jinping’s speech during his visit was along the lines of the following, Pozsar wrote:

“In the next three to five years, China is ready to work with GCC countries in the following priority areas: first, setting up a new paradigm of all-dimensional energy cooperation, where China will continue to import large quantities of crude oil on a long-term basis from GCC countries, and purchase more LNG. We will strengthen our cooperation in the upstream sector, engineering services, as well as [downstream] storage, transportation, and refinery. The Shanghai Petroleum and Natural Gas Exchange platform will be fully utilized for RMB settlement in oil and gas trade, […] and we could start currency swap cooperation and advance the m-CBDC Bridge project”.

It’s a response to reduce reliances and hedge against sanctions risks. In “the next three to five years,” China, Saudi Arabia, and the GCC are pursuing “all-dimensional energy cooperation, … and oil [in exchange] for development.” No funding would happen in US dollars. Instead, China will buy more oil at big discounts, and it will do so “in renminbi over the next three to five years, … which GCC countries will be able to decumulate” through investments and development, as well as convertibility to gold via exchanges in Shanghai and Hong Kong, and mechanisms that involve the use of CBDCs “interlinked to facilitate interstate payments ‘off the Western system.’”

A product of this regime includes commodity encumbrance and rehypothecation, or the re-export of resources for profits (e.g., “China became a big exporter of Russian LNG to Europ, and India a big exporter of Russian oil and refined products such as diesel to Europe”).

Per the Financial Times’ Rana Foroohar, “the recycling of petrodollars by oil-rich nations” fueled “several emerging market debt crises” and prompted “the creation of a more speculative, debt-fueled economy in the US.”

“That trend may now start to go in reverse,” Foroohar added, a nod to Pozsar’s comments on the impact of the broader efforts to de-dollarize (e.g., the creation of a “commodity-weighted neutral reserve asset that encourages members to pledge their commodities to the BRICS ‘cause’”), all the while more drilling does less and less to boost the supply oil and gas.

Consequently, by encumbering commodities in strict supply, nations can boost their weights in currency baskets. This may “keep inflation from slowing and interest rates from falling for the rest of this decade.” Monetary policymakers are not well-equipped to fight this trend.

More on these themes in the coming newsletters. Have a great day!

Technical

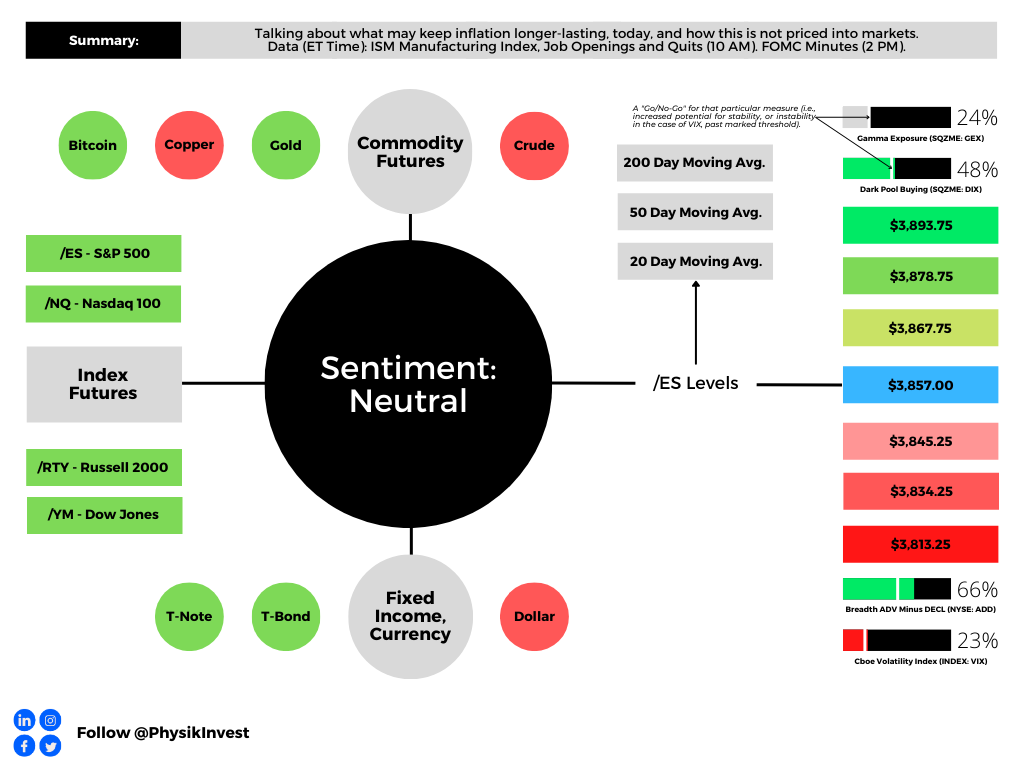

As of 8:45 AM ET, Wednesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, is likely to open in the upper part of a positively skewed overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

Our S&P 500 pivot for today is $3,857.00.

Key levels to the upside include $3,867.75, $3,878.75, and $3,893.25.

Key levels to the downside include $3,845.25, $3,834.25, and $3,813.25.

Click here to load today’s key levels into the web-based TradingView platform. All levels are derived using the 65-minute timeframe. New links are produced, daily. The levels may have changed since initially quoted due to rapid movement prior to the market opening.

Definitions

Volume Areas: Markets will build on areas of high-volume (HVNodes). Should the market trend for long periods of time, it will be identified by low-volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants auction and find acceptance in an area of a prior LVNode, then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

MCPOCs: Denote areas where two-sided trade was most prevalent over numerous sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

About

In short, an economics graduate working in finance and journalism.

Capelj spends most of his time as the founder of Physik Invest through which he invests and publishes daily analyses to subscribers, some of whom represent well-known institutions.

Separately, Capelj is an equity options analyst at SpotGamma and an accredited journalist interviewing global leaders in business, government, and finance.

Past works include conversations with investor Kevin O’Leary, ARK Invest’s Catherine Wood, FTX’s Sam Bankman-Fried, Lithuania’s Minister of Economy and Innovation Aušrinė Armonaitė, former Cisco chairman and CEO John Chambers, and persons at the Clinton Global Initiative.

Contact

Direct queries to renato@physikinvest.com or Renato Capelj#8625 on Discord.

Calendar

You may view this letter’s content calendar at this link.

Disclaimer

Do not construe this newsletter as advice. All content is for informational purposes.

One reply on “Daily Brief For January 4, 2023”

[…] coverage adds to comments made, yesterday. See the Daily Brief for January 4, here. If you’re short on time, here’s an […]