Market Commentary

Equity index futures are set to open sideways Sunday after a divergent advance on light volume and poor structure.

- Fundamental context – the good and bad.

- Ahead a heavy week in terms of releases.

- A narrow rally on unsupportive dynamics.

- A simple way to hedge off your downside.

What Happened: U.S. stock index futures auctioned sideways to higher last week as the baseline Dow Jones Industrial Average is forecast to have peaked, according to Moody’s.

Ahead is data on the Empire State manufacturing index (8/16), retail sales (8/17), industrial production (8/17), capacity utilization (8/17), business inventories (8/17), NAHB home builders’ index (8/17), building permits (8/18), housing starts (8/18), Federal Open Market Committee (FOMC) minutes (8/18), jobless claims (8/19), Philadelphia Fed manufacturing index (8/19), and the index of leading economic indicators (8/19).

What To Expect: During the prior week’s trade, on weak intraday breadth and market liquidity metrics, the best case outcome occurred, evidenced by trade above the $4,422.75 balance area high (BAH). This trade is significant because it validated a balance area breakout.

More On Balance-Break Scenarios: A change in the market (i.e., the transition from two-time frame trade, or balance, to one-time frame trade, or trend) is occurring. Monitor for acceptance (i.e., more than 1-hour of trade) outside of the balance area. Rejection (i.e., return inside of balance) portends a move to the opposite end of the balance.

Further, the aforementioned trade is happening in the context of peak growth, moderating inflation, renewed fiscal stimulus efforts, and increased odds of Fed tapering early next year.

The implications of this fundamental context on price are contradictory; to elaborate, as Michael Gayed of The Lead-Lag Report recently said, narrow high yield spreads offer little potential for capital growth, and “conditions that favor higher volatility – the Fed backing off stimulus measures, the upcoming battle over the debt ceiling, high current inflation and/or longer-term deflation – could be not far off into the future.”

As an aside, this leads us into the narrative on the so-called shift from monetary to fiscal; in a conversation for a Benzinga article, Kai Volatility’s Cem Karsan said the following: when liquidity is removed, as policymakers look to fiscal policy to address inequality, for instance, corporations may have to worry about making money, again.

“We’ve seen this throughout history,” Karsan said in reference to this thesis playing out over the next decade, at least. “These cycles are a lot shorter than the monetary supply-side cycles but they tend to be very bad for multiples and great for economic growth.”

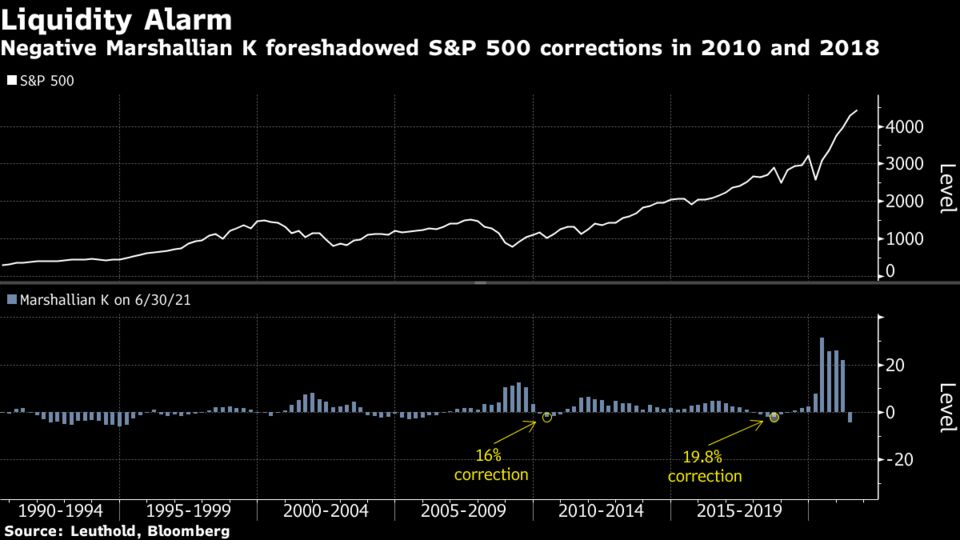

Adding, in Friday’s note, the theme of liquidity was discussed. Simply put, the gap between the rates of growth in the supply of money and the gross domestic product turned negative for the first time since 2018.

“Put another way, the recovering economy is now drinking from a punch bowl that the stock market once had all to itself,” said Doug Ramsey, Leuthold Group’s chief investment officer.

Moreover, for next week, given expectations of middling volatility and responsive trade, on factors like the upcoming August 20 monthly options expiration, participants may make use of the following frameworks.

Options Expiration (OPEX): Option expiries mark an end to pinning (i.e, the theory that market makers and institutions short options move stocks to the point where the greatest dollar value of contracts will expire worthless) and the reduction dealer gamma exposure.

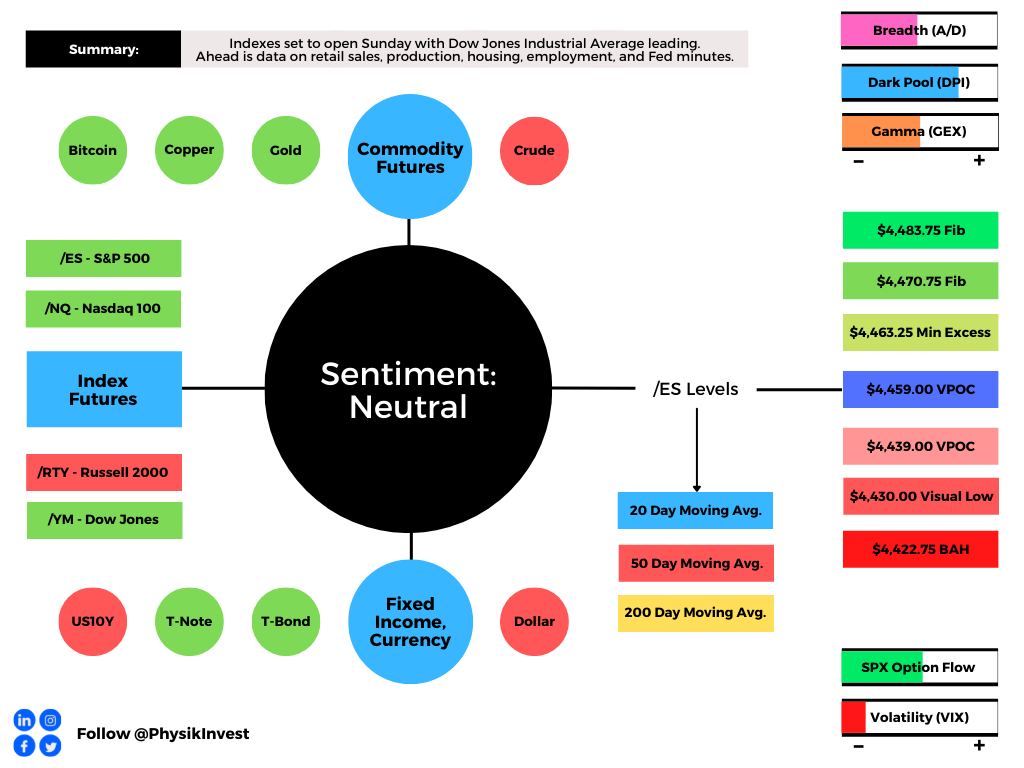

In the best case, the S&P 500 trades sideways or higher; activity above the $4,459.00 untested point of control (VPOC) puts in play the $4,463.25 minimal excess high. Initiative trade beyond the minimal excess high could reach as high as the $4,470.75 and $4,483.75 Fibonacci-derived price targets.

In the worst case, the S&P 500 trades lower; activity below the $4,459.00 VPOC puts in play the $4,439.00 VPOC. Initiative trade beyond the $4,439.00 VPOC could reach as low as $4,430.00 – a visual low likely generated by short-term (i.e., technically driven) participants who may be unable to defend retests – and the previously discussed $4,422.75 BAH.

Volume Areas: A structurally sound market will build on past areas of high volume. Should the market trend for long periods of time, it will lack sound structure (identified as a low volume area which denotes directional conviction and ought to offer support on any test). If participants were to auction and find acceptance into areas of prior low volume, then future discovery ought to be volatile and quick as participants look to areas of high volume for favorable entry or exit. Excess: A proper end to price discovery; the market travels too far while advertising prices. Responsive, other-timeframe (OTF) participants aggressively enter the market, leaving tails or gaps which denote unfair prices. POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent. Participants will respond to future tests of value as they offer favorable entry and exit.

Weekly Trade Idea

Please Note: In no way is the below a trade recommendation. It’s a response to a solicitation for simple ways to hedge against a move lower, into the end of the month.

Options offer an efficient way to gain directional exposure.

If an option buyer was short (long) stock, he or she could buy a call (put) to hedge upside (downside) exposure. Additionally, one can spread, or buy (+) and sell (-) options together, strategically.

Commonly discussed spreads include credit, debit, ratio, back, and calendar.

- Credit: Sell -1 option closer to the money. Buy +1 option farther out of the money.

- Debit: Buy +1 option closer to the money. Sell -1 option farther out of the money.

- Ratio: Buy +1 option closer to the money. Sell -2 options farther out of the money.

- Back: Sell -1 option closer to the money. Buy +2 options farther out of the money.

- Calendar: Sell -1 option. Buy +1 option farther out in time, at the same strike.

Typically, if bullish (bearish), sell at-the-money put (call) credit spread and/or buy a call (put) debit/ratio spread structured around target price. Alternatively, if the expected directional move is great (small), opt for a back spread (calendar spread). Also, if credit spread, capture 50-75% of the premium collected. If debit spread, capture 2-300% of the premium paid.

Be cognizant of risk exposure to direction (delta), time (theta), and volatility (vega).

- Negative (positive) delta = synthetic short (long).

- Negative (positive) theta = time decay hurts (helps).

- Negative (positive) vega = volatility hurts (helps).

Trade Idea: BUY +1 BUTTERFLY SPX 100 (Weeklys) 31 AUG 21 4450/4400/4350 PUT @4.90 LMT.

Thesis: I’m neutral to bearish on the S&P 500 and I think the index may trade sideways to lower into the next month. I will structure a spread below the current index price, expiring in 15 days. I will buy the 4450 put option once (+1), sell the 4400 put option twice (-2), and buy the 4350 put option once (+1) for a $4.90 debit or so. Should the index not move to my target, I may lose the $490 debit. Should it move to $4,400.00, I could make $4,510.00 (i.e., the $5,000.00 payout less debit at entry) at expiry. Should the index move below $4,354.90, I may lose the entire $490 debit. My goal, with this spread, is to close for credit (e.g., $9.80-14.70) if the index moves lower. Note that this trade carries a positive theta at entry.

If necessary, I will hedge the position by either (A) buying S&P 500 futures, (B) narrowing strikes, (C) selling call credit to reduce cost, or (D) roll strikes up in price and out in time.

News And Analysis

Rates recovering; realtors see price moderating.

This turning point for markets merits a hard look.

Market disruptions as Fed balance sheet swells.

Job data eases fears of a slowdown in recovery.

U.S. high yield default rate lowest start in 14 yrs.

Delta variant will not impact Fed’s tapering plan.

What People Are Saying

About

After years of self-education, strategy development, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Additionally, Capelj is a finance and technology reporter. Some of his biggest works include interviews with leaders such as John Chambers, founder and CEO, JC2 Ventures, Kevin O’Leary, businessman and Shark Tank host, Catherine Wood, CEO and CIO, ARK Invest, among others.

Disclaimer

At this time, Physik Invest does not manage outside capital and is not licensed. In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.