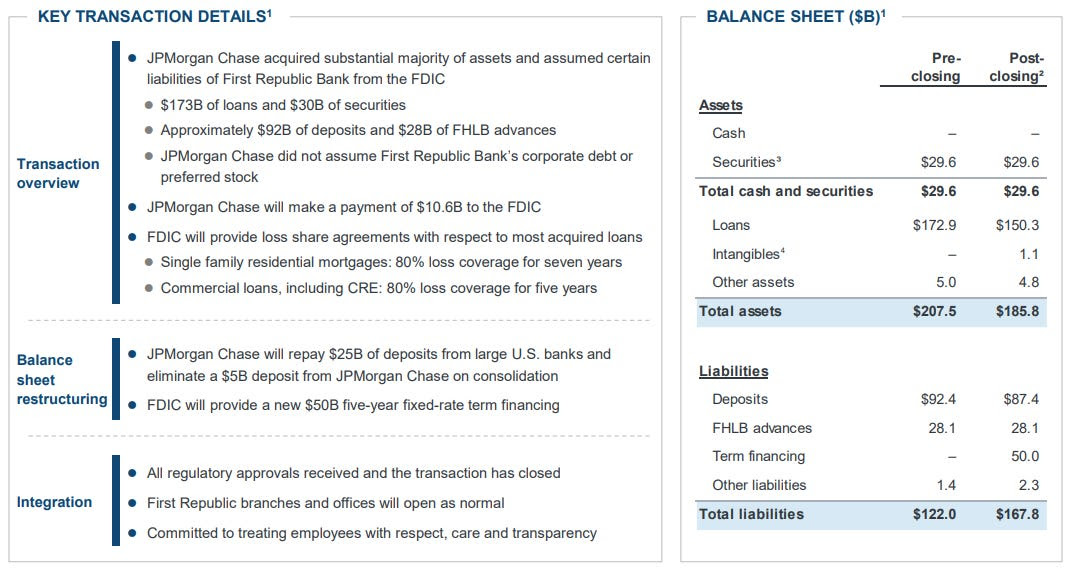

First Republic Bank (NYSE: FRC) is in the news for its failure. FRC was known for handing out mortgages at rock-bottom rates. When interest rates rose, the bank’s book of mortgages was hurt and left it with not enough to suffice withdrawals.

“FRC believed its business model of extraordinary customer service and product pricing would result in superior customer loyalty through all cycles,” wrote Timothy Coffey of Janney Montgomery Scott. “Instead, too many FRC customers showed their true loyalties were to their own fears.”

This “marks the second-biggest bank failure in U.S. history, behind the 2008 collapse of Washington Mutual Inc.,” reports WSJ; after the instability in March, the bank finally succumbed to the Federal Reserve’s (Fed) rate increases and depositor worry.

JPMorgan Chase & Co (NYSE: JPM) acquired the bulk of FRC’s operations.

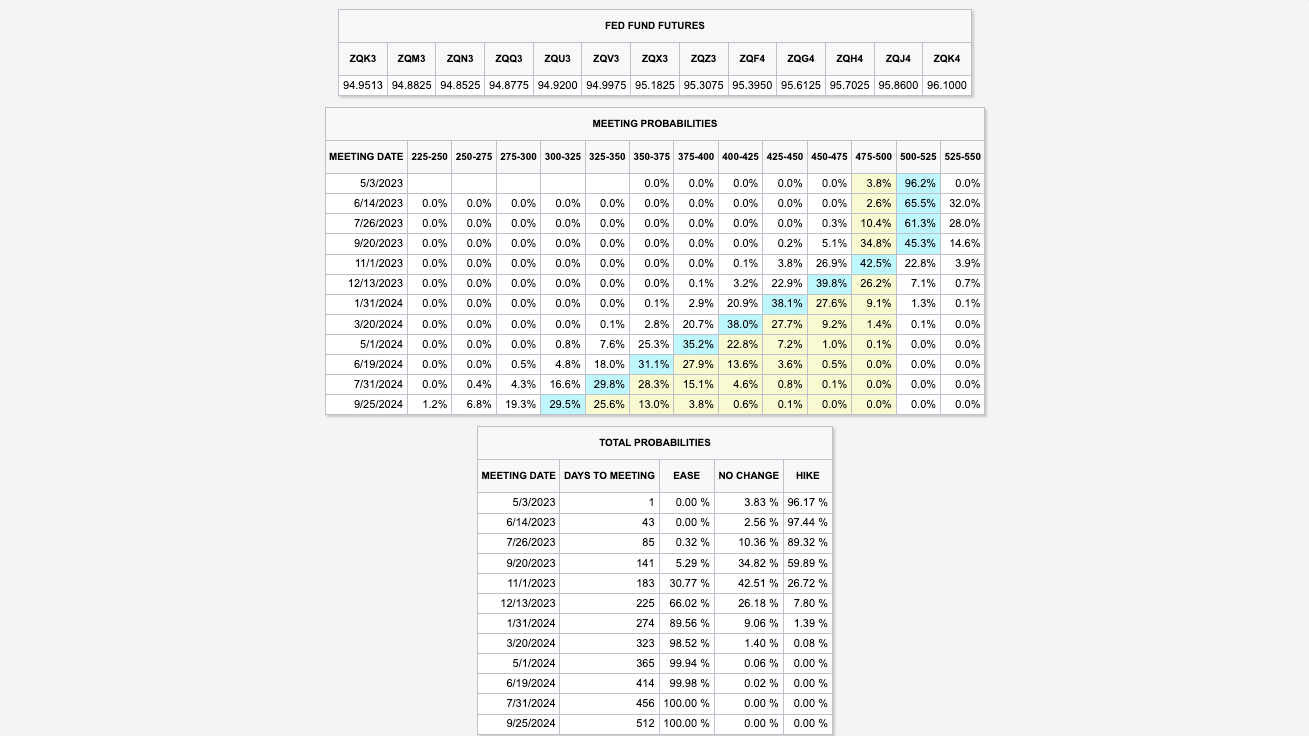

Further, research shows money is getting tighter, a headwind for the economy, while inflation is sticky and the Fed’s bond holdings are preventing tightening from being effective; WSJ reports the Fed’s balance sheet loaded with bonds may be insulating stocks from interest rate policies.

“Quantitative easing locked the Fed into a position that is difficult to unwind,” said Stephen Miran of Amberwave Partners. Quantitative easing, or QE, made stocks less sensitive to interest rates. “It’s made tightening both slower and less effective than it should have been.”

Not “adjusting balance-sheet policy,” but raising rates to 5.00-5.25% as expected, ‘is akin to “hitting the same nail with a hammer over and over again.’” Therefore, stocks, which are higher alongside surprising economic and earnings data, though risky, can do “ok” for longer, comments Andy Constan of Damped Spring Advisors.

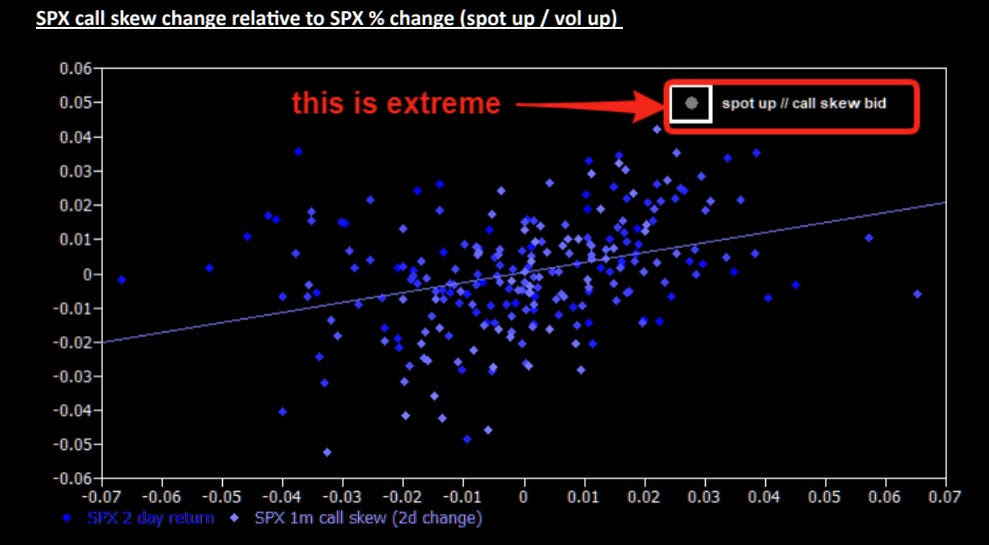

The sale of volatility bolsters the stability and emboldens upside bettors, adds JPM’s Marko Kolanovic, who finds “selling of options forces intraday reversion, leaving the market price virtually unchanged many days.”

“This, in turn, drives buying of stocks by funds that mechanically increase exposure when volatility declines (e.g., volatility targeting and risk parity funds),” he elaborates. “This market dynamic artificially suppresses perceptions of fundamental macro risks. The low hurdle rate and robust fundamentals bode well for 1Q earnings results, but we advise using any market strength on reporting to reduce exposure.”

At this juncture, yes, stocks can move sideways or higher for a bit longer as a function of “momentum, not value,” Simplify Asset Management’s Michael Green concludes. Traders can position for this and various levels of potential upset later with structures included in a report we published last week.

About

Welcome to the Daily Brief by Physik Invest, a soon-to-launch research, consulting, trading, and asset management solutions provider. Learn about our origin story here, and consider subscribing for daily updates on the critical contexts that could lend to future market movement.

Separately, please don’t use this free letter as advice; all content is for informational purposes, and derivatives carry a substantial risk of loss. At this time, Capelj and Physik Invest, non-professional advisors, will never solicit others for capital or collect fees and disbursements. Separately, you may view this letter’s content calendar at this link.