Inflation and employment rates remain high. Additionally, consumers show resilience, and earnings are strong. As a consequence, markets are back to pricing higher rates for longer. This is a pressure on bonds and stocks which appear “overvalued relative to coming bad news on both economic growth and corporate earnings.”

Morgan Stanley (NYSE: MS) says stocks are at risk of a pullback, accordingly.

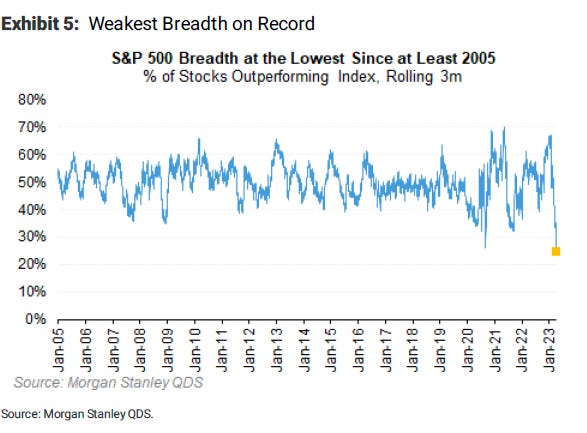

With the percentage of stocks outperforming the S&P 500 the lowest on record, MS added, a slump in technology is the big risk if yields continue to rise; the bear market is not yet over. “If there is one thing that can throw cold water on the large mega-cap rally, it’s higher yields due to a Fed that can’t stop hiking.”

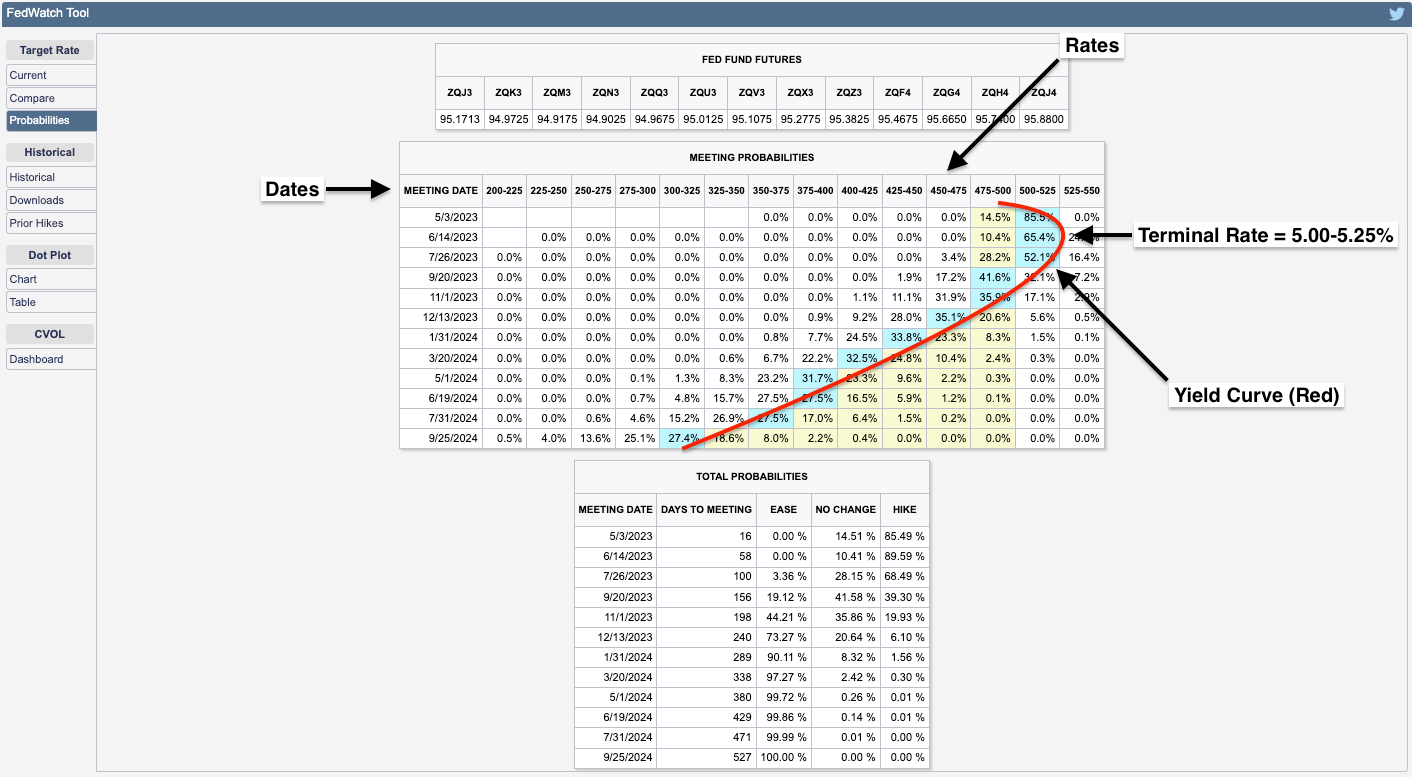

Moody’s Corporation (NYSE: MCO) expects a “0.25-percentage point increase to the fed funds rate when the FOMC reconvenes in early May.” Following this hike, there is likely to be a pause at a 5.00-5.25% terminal rate for a few months.

From a positioning perspective, Kai Volatility’s Cem Karsan stated that in the past 6-9 months, there has been a significant increase in the volume of options with zero days to expiration (0 DTE), which now accounts for 44% of the total volume. This increase in short-dated options volume has been accompanied by a similarly sized decrease in longer-dated options volume.

Further, the majority of trading activity in these short-dated options is split between hedging and directional trading, as well as yield harvesting via out-of-the-money (OTM) options sales. Though the short-dated activity may prompt cascading events in market downturns, the main issue is the reduced use of longer-dated options; a supply and demand imbalance likely resolves itself with an implied volatility repricing of great size where longer-dated options outperform those that are shorter-dated.

Traders can look to position for a potential IVOL repricing, particularly in the back half of the year when dealer positioning is less clear, buybacks are to fall off of a cliff, and the boost from short-covering has played its course.

Traders can continue to play near-term strength via call spread structures and use those profits to reduce the costs of owning longer-dated bets on markets or rates falling and IVOL increasing. If not interested in directional exposure, traders may allocate funds to T-bills and SPX box spreads which allow traders to create a loan structure similar to a T-bill. If savvy, one could find some structures yielding ~5.5%. Traders can also consider blending T-bills and boxes with directional exposure. This way, they can cut portfolio volatility but still have a bit of leverage potential. Please check out our past letters for trade structure specifics. Have a great day!

About

Welcome to the Daily Brief by Physik Invest, a soon-to-launch research, consulting, trading, and asset management solutions provider. Learn about our origin story here, and consider subscribing for daily updates on the critical contexts that could lend to future market movement.

Separately, please don’t use this free letter as advice; all content is for informational purposes, and derivatives carry a substantial risk of loss. At this time, Capelj and Physik Invest, non-professional advisors, will never solicit others for capital or collect fees and disbursements. Separately, you may view this letter’s content calendar at this link.