The narrative yesterday was bearish.

A big deal was made surrounding some data that shows investors increasing their bets on US equities falling; net short positions in the E-mini S&P 500 (FUTURE: /ES) are the highest since 2011, Bloomberg reports. JPMorgan Chase & Co (NYSE: JPM) and Goldman Sachs Group Inc (NYSE: GS) concur as their data shows clients betting on stocks falling or reducing stock exposure quickly.

This is happening in the context of some mixed, albeit still robust-leaning, data; payrolls upped bets that the Federal Reserve or Fed would move its target rate to 5.00-5.25%. GS’ Bobby Molavi adds, “the prevalent view seems to be that more things will break on the back of rapid rise in cost of capital.”

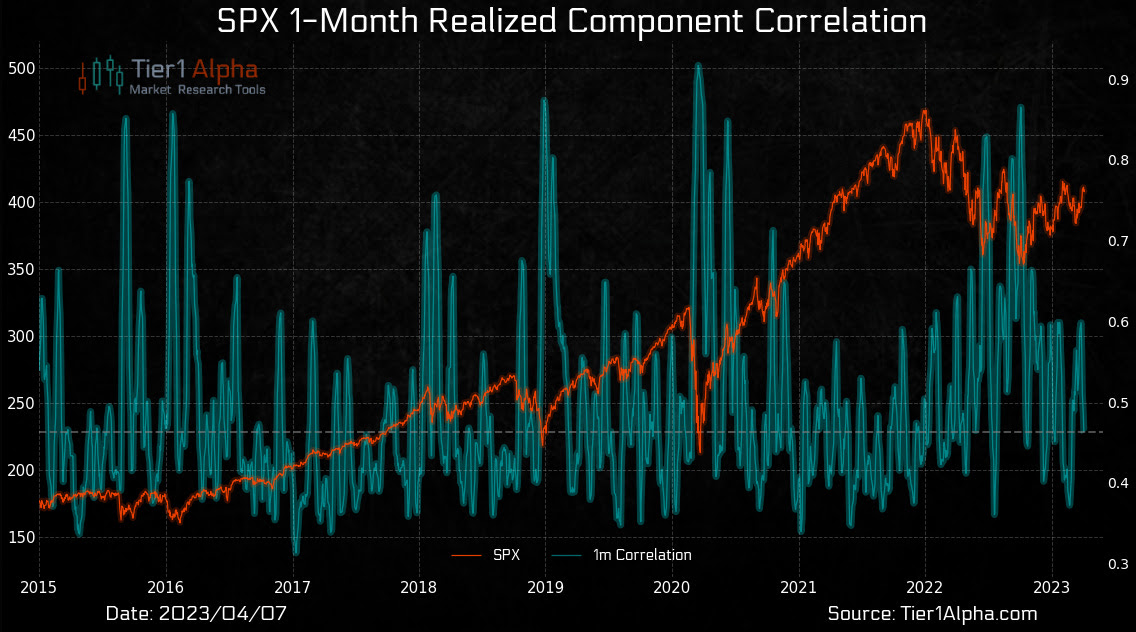

In light of the rate expectations, the Nasdaq 100 (INDEX: NDX) appears to be handing over the leadership baton to the S&P 500 (INDEX: SPX), though both indexes remain primarily intact and coiling; the fundamental-type pressures are balanced by follow-on support from those actors that base their decisions on such things as the amount a market moves (i.e., realized volatility or RVOL), says Tier1Alpha and SpotGamma.

The two providers of market insights see falling implied (IVOL) and RVOL as catalysts for buying stocks. This, coupled with the hedging of soon-to-expire large options open interest, particularly on the put side, in a lower liquidity environment, supports the indexes while underlying breadth and correlations are underwhelming.

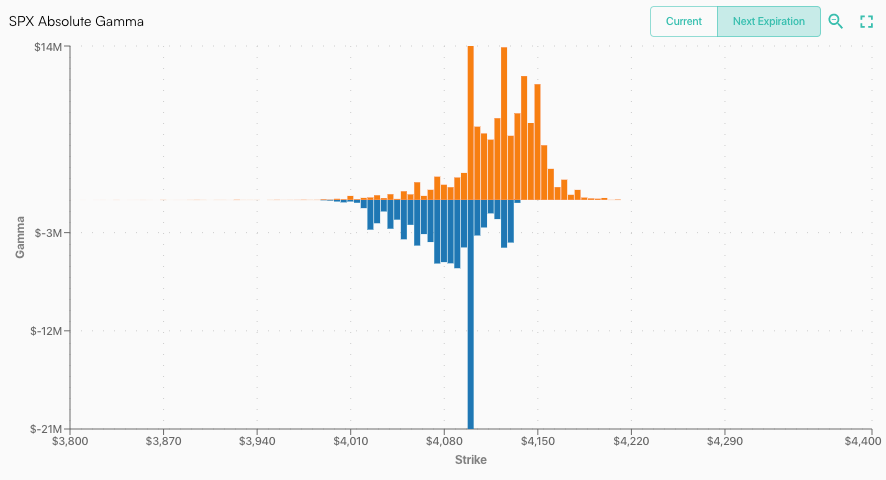

A large concentration of put open interest near current prices is pictured just below. The eventual removal of this put-heavy positioning will reduce some directional risks to options counterparts; as puts disappear or decline in value, their delta or exposure to direction does too. If a counterparty is short a put and has less positive delta to hedge, they may buy back some of their short-delta exposure in the underlying index, a catalyst for higher S&P 500 prices.

A large open interest concentration set to roll off this April is pictured just below.

This has happened before. Newfound Research explains it best in their paper titled “Liquidity Cascades: The Coordinated Risk of Uncoordinated Market Participants.”

In keeping the indexes and their underlying idiosyncratic baskets in line via arbitrage constraints, while there is a build-up of suppressive and supportive dealer hedging at the index level, “then the only reconciliation is a decline in correlation.”

In this context, Tier1Alpha explains, “lower correlations tend to lead to lower volatility … giv[ing] volatility control funds the go-ahead to augment their risk exposure, with an estimated $14 billion in equities purchases … to be spread out in blocks.”

Consequently, in line with our thesis that positioning and technical contexts support near-term strength, it still makes sense to take the profits of very wide, albeit low- or zero-cost, call ratio spread structures discussed in past letters to cut the cost of our bets on the equity market downside and lower rates with more time to expiry. Should the indexes trade higher, SpotGamma agrees with Kai Volatility’s Cem Karsan that volatility could be sticky.

Hence, call structures could keep their value better and enable us to lower the cost of our bets on the market downside. If the fundamental context supporting the rotation of call option profits into puts is no longer valid, then the losses on such trades are limited; the money is made in not losing it.

Not doing as outlined and blindly buying put options to protect long equity exposure is generally a poor-performing strategy, despite the performance claims of some funds specializing in that practice.

About

Welcome to the Daily Brief by Physik Invest, a soon-to-launch research, consulting, trading, and asset management solutions provider. Learn about our origin story here, and consider subscribing for daily updates on the critical contexts that could lend to future market movement.

Separately, please don’t use this free letter as advice; all content is for informational purposes, and derivatives carry a substantial risk of loss. At this time, Capelj and Physik Invest, non-professional advisors, will never solicit others for capital or collect fees and disbursements. Separately, you may view this letter’s content calendar at this link.