The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 300+ that read this report daily, below!

What Happened

U.S. markets were weighed by action abroad before recovering late in the overnight session.

This was ahead of a European Central Bank (ECB) decision that likely results in a tightening of monetary policies in that region of the world. The expectation is that the ECB will end its bond purchases this month. Then, hike rates in July and September.

At home, in the U.S., the Securities and Exchange Commission (SEC) is looking to change the business model of wholesalers. In consideration is a model in which different firms compete with each other to fill investors’ trades. Some suggest this would increase trading costs.

Elsewhere, one of the largest U.S. export plants of liquified natural gas (LNG) is to shut down due to a facility explosion, raising the risk of shortages in Europe, according to Reuters.

Ahead is data on jobless claims (8:30 AM ET), as well as real household net worth and domestic financial debt (12:00 PM ET).

What To Expect

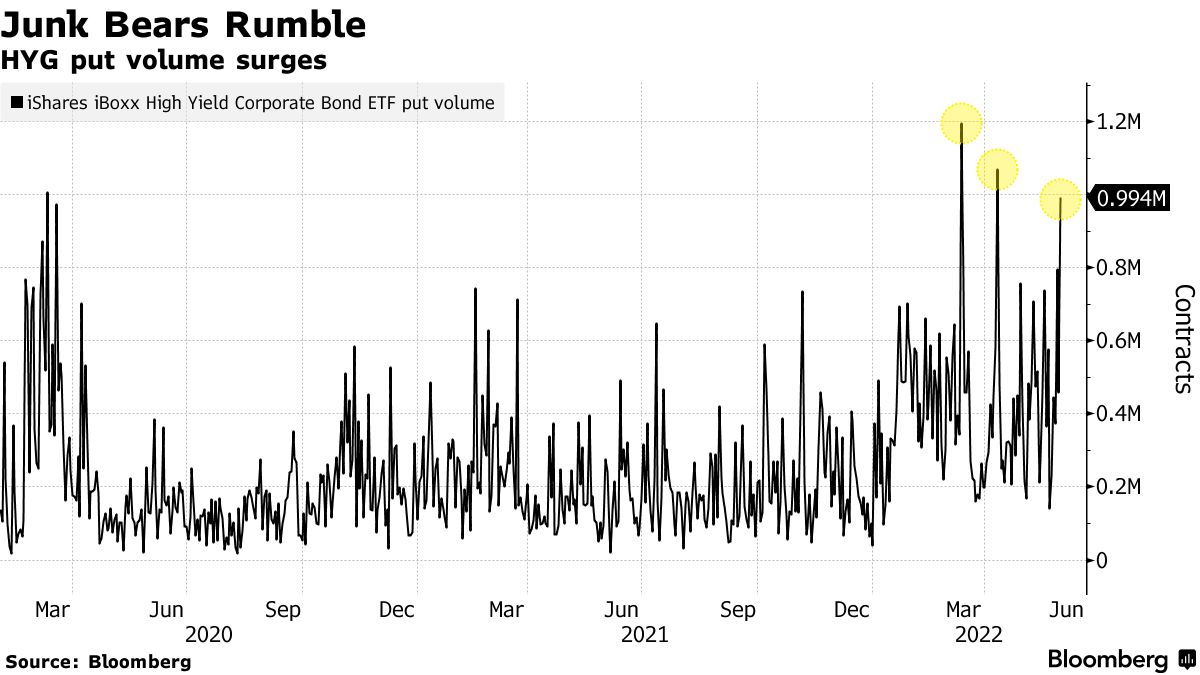

In the past week, a narrative on bearish bets in funds such as the iShares iBoxx $ High Yield Corporate Bond ETF (NYSE: HYG) surfaced.

The ETF saw some of the largest volumes since March of 2020, presumably as traders looked to hedge for low cost, the Federal Reserve’s (FED) hawkishness.

According to The Ambrus Group’s Kris Sidial, “a lot of banks continue to push credit vol[atility] as a cheap hedge. Every month, at least four banks push the theme on that trade because of ‘value.’”

This is “also, another reason why every month you see HYG put spreads hit the tape with big size, relatively speaking,” he adds.

Adding, Bridgewater Associates, which was founded by Ray Dalio in 1975, is betting on the sale of corporate bonds via credit default swaps (CDS), which are used to transfer and hedge credit exposure on fixed income products.

Bridgewater’s Co-Chief Investment Officer Greg Jensen explained their bet against corporate bonds is based on inflation remaining stubborn, resulting in the Fed to “tighten in a very strong way, which would then crack the economy and probably crack the weaker [companies].”

Here’s why that matters.

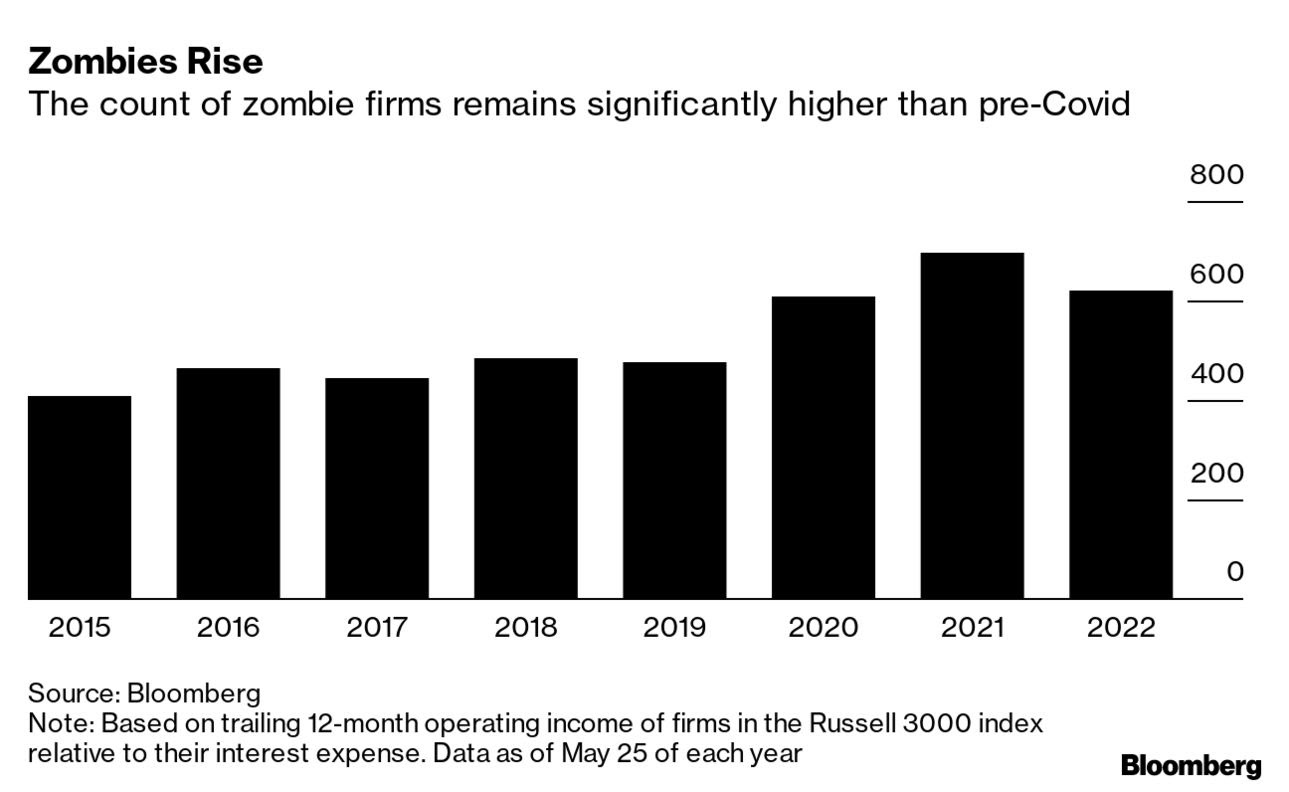

The firms facing challenges, “are creations of easy credit,” according to Bloomberg and, now, for some of them, their time is running short as they “aren’t earning enough to cover their interest expenses, let alone turn a profit.”

“When interest rates are at or close to zero, it’s very easy to get credit, and under those circumstances, the difference between a good company and a bad company is narrow,” said Komal Sri-Kumar of Sri-Kumar Global Strategies.

“It’s only when the tide runs out that you figure out who is swimming naked.”

Despite many of these companies having debt that could last them “months, even years,” Vincent Reinhart explains that “[a]s rates rise, it pushes more of those firms into distress, and amplifies the tightening by the Fed of financial conditions and credit availability.”

As stated yesterday, financial conditions are “the mechanism through which the Fed [impacts] the economy,” and “if the data doesn’t slow, financial conditions will need to tighten more,” potentially feeding into a freezing of credit and a harder hit on still-frothy areas of the market “with the greatest systemic risk.”

As we quoted Simplify Asset Management’s Mike Green explaining in early May, we’re more than halfway through a dot-com type collapse that’s happened “underneath the surface of the indices.”

That’s noteworthy since still-strong passive flows continue to support the largest stocks within the index.

That said, with bonds “not acting as a hedge and appear to be becoming less ‘money’ like due persistent declines in price and elevated rate vol,” per Joseph Wang, who was a trader at the Fed, “[i]nvestors in both bonds and stocks are reaching for cash by selling their assets, driving further asset price declines. For non-bank investors, ‘cash’ means bank deposits.”

How to think about trades?

As explained, yesterday, the marginal impact of further volatility compression is likely to do less to bolster equity market upside. Heading into the Federal Open Market Committee (FOMC) event, next week, according to SpotGamma, short-dated, pre-event volatility is likely to get sold (further promoting market consolidation) while that which is farter-dated is likely to be bought.

To capitalize on a resolution of the index-level pinning, participants, too, could sell short-dated volatility (which capitalizes on pinning and the rapid decay of soon-to-expire options) and use those proceeds to fund farther dated options.

Such a structure would assist in lower the cost of directional exposure.

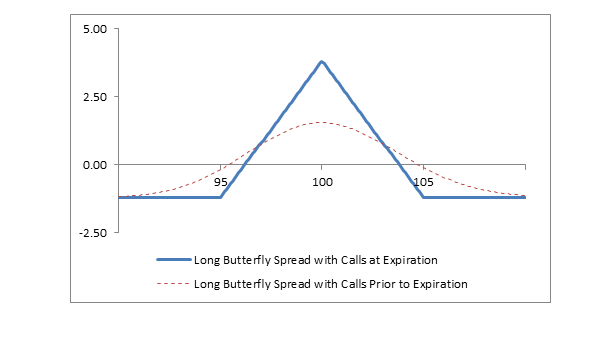

Alternatively, if bearish on volatility, one could buy a butterfly (short two times at the money and long above and below out of the money options).

In such a case, the trader becomes long implied skew convexity. This is a play on the comments above, coupled with the fact that the Cboe VVIX Index (INDEX: VVIX), the expected volatility of the 30-day forward price of the VIX, or the volatility of volatility (a naive but useful measure of skew), dropped off largely, too, in comparison to the VIX, itself.

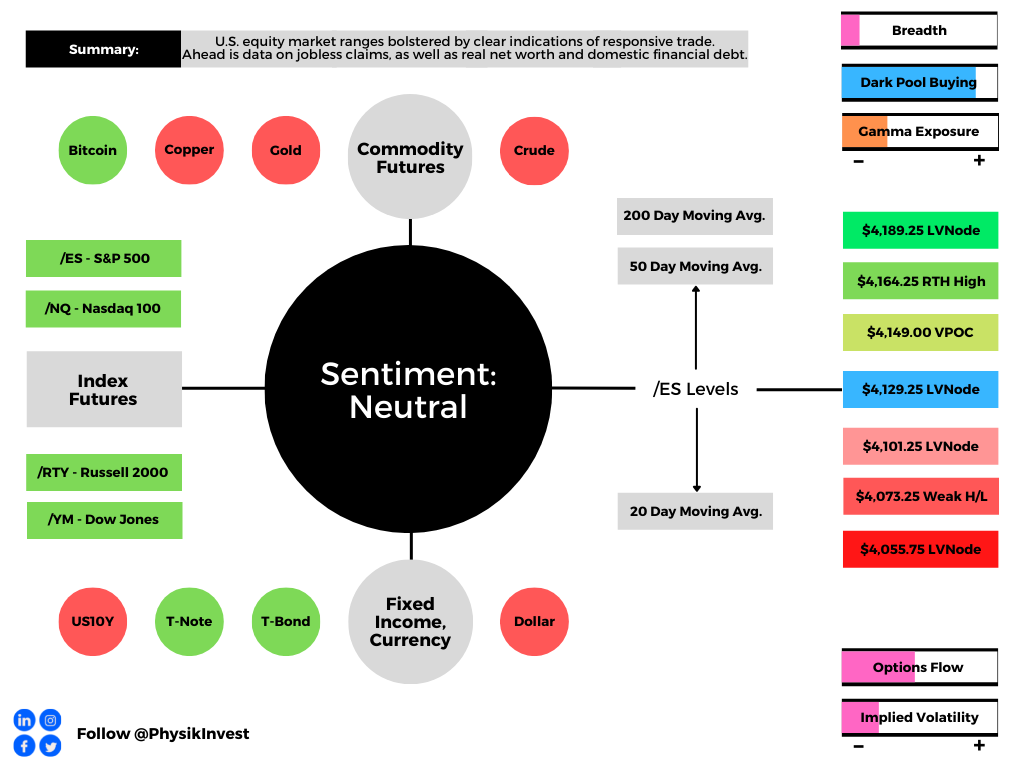

Technical: As of 6:40 AM ET, Thursday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the upper part of a balanced overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher; activity above the $4,129.25 low volume area (LVNode) puts in play the $4,149.00 untested point of control (VPOC). Initiative trade beyond the VPOC could reach as high as the $4,164.25 regular trade high (RTH High) and $4,189.25 LVNode, or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,129.25 LVNode puts in play the $4,101.25 LVNode. Initiative trade beyond the LVNodes could reach as low as the $4,073.25 weak high/low and $4,055.75 LVNode, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

Some of his works include conversations with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, FTX’s Sam Bankman-Fried, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, among many others.

Disclaimer

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.

One reply on “Daily Brief For June 9, 2022”

[…] It remains profitable to own options structures as implied (IVOL) underprices the volatility which is realized […]