What Happened: On November 17, 2020, shares of Tesla Inc (NASDAQ: TSLA) surged on news that S&P Dow Jones Indices would include the stock in the S&P 500, the most liquid index in the world.

Since markets are most influenced by credit and positioning, news of the inclusion was impactful. Funds tied to the S&P 500 would purchase Tesla shares from a dealer by the addition date. This means that dealers would look to purchase shares of the stock heading into the event, to later supply funds at the close of Friday, December 18, the last session before the inclusion.

In the simplest of terms, the event was a positive since it meant that (1) speculative derivatives activity and associated hedging, (2) short-term traders, as well as (3) dealers and index funds would now support the stock.

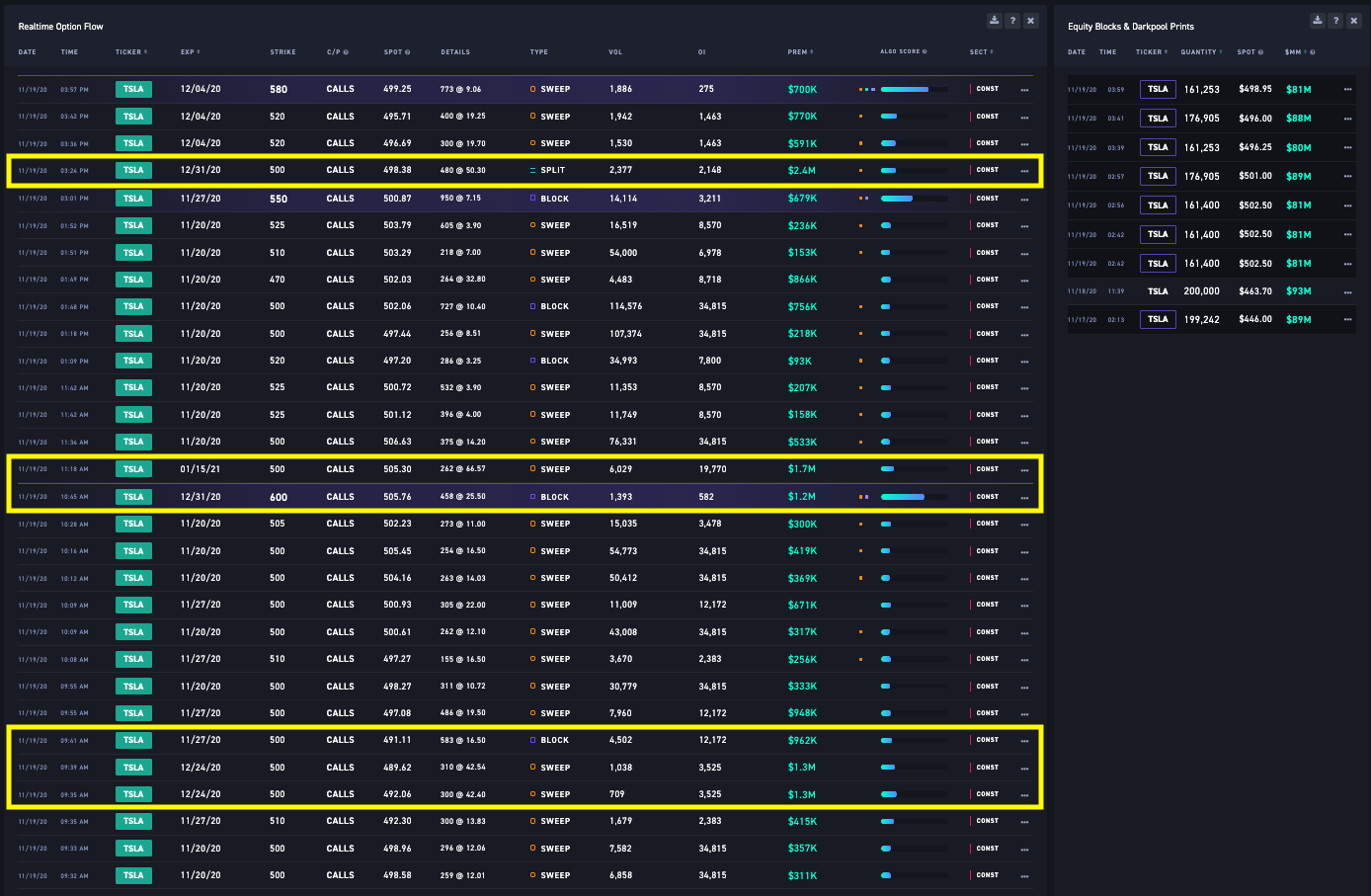

The following sequence analysis unpacks how Physik Invest traded equity and derivatives tied to the carmaker’s stock leading up to the December 21, 2020 index inclusion.

Note: Click here to view all transactions.

Sequence 1: On news of the inclusion, market participants initiated shares of Tesla out of balance, beyond trend resistance. Thereafter, in accordance with a typical give and go scenario, the stock faded, filling 50% of the low-volume area left after the initial move higher, before aggressive buying resurfaced to continue the new trend.

Through November 19, the following positions were added for a $61.00 debit, in total. At this point if all legs were to remain out of the money (i.e., expire worthless) by November 20, the maximum loss would be $61.00, approximately 1/10 of a standard risk unit, or the capital risked in a typical position.

- 500+1/530-2 call ratio spread

- 490+2/505-3 call ratio spread

- 525+1/550-2 call ratio spread

- 510+1/525-2 call ratio spread

- 445-1 put

- 460-1 put

By November 20, all aforementioned positions were closed for an $827.00 credit, a 1,255.74% return on initial investment.

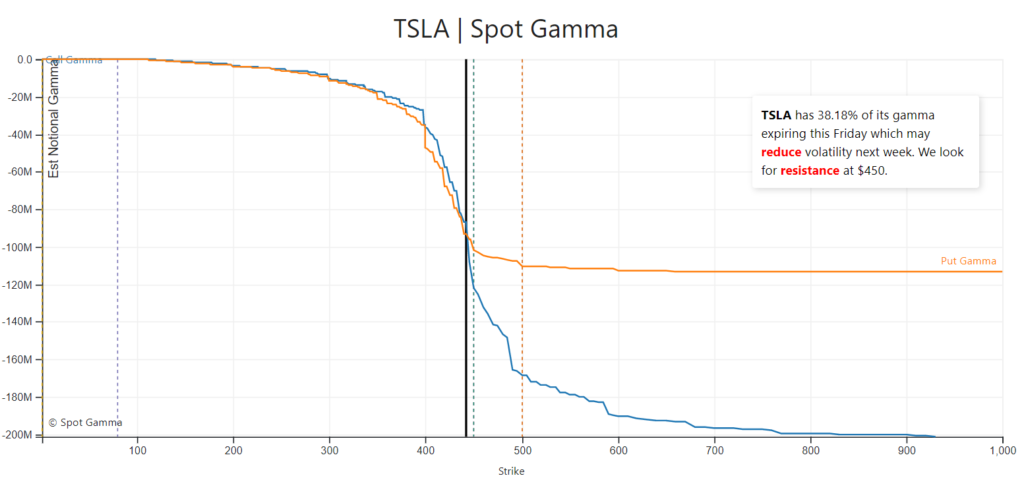

All the above call-side structures were initiated against the $500 high open interest strike. Reason being, option expiries mark an end to pinning (i.e, the theory that market makers and institutions short options move stocks to the point where the greatest dollar value of contracts will expire worthless) and the reduction dealer gamma exposure.

On November 20, nearly 40% of Tesla’s gamma was to roll off.

Moreover, since derivatives exposure was rolled into farther dated expiries, the stock would now be supported by dealers buying to hedge their derivatives exposure and facilitate the index inclusion.

Noting, at a simplistic level, prices often encounter resistance at prior highs due to the supply of old business. These areas take time to resolve. Breaking and establishing value (i.e., trading more than 15-minutes above this level) portends continuation.

Sequence 2: On November 20, the following structures expiring on December 4 were initiated for a $644.00 credit.

- 450-1 put

- 520+1/550-1 call ratio spread

- 570+1/600-2 call ratio spread

- 490-1/475+1 put ratio spread

Through November 24, the above structures were removed for a $876.00 credit.

Sequence 3: On November 24, the cost basis from November 19 ($61.00 debit) was reduced via an intraday long stock delta hedge that bought 10 shares at an average of $539.50.

The initial cost basis, after this particular trade, was brought down to a $0.20 debit.

Sequence 4: On November 25 the following positions were opened and closed the same day for a $179.30 credit.

- Bought stock at $550.14 average

- 480+1/500-2 call ratio spread

Sequence 5: On November 27, the following positions were initiated and closed by December 3 for a $117.10 debit.

- Bought stock at $595.55 average

- 475+1/437.5-2 put ratio spread

Sequence 6: On December 1 through December 3, the following positions were initiated, and then exited from by December 7 for a $1.77 debit.

- Bought stock at $589.20 average

- Bought stock at $563.77 average

- 740+1/780C-2 call ratio spread

Sequence 7: Through December 17, the following positions were initiated and closed for a total $452.30 credit.

- 720+1/820-2 call ratio spread

- 740+1/830-2 call ratio spread

- Bought stock at $632.17 average

- 720+1/820-2 call ratio spread

- Bought stock at $606.88 average

- 800+1/860-2 call ratio spread

- 500+1/480-2 put ratio spread

Sequence 8: From December 17 through December 23 the following positions were entered and exited from for a $322.00 credit.

- 500+2/450-4 put ratio spread

- 800+2/850-4 call ratio spread

- 670+1/685-2 call ratio spread

Summary: In total, the above sequence of trades net a $3,098.29 credit after commissions and fees.

The strategies employed were in accordance with Physik Invest’s methodology: the trade of ratioed, multi-leg strategies that combine short and long positions to reduce risk and increase returns.

Yes, in hindsight, one could have opted for something as simple as risk-reversals (e.g., buying calls and selling puts). However, the risks tied to such strategies are immense. By leveraging the dynamics of time and volatility, through complex spreads, risk was reduced.

Note: There were many times, during these sequences, that positions were structured in a way that would net no loss had the security moved sideways or lower into expiry.

Adding, per Fibonacci principles, one core aspect of Physik Invest’s market structure analysis, an upside target of $675.10 was established early on in the process. Tesla spent the majority of its December 18 session at this level.

Disclaimer: There is a $0.11 discrepancy between the transaction sheet and numbers provided in this case study. This is attributable to differences in rounding.