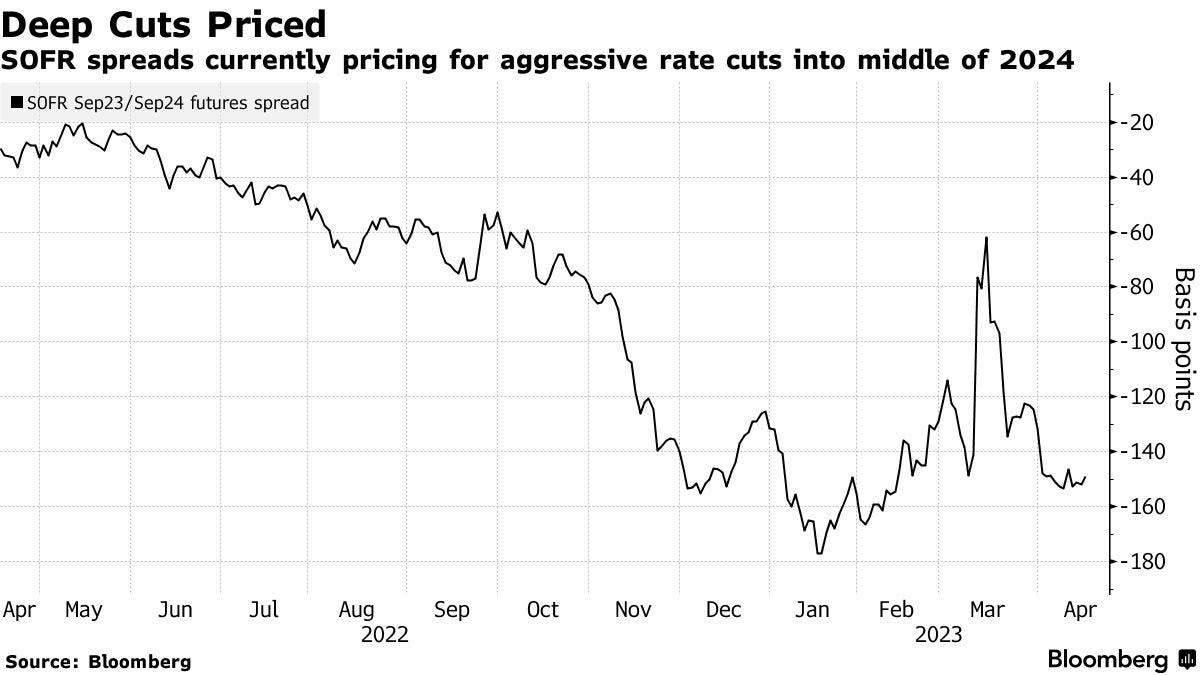

TD Securities said traders are not pricing in a large enough pivot.

“We look for cut pricing to increase even further,” strategists led by Priya Misra said, noting they expect cuts totaling 2.75% from December 2023 to September 2024.

This opposes Goldman Sachs’ view that investors have priced too much easing and will reverse their position in response to improving data and high inflation readings.

Regardless, a consensus is that rates will fall in the future and the economy will slow. Some traders are betting big on volatility, accordingly. The Ambrus Group’s Kris Sidial appeared on CNBC and elaborated.

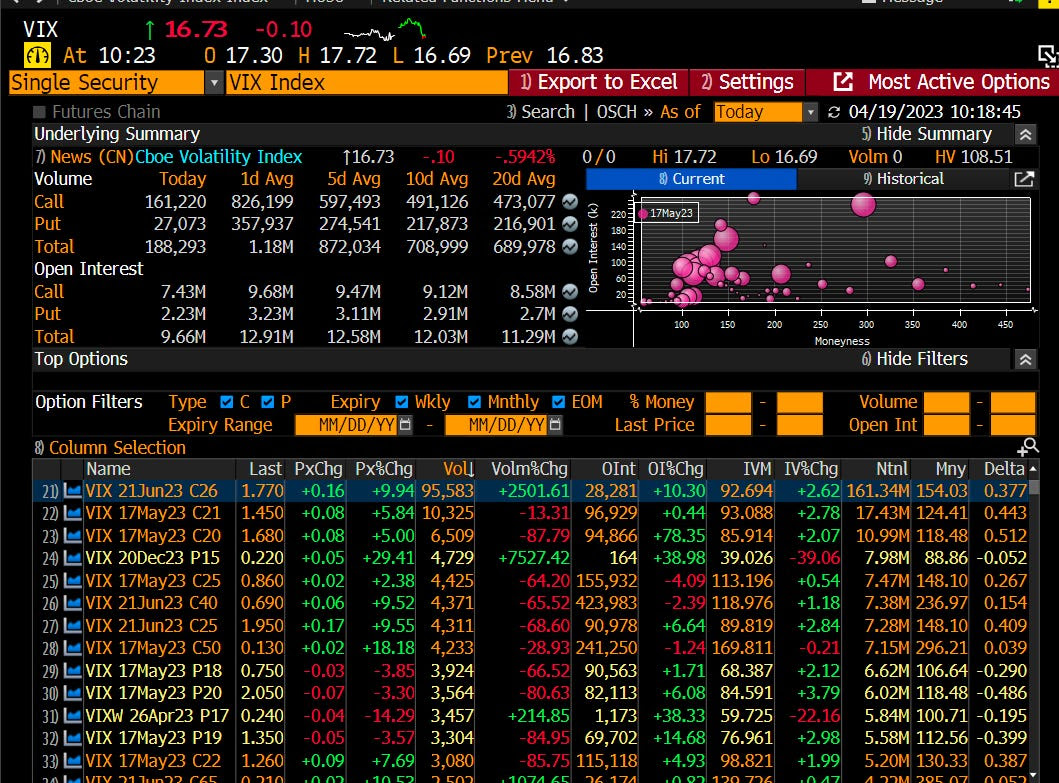

Before the last time the Cboe Volatility Index or VIX spiked to 30 from similarly low levels, very large VIX call buying was observed. Recently, a large buyer of June 26 calls at $1.71 on 94,000 contracts, worth about $16 million in premium, was seen.

“This is a pretty big bet in the VIX complex,” Sidial explained, adding that the VIX is a measure of variance. “When volatility starts to move, it moves at a higher rate than S&P volatility which is something that’s really important for the call option buyers.”

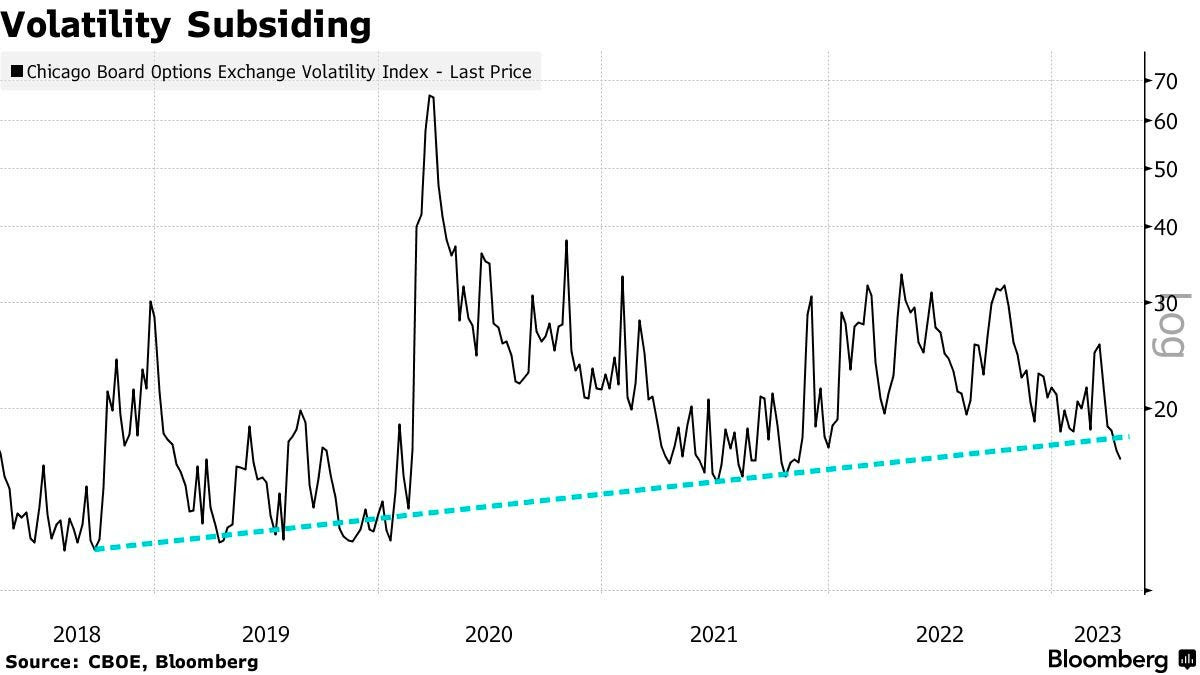

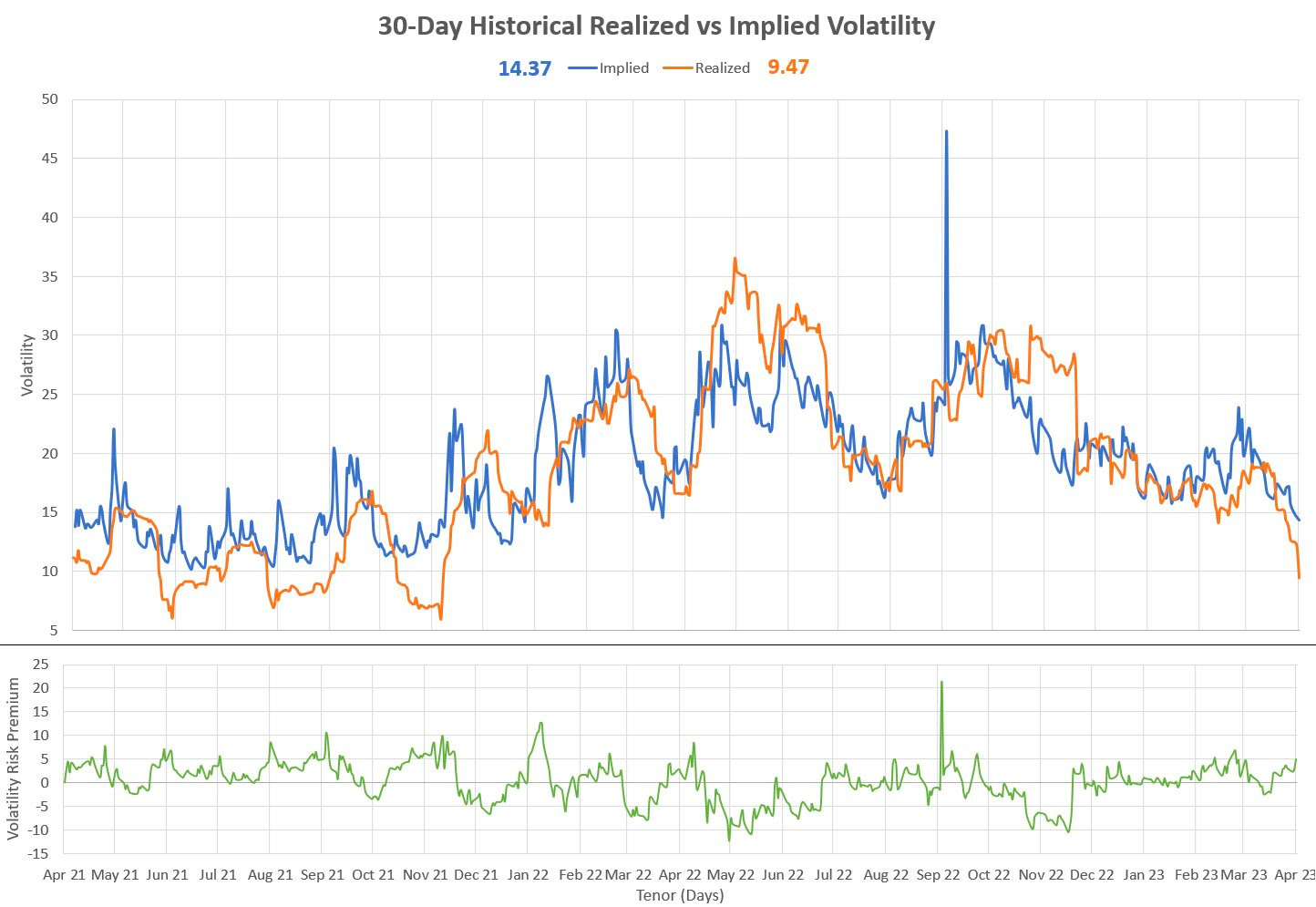

Bloomberg’s John Authers adds that the market’s hope of easing in the second half of the year is a reason for the low VIX. However, history suggests that rate cuts tend only to occur when the VIX exceeds its long-run average of 20.

Authers explains that the widening gap between the implied volatility (IVOL) metrics of Treasury and equity markets, which have historically had a high correlation, is also a concern. This is partly what may have inspired the purchase of the VIX protection Sidial elaborated on; such gaps could portend more equity volatility.

Notwithstanding, with the VIX near its average and trading at some premium to one-month realized volatility (RVOL), we may “see more systematic vol sellers make a comeback amid VIX contango, juicy VRP, and vol underperformance,” says Sergei Perfiliev. In such a case, markets may remain contained and bets on big market movements (e.g., the VIX trade detailed by Sidial) may not work that well.

It may be better for traders to limit their expectations and stay the course: buy call structures on weakness and monetize them into strength to finance put structures. Alternatively, define risk and enhance yield with short volatility bets, skewing them based on directional opinion (e.g., skewed iron condor), or get into risk-free and interest bearing assets (e.g., money market funds or box spreads). We covered this and more much better in a detailed research-type note soon to be released for public viewing. Stay tuned and watch your risk. PS: Sorry for the delay and rushed note!

About

Welcome to the Daily Brief by Physik Invest, a soon-to-launch research, consulting, trading, and asset management solutions provider. Learn about our origin story here, and consider subscribing for daily updates on the critical contexts that could lend to future market movement.

Separately, please don’t use this free letter as advice; all content is for informational purposes, and derivatives carry a substantial risk of loss. At this time, Capelj and Physik Invest, non-professional advisors, will never solicit others for capital or collect fees and disbursements. Separately, you may view this letter’s content calendar at this link.