What Happened: On June 23, 2021, shares of Tesla Inc (NASDAQ: TSLA) surged on news the company opened a Chinese-based solar-powered charging station with on-site power storage.

Prior to the development, the stock endured months of corrective activity during which negative narratives were out in full force. From calls against Tesla’s biggest bull – ARK Invest – to famed Michael Burry’s synthetic short position on the stock, it seemed as though the end was near.

However, as evidenced by Tesla’s June 23 breakout from consolidation and subsequent upside continuation in light of a 300,000 vehicle recall in China, it is obvious the fear was unwarranted.

Those who understand that markets are most influenced by credit and positioning knew this all along.

Taking a look at market liquidity metrics – such as those offered by services like HFT Alert – market participants had been aggressively accumulating shares of the company from its mid-May low.

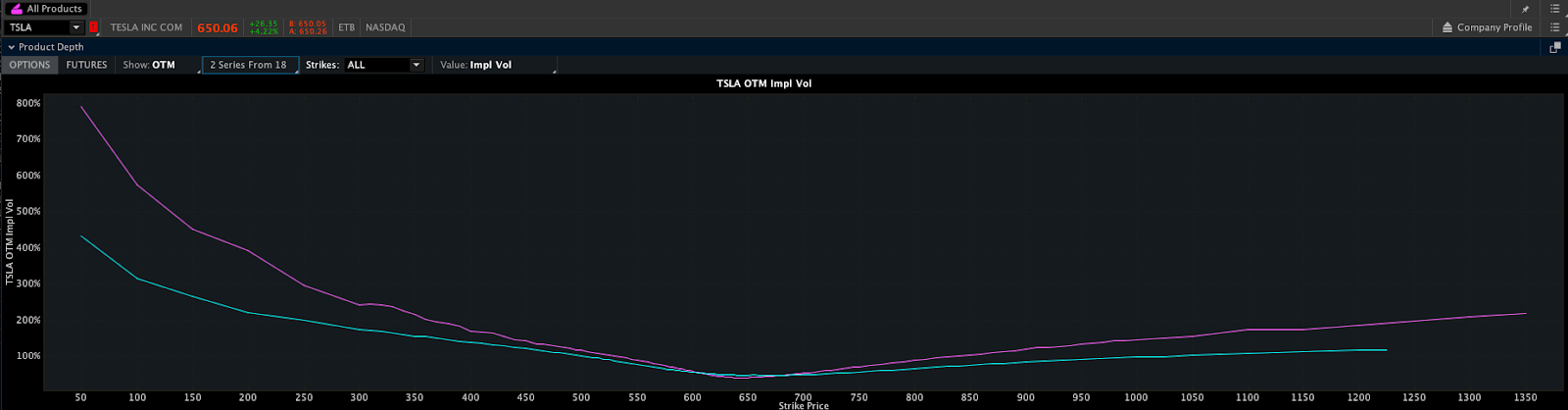

Still, with skepticism out in full force, there was a heightened demand for protection, as evidenced by metrics like volatility skew, in options at and below the current stock price.

Skew: The difference in implied volatility (IV) – an estimate of potential price changes given the fear of movement – between option strikes that are close and far from the underlying stock price.

To put it simply, the fear of corrective activity in Tesla fueled demand for protection via put option strikes farther below the stock. This, in turn, bid volatility in downside strikes, more than upside strikes. Because volatility is input in option pricing models, put options, further down the chain, were valued more relative to their call-side counterparts.

Given this dynamic, the following sequence analysis unpacks how Physik Invest traded options tied to the carmaker leading up to, and through, the June 23, 2021 upside consolidation break.

Note: Click here to view all transactions. Adding, positions were structured in a way that would potentially net higher credits had the stock moved markedly lower or higher.

Sequence 1: After skew was observed, through 6/18/2021, the following positions were initiated against the $500 support level for a $1,011.00 credit.

- June 11 Expiry 500P+1, 450P-2

- June 25 Expiry 490P+9, 440P-18

- June 25 Expiry 550P+2, 500P-4

- June 25 Expiry 300P+2

By 6/21/2021, all aforementioned positions were closed for a $271.00 debit, netting a $691.58 credit after commissions and fees.

Sequence 2: Through 6/29/2021, skew improved and the following positions were initiated for a $5,651.38 credit.

- July 2 Expiry 500P+3, 450P-6

- July 2 Expiry 525P+7, 475P-14

- July 2 Expiry 545P+1, 495P-2

- July 9 Expiry 850C+2, 900C-4

- July 9 Expiry 580P+11, 530P-22

- July 9 Expiry 350P+3

- July 16 Expiry 850C+4, 900C-8

Through 7/12/2021, the above structures were removed for a $90.00 debit, netting a $5,443.93 credit after commissions and fees.

Sequence 3: Through 7/6/2021, skew remained and the following positions were initiated for a $3,566.00 credit.

- July 16 Expiry 575P+11, 525P-22

- July 16 Expiry 600P+1, 550P-2

- July 16 Expiry 350P+3

Through 7/14/2021, the above structures were removed for a $473.00 debit, netting a $3,043.29 credit after commissions and fees.

Summary: In total, the sequence of trades net a $9,178.80 credit after commissions and fees.

The above strategies were employed per Physik Invest’s core edge: the trade of ratioed, multi-leg strategies that combine short and long positions to reduce risk and increase returns.

By leveraging the dynamics of time and volatility, through complex spreads, Physik Invest was paid to express a neutral stance on underlying Tesla stock with the potential to further capitalize on an expansion of range in either direction.

Disclaimer: There is a $0.77 discrepancy between the transaction sheet and the numbers provided in this case study. This is attributable to differences in rounding.