The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 300+ that read this report daily, below!

What Happened

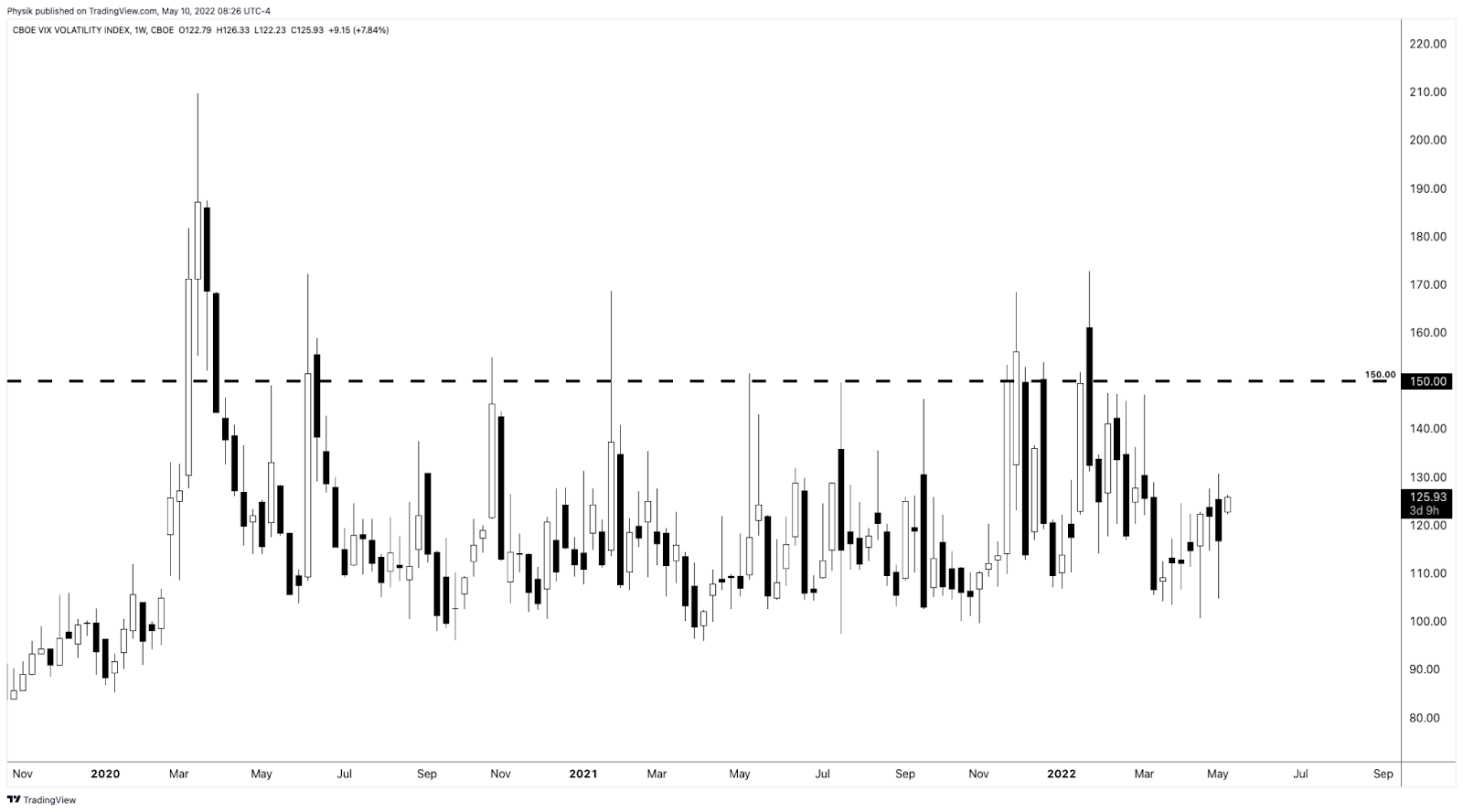

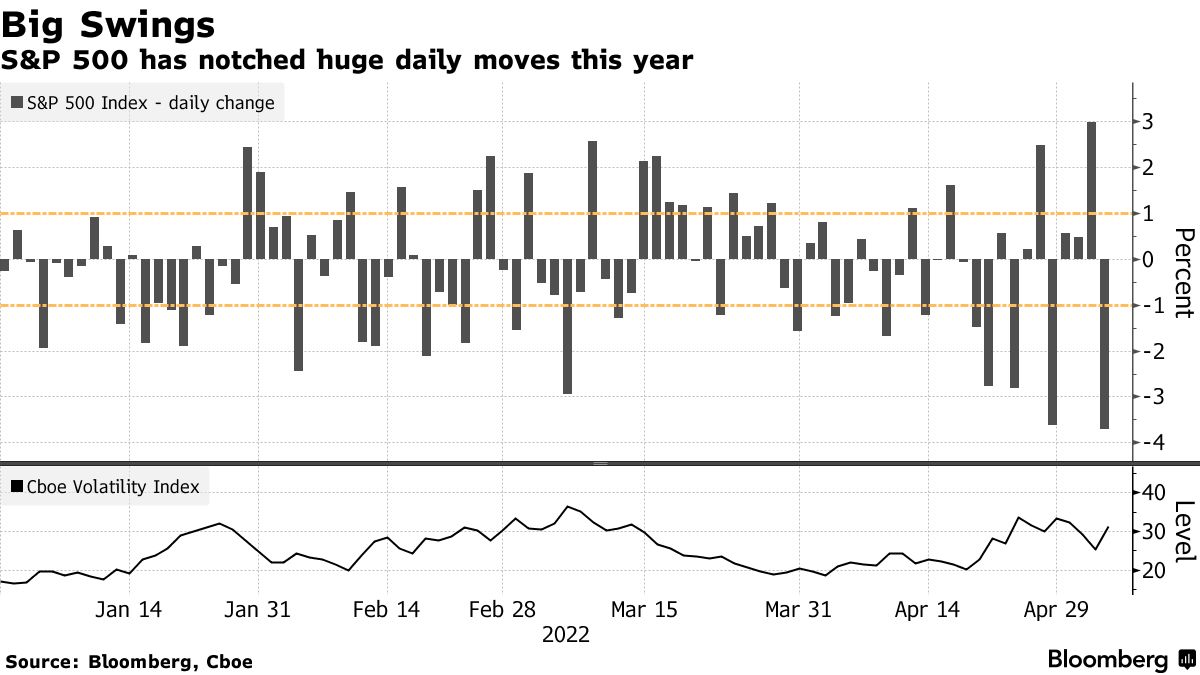

Overnight, equity indices auctioned lower alongside commodities and bonds. The Cboe Volatility Index (INDEX: VIX) caught a bid ahead of its large expiration this morning.

Fundamentally, the context is the same. To note, Federal Reserve Chair Jerome Powell was at a conference, yesterday, and said the central bank would continue raising rates until there is evidence that inflation is in retreat.

Until that evidence appears, the Fed could move “more aggressively.” That was hawkish.

Today we receive updates on building permits and housing starts (8:30 AM ET). Later, Philadelphia Fed President Patrick Harker speaks (4:00 PM ET).

What To Expect

Fundamental: If you have not already, check out Tuesday’s letter which discussed, in-depth, some of the implications of changing monetary policies, and their impact on markets.

Today’s letter will add to our narrative.

Over the course of a month or so, markets traded marginally lower while research houses have upped their calls for a slowing in the economy or, even, the prospect of a global recession.

So, in the span of a month, the tone changed to “[w]e’re on the brink of global recession.”

Let’s try to work through some narrative and theory, here.

On March 31, 2022, we unpacked what carry trades are (i.e., the act of borrowing at low rates and investing where there are higher rates to make money so long as nothing [bad] happens), and the implications of their unwind.

Such strategies are characterized by a sawtooth wave returns pattern (i.e., steady positive returns followed by sharp drops).

A great book on this – “The Rise of Carry: The Dangerous Consequences of Volatility Suppression and the New Financial Order of Decay Growth and Recurring Crisis – discusses many of the different forms of carry, their attractiveness, and the implications of their failure.

Further discussed is global monetary policy feeding into the growth and the reinforcement of carry, which has become embedded (or a core force of financial conditions).

Let’s elaborate.

Carry trades often involve leverage and, to avoid losses, these strategies force traders to close positions when positions move against them, buying strength and selling weakness.

By that token, expansion of carry plays into increased liquidity, which is related to the ease with which credit is obtained and available in the economy, a driver of economic growth and what we talked about yesterday – Planet Palo Alto – over recent business cycles.

Moreover, over the last four decades, monetary policy was a go-to for supporting the economy. Money was sent to capital and that promoted innovation and, by that token, deflation, ultimately creating “a disinterest and unimportance to cash flows.”

In other words, prevailing monetary policies made it easier to borrow and make longer duration bets on ideas with a lot of promise in the future. Central banks underwrote losses of this regime (e.g., post-1998 easing after widening of credit spreads), encouraging continued growth (and innovation).

Now, there’s a strong commitment to reducing liquidity and credit.

This has consequences on the real economy and asset prices, accordingly, which rose and kept deflationary pressures at bay.

What we’re getting to basically is the distinction between the economy and financial markets.

This distinction has blurred.

As the book explains, U.S. market liquidity, as well as the U.S. dollar’s role as a global reserve currency, makes the U.S. markets and S&P 500 at the center of the global carry regime.

A stock market drop is both a recession and a direct reflection of the unwind of carry. It is the manifestation of a deflationary shock, and today’s sentiment reflects this.

So, what?

Yesterday, we quoted Elon Musk saying the U.S. was facing a tough recession. This is on the heels of a large “misallocation of capital,” he says, by the government printing “a zillion amount of more money than it had,” which ultimately played into price instabilities we’re seeing today.

“The Fed has a mandate, which is completely unreasonable — to control price stability,” Kai Volatility’s Cem Karsan explains.

“With supply-side economics, the only way that they can control this ultimately is to pull back. And slow capital markets decrease via the wealth effect. Ultimately, there’s a significant lag, so they are not in a position to ultimately control inflation without bringing down markets.”

“Unfortunately for the Fed, the U.S. economic growth rate is already decelerating,” Lyn Alden of Lyn Alden Investment Strategy adds. To cut inflation, the Fed must reduce demand for goods, and this is recessionary (just as “Walmart Inc [NYSE: WMT] and Target Corporation [NYSE: TGT] are feeling the effect of the stretched consumer,” per Bloomberg).

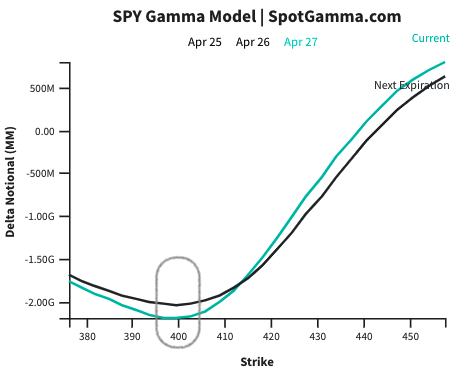

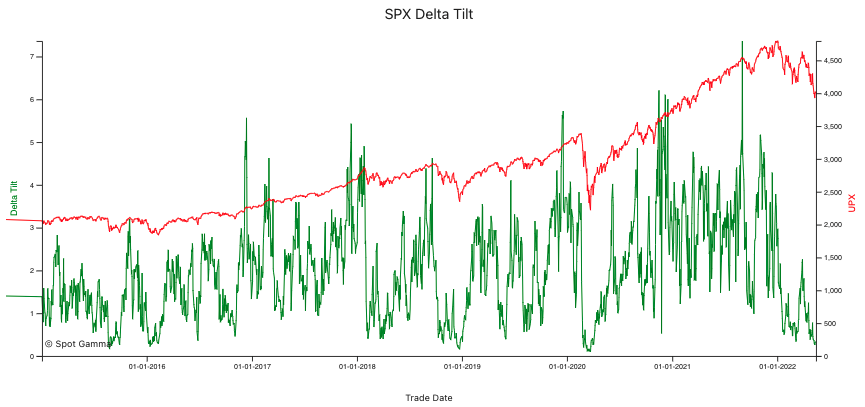

Positioning: Participants legged into protective put options.

As talked about before, with this stretched positioning, liquidity providers had a lot of synthetic exposure to the upside (positive delta) and asymmetric losses to the downside (negative gamma). To hedge, underlyings were sold.

As markets rise, and that particular options exposure decays, the pressure these liquidity providers must add, softens. That’s what we’ve been seeing over the past few sessions.

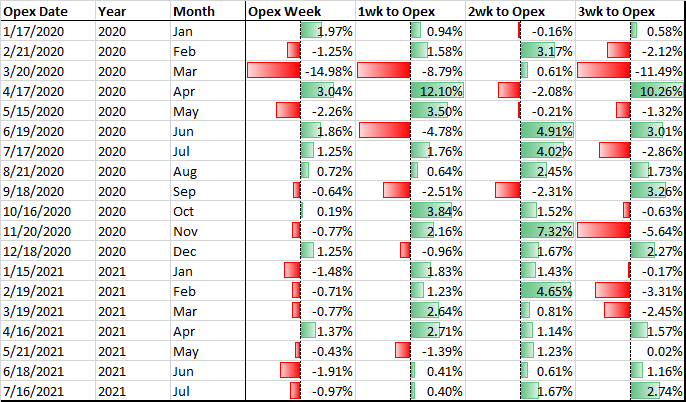

If participants were to continue trading in this manner, that may offer markets additional support. Notwithstanding, this activity likely does little to disrupt the balance of trade heading into and around the May 2022 options expiration (OPEX).

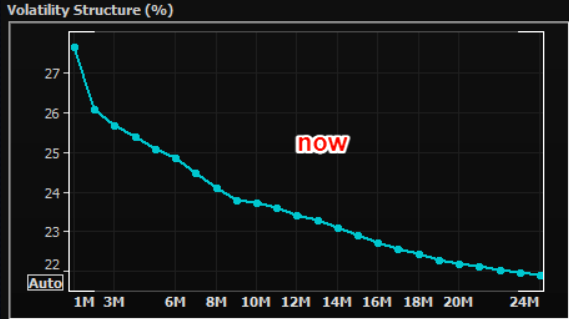

Into that event, we expect delta hedging flows with respect to changes in time (charm), mainly, and volatility (vanna) to provide an added boost. However, with volatility coming in from lower levels, SpotGamma says, there’s not as much “stored energy to catalyze a rally.”

Instead, SpotGamma adds, “[o]ur fear, here, is that, fundamentally, markets are weak and the May OPEX opens the door for lower lows as some of the ‘max put’ positioning is cleared and markets succumb to the remaining negative gamma positioning.”

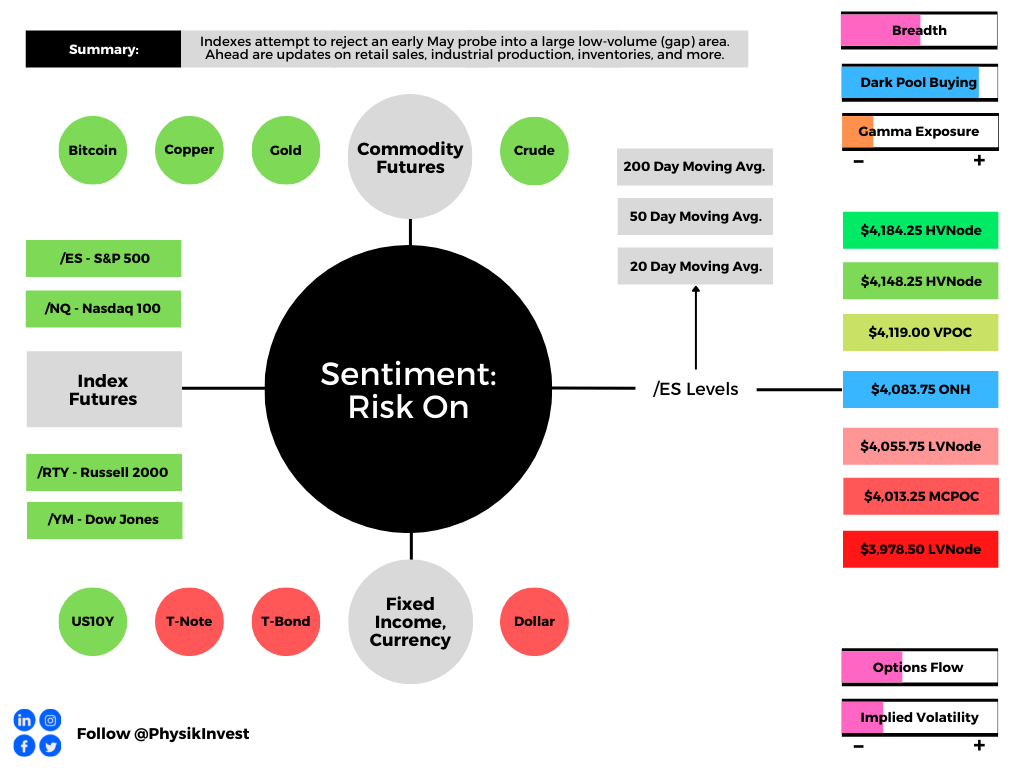

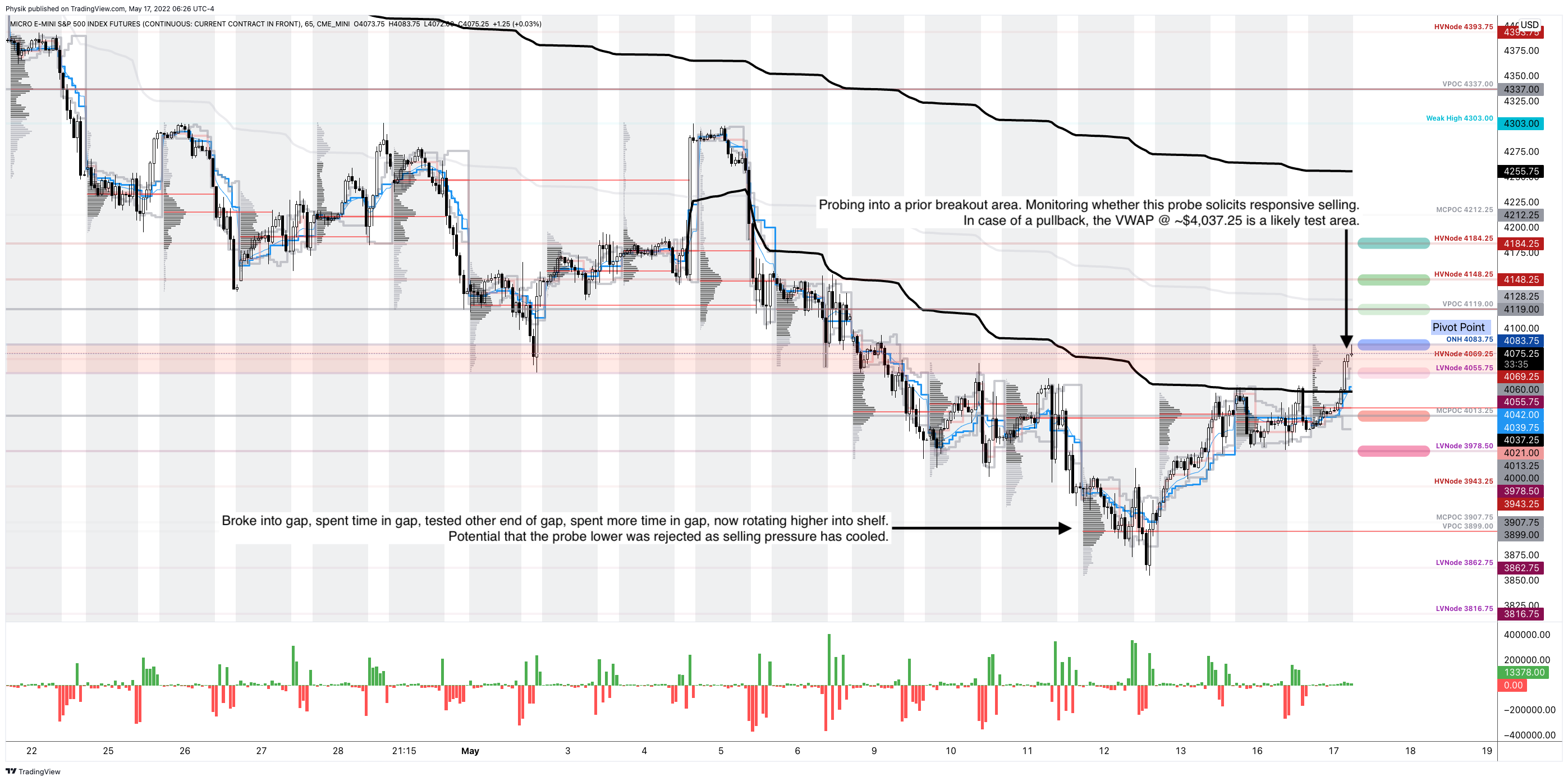

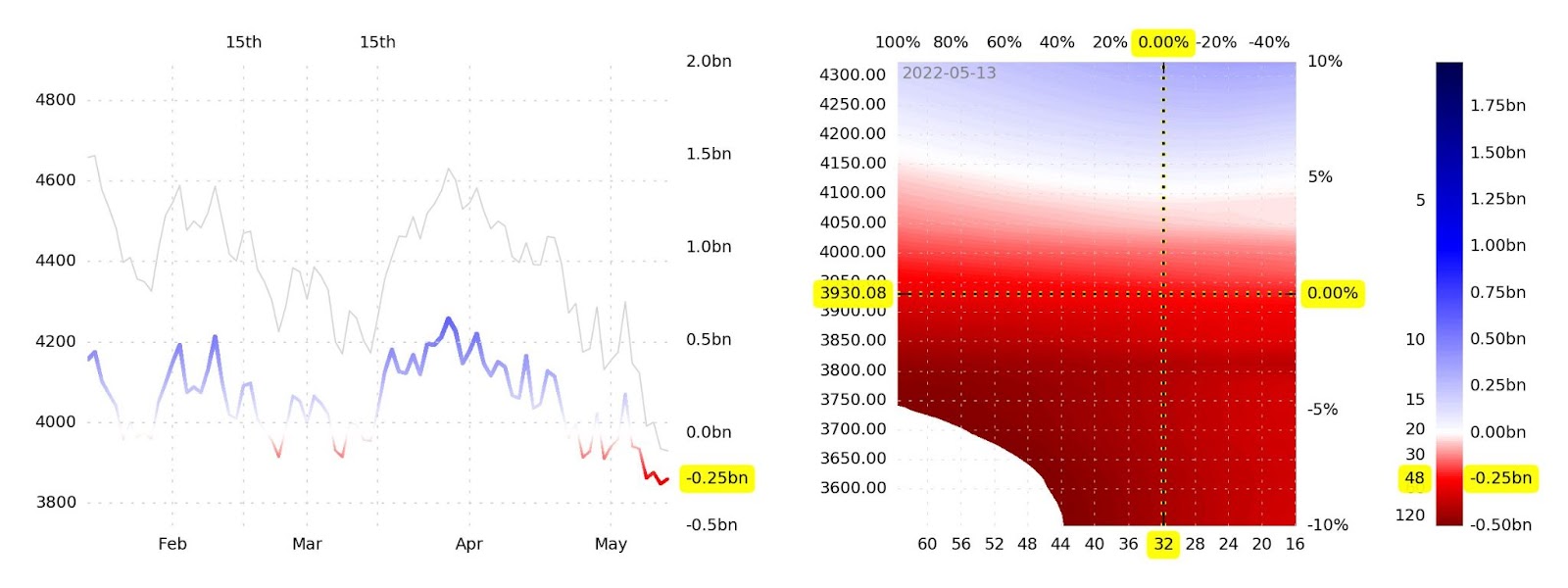

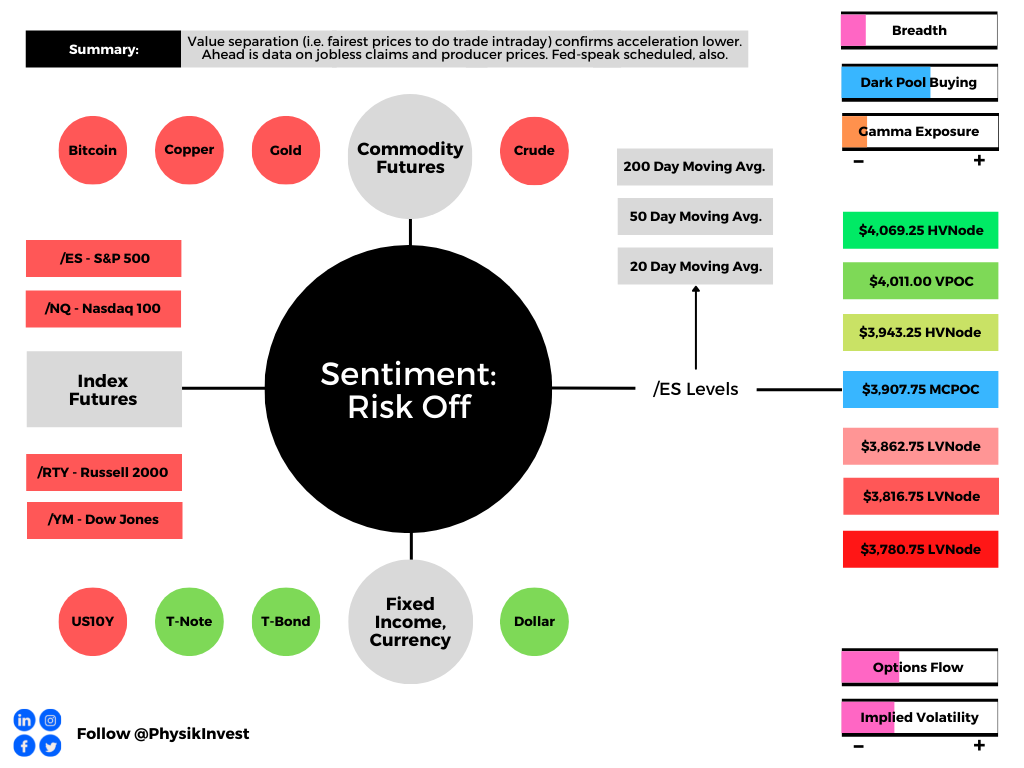

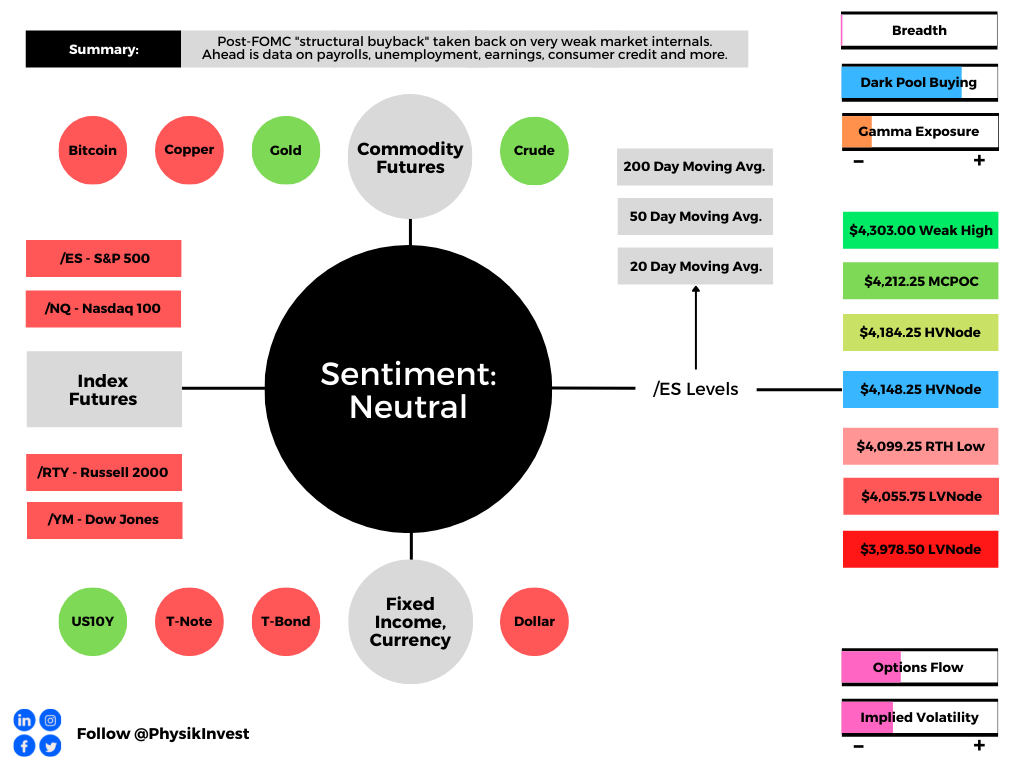

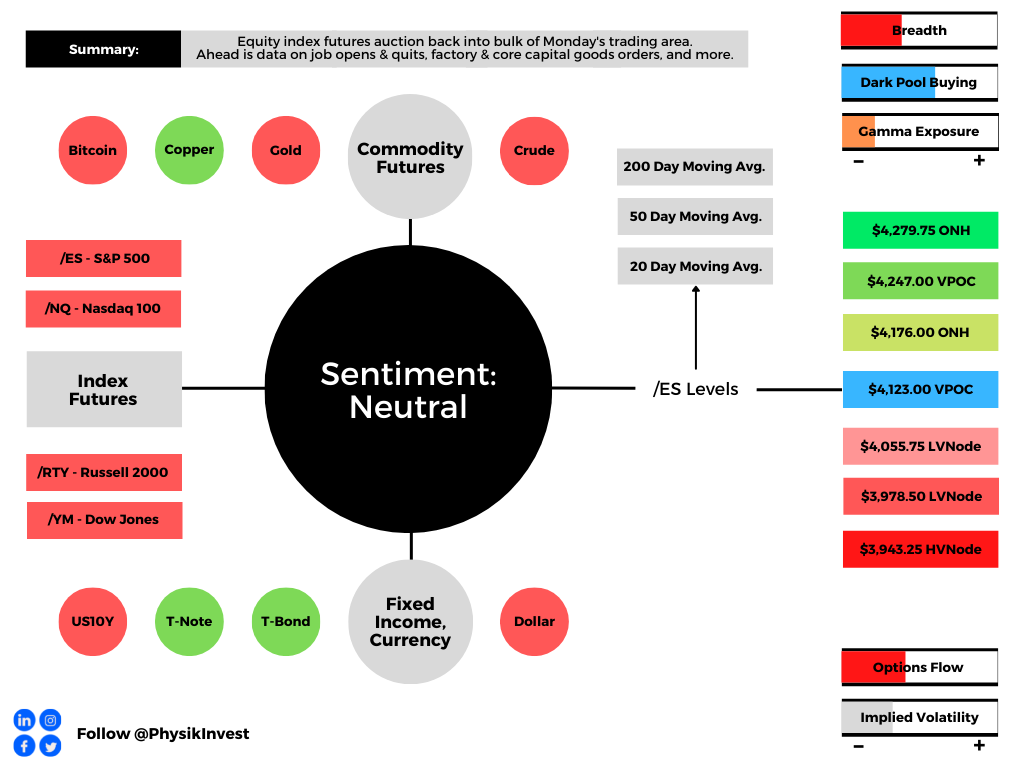

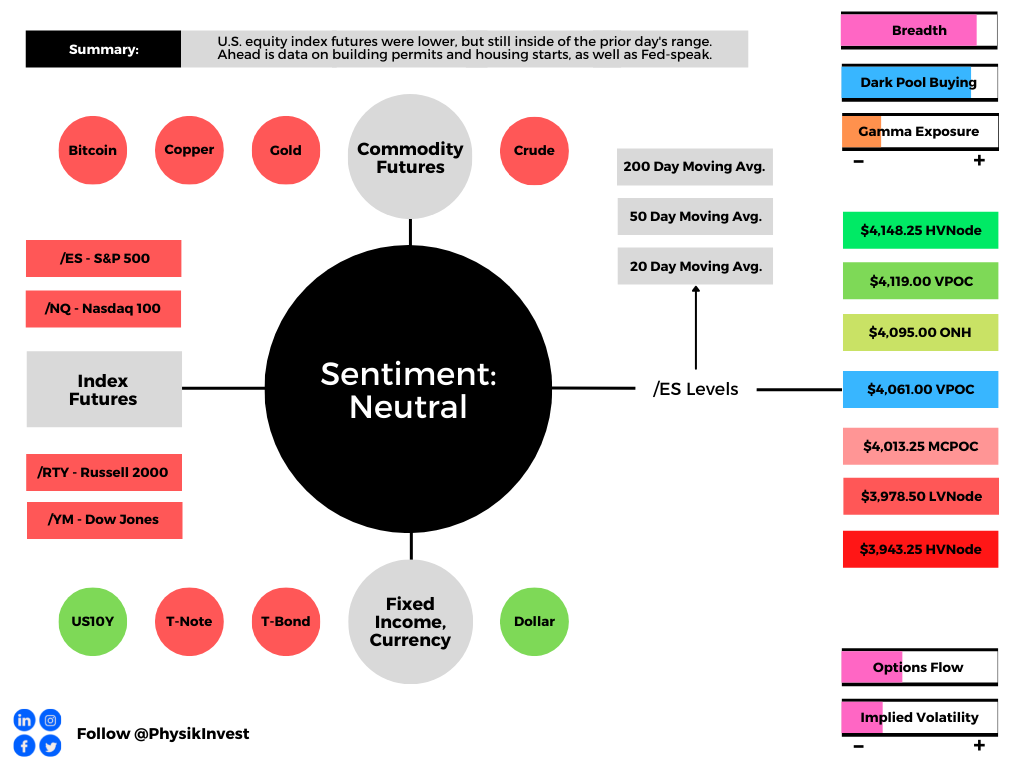

Technical: As of 6:30 AM ET, Wednesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the lower part of a negatively skewed overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

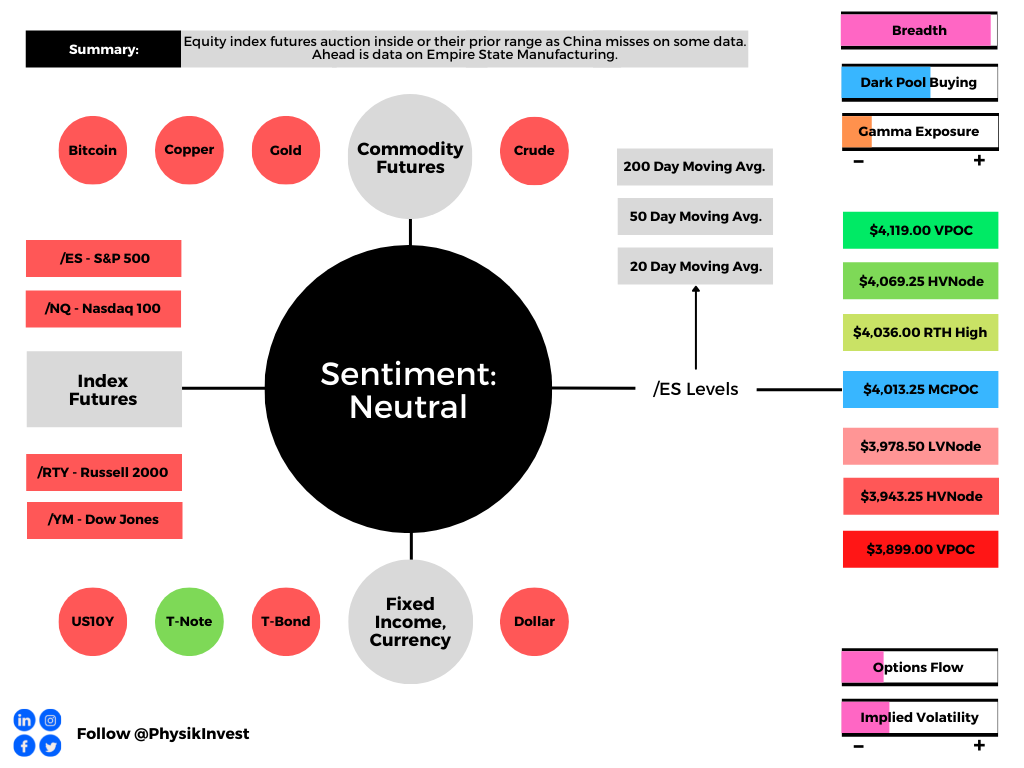

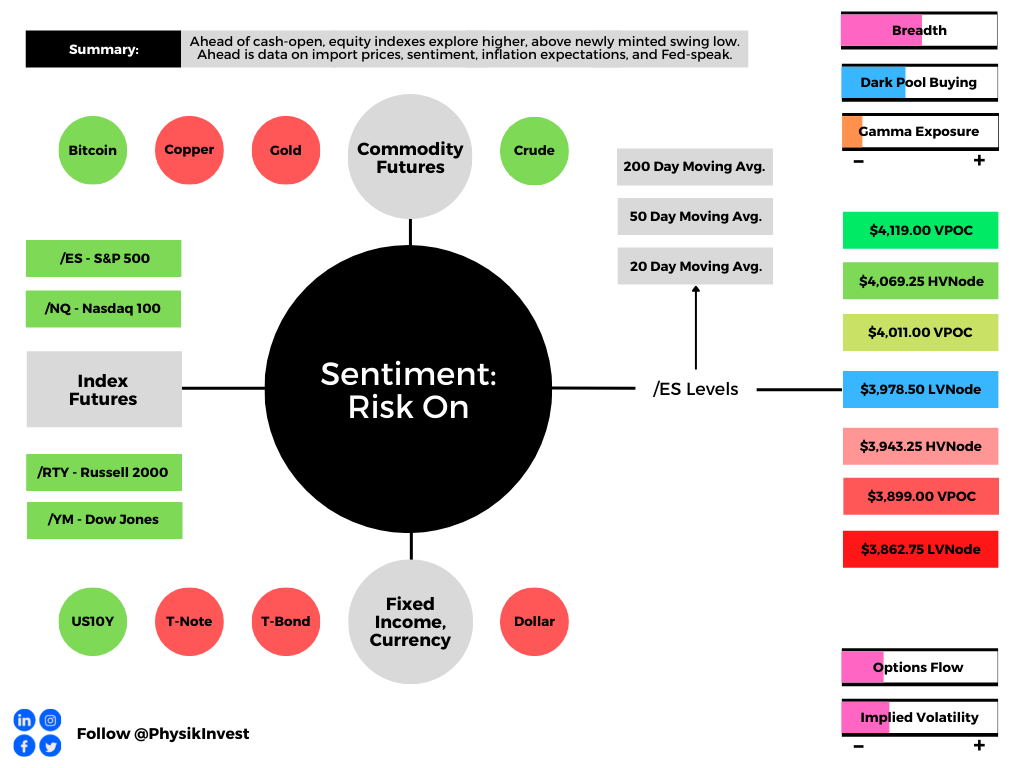

In the best case, the S&P 500 trades higher; activity above the $4,061.00 untested point of control (VPOC) puts in play the $4,095.00 overnight high (ONH). Initiative trade beyond the ONH could reach as high as the $4,119.00 VPOC and $4,148.25 high volume area (HVNode), or higher.

In the worst case, the S&P 500 trades lower; activity below the $4,061.00 VPOC puts in play the $4,013.25 micro composite point of control (MCPOC). Initiative trade beyond the MCPOC could reach as low as the $3,978.50 low volume area (LVNode) and $3,943.25 HVNode, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Definitions

Overnight Rally Highs (Lows): Typically, there is a low historical probability associated with overnight rally-highs (lows) ending the upside (downside) discovery process.

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

Some of his works include conversations with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, FTX’s Sam Bankman-Fried, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, among many others.

Disclaimer

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.