The daily brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 300+ that read this report daily, below!

What Happened

Overnight, equity index futures softened after what appeared to be continued covering of shorts into Monday’s close. Commodities were mixed, bonds higher, and implied volatility higher.

In the news the amount of money parked at major Federal Reserve facilities climbed to another all-time high, passing $2 trillion. JPMorgan Chase & Co’s (NYSE: JPM) CEO Jamie Dimon said recently that the Fed must do quantitative tightening since there’s too much liquidity in the pipes.

Adding, the Fed’s Raphael Bostic said policymakers may hike rates by 0.50 basis points after their next two meetings before pausing in September to allow for observation. This is as banks UBS Group AG (NYSE: UBS) and JPMorgan Chase & Co cut their expectations for growth here and abroad.

Ahead is data on S&P Global Inc (NYSE: SPGI) manufacturing and services (9:45 AM ET). Later, participants get updates on new home sales (10:00 AM ET) and Fed-speak by Chair Jerome Powell. Later this week, on Wednesday, participants will receive minutes of the Fed’s most recent meeting which may provide further insight into the central bank’s intent to tighten.

What To Expect

Fundamental: So long as market participants are using JPEG images of rocks as collateral for debt, it is likely we have not reached a more permanent bottom in the broad market.

Kidding – just trying to lighten the mood, haha! Sorry to my crypto friends! For real, though, maybe the destruction of that market is what we’re to watch for.

Support of market excesses was liquidity in the financial system, a lot of which is now piling into the Fed’s overnight reverse repurchase agreement facility (RRPs).

Since the start of the year, however, the anticipation and pricing in of the removal of some of this liquidity have fed into market weaknesses.

Per the Damped Spring Advisors’ Andy Constan, the “Fed will reduce their balance sheet by choosing not to reinvest the proceeds of maturity payments of existing holdings back into the market. The U.S. Treasury will need to find new buyers for the bonds it issues.”

Please read our Daily Brief For May 5, 2022, here, for more on the Federal Reserve’s updates.

On June 1, the Fed will start the process of balance sheet reduction at $47.5 billion ($30B UST and $17.5B MBS) a month for the first three months. This will increase to $95 billion ($60B UST and $35B MBS), after, about double the maximum pace of $50 billion a month in 2017-2019.

Constan adds: “In June, that supply those markets will need to absorb will be $50 billion USD and will grow to $95 billion (of which some will be outright sales of mortgages by the Fed).”

Accordingly, “[j]ust as USD strength occurred as global investors chased U.S. assets, as the U.S. economy led the global economy out of the Covid chasm, the next leg of asset returns is more likely in countries that remain relatively easy and where the economy is still lagging.”

Goldman Sachs Group Inc’s (NYSE: GS) Vickie Chang notes: “Using history as a guide, in order for equities to come off their recent lows (and stop declining), this kind of monetary-tightening induced contraction is most likely to end when the Fed itself shifts.”

“It may be that the market needs to see signs of the inflation deceleration that our US economists expect in the second half of the year in order to see sustained relief.”

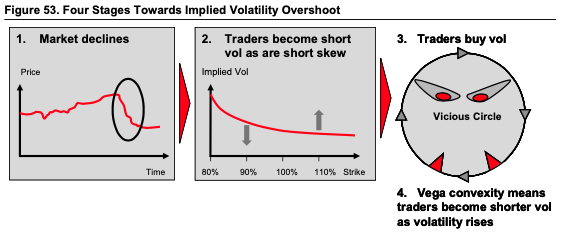

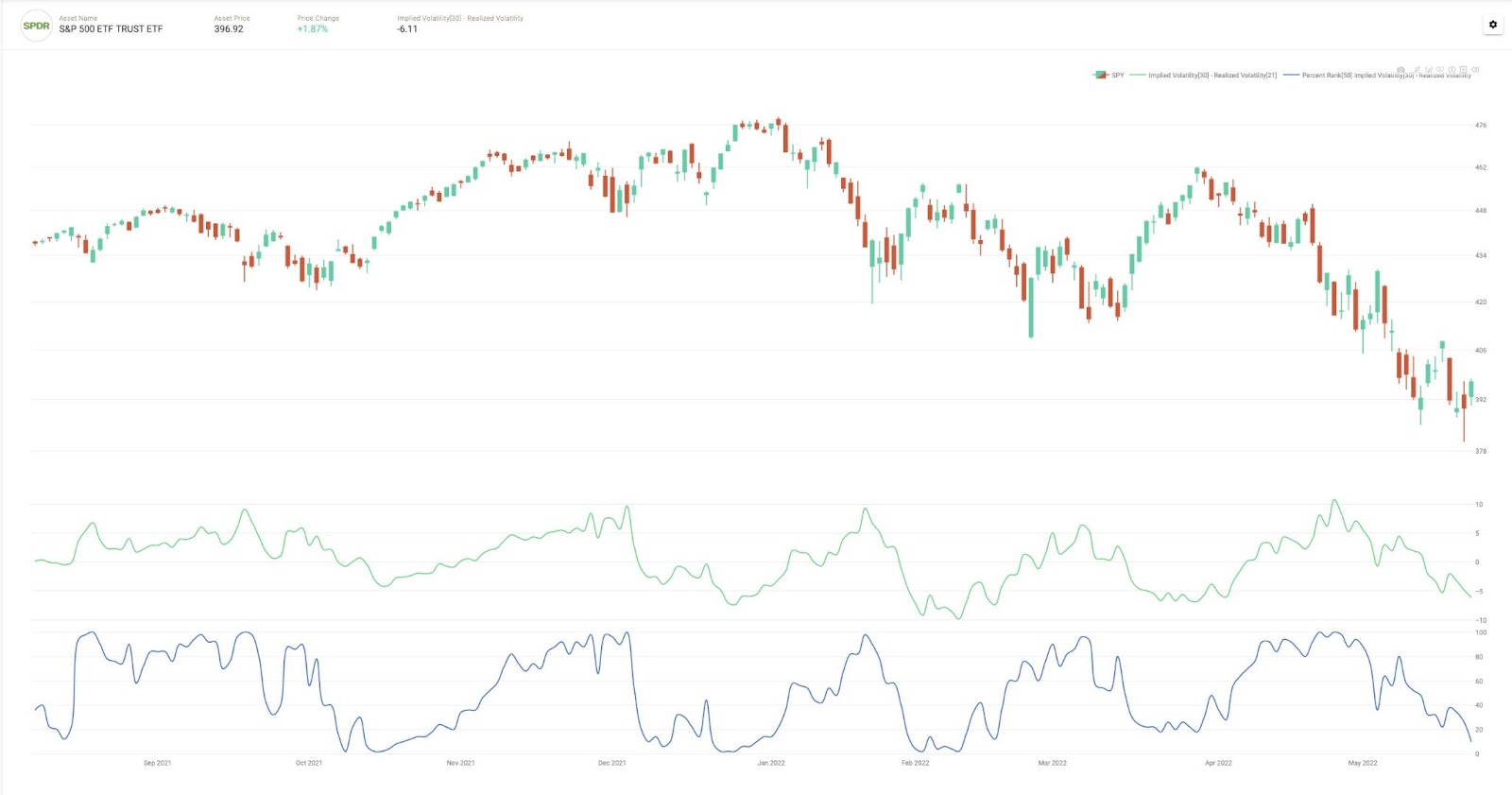

Positioning: Pursuant to comments established last week, Dennis Davitt of Millbank Dartmoor Portsmouth explains that the “realized volatility of the underlying S&P 500 is above 27% … with implied volatility of options trading between 24%-27%,” which translates to a VIX at 30%.

“It is profitable to own options with such an active and volatile cash market. This is the opposite of 2017 where the VIX was at 10% and the realized was 7%,” a trade that leverage poured into and resulted in the spectacular short-volatility ‘Volmageddon’ blow-up in February of 2018.

What does this mean?

Davitt concludes that “18 months” out there are “elevated option prices which may foretell an increase in the volatility of the equity market through this time next year.”

Though the Cboe Volatility Index (INDEX: VIX) may print higher, it is likely that it does not spike and point to an immediate market bottom, all else equal, like it has in the very near past.

How to play?

It makes more sense to have exposure to underlying markets, synthetically (i.e., own options). This is based on the current relationship between realized and implied volatility.

This is in contrast to the thesis that “long volatility is a poor equity hedge” because, on average, it’s overpriced and has less than a 100% negative correlation with the equity market.

Given fundamental contexts, many foresee continued weaknesses. Notwithstanding, markets are stretched to the downside and the path of least resistance, based on prior comments, is up.

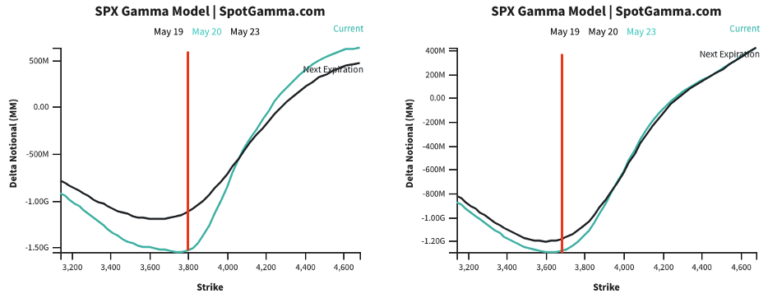

This is with the caveat that traders should look at the current window of time as a period during which markets have less pressure to rally against. Per SpotGamma, this is due to the put-heavy options expiration (OPEX), Friday.

Still, the rally into Monday “pulled forward some of the energy from [those] options that were to roll off,” and now, participants are “much less hedged than they were.” Should demand return, that will bid options prices and likely solicit liquidity provider pressures which, all else equal, start to cool into the $3,700.00 S&P 500 area.

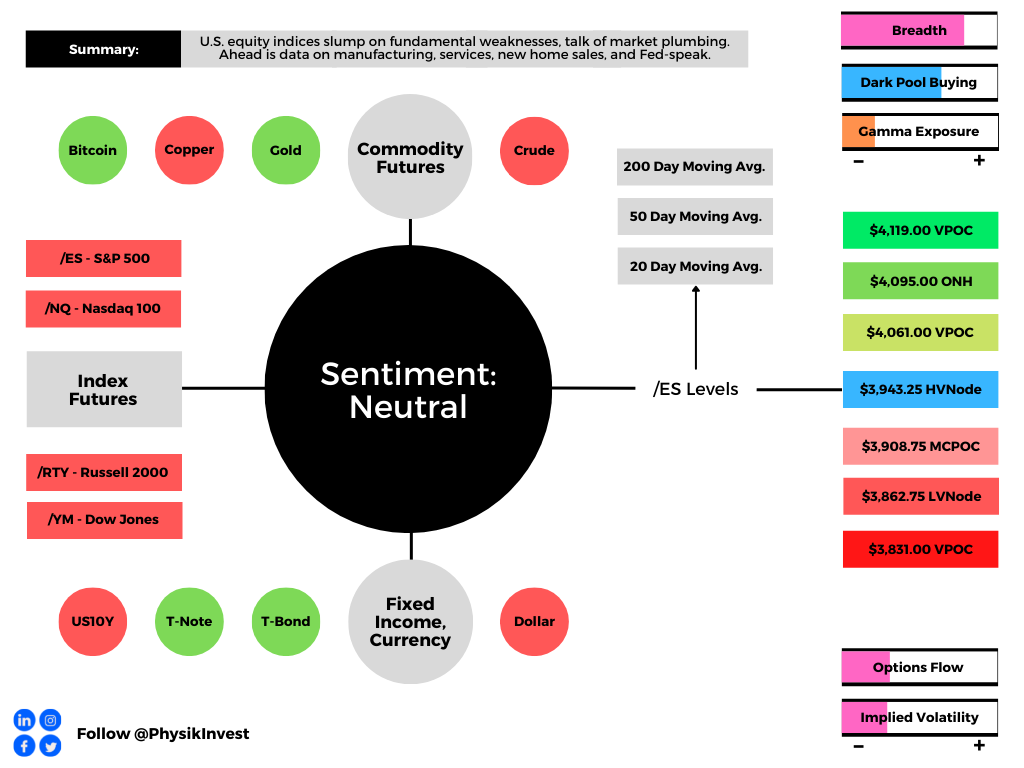

Technical: As of 6:15 AM ET, Tuesday’s regular session (9:30 AM – 4:00 PM ET), in the S&P 500, will likely open in the middle part of a negatively skewed overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher; activity above the $3,943.25 HVNode puts in play the $3,969.00 VPOC. Initiative trade beyond the VPOC could reach as high as the $4,061.00 VPOC and $4,095.00 ONH, or higher.

In the worst case, the S&P 500 trades lower; activity below the $3,943.25 HVNode puts in play the $3,908.75 MCPOC. Initiative trade beyond the MCPOC could reach as low as the $3,862.75 LVNode and $3,831.00 VPOC, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Considerations: Push-and-pull, as well as responsiveness near key-technical areas (discernable visually on a chart), suggests technically-driven traders with shorter time horizons are very active.

Such traders often lack the wherewithal to defend retests.

Large participants (who often move by committee) seldom respond to key technical inflections. It is their activity that often results in poor reliability of our technical levels.

Sometimes, the better trade is to wait for the larger participants’ entry and use the expansion of the range as a confirmation of a new trend.

Catalysts to consider include the release of Federal Open Market Committee (FOMC) minutes, Wednesday.

Definitions

Overnight Highs And Lows (ONH and ONL): Typically, there is a low historical probability associated with overnight rally-highs (lows) ending the upside (downside) discovery process.

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent in a prior day session. Participants will respond to future tests of value as they offer favorable entry and exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

Some of his works include conversations with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, FTX’s Sam Bankman-Fried, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, among many others.

Disclaimer

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.

3 replies on “Daily Brief For May 24, 2022”

[…] In yesterday’s in-depth write-up, we talked about the underperformance of implied volatility (IVOL), relative to that which is […]

[…] It remains profitable to own options structures as implied (IVOL) underprices the volatility which is realized […]

[…] Read: Daily Brief for May 24, 2022. […]