Market Commentary

U.S. equity index futures sideways overnight.

- PBOC cut RRR, tax talk, and virus.

- Ahead: WASDE, Fed speak, G20.

- SPX, RUT, DJI weak. NDX firmed.

What Happened: U.S. stock index futures auctioned within prior range alongside news the ECB would revise forward guidance and maintain asset purchases until “at least” March of 2022.

Additionally, the People’s Bank of China made a 50 basis-point cut to the reserve ratio at most banks given a weakened economic outlook. At the same time, G20 finance ministers are meeting over a global tax agreement and some concerns were raised over the spread of COVID-19 variants.

Ahead is the WASDE crop report for July and Fed speak by Neel Kashkari. Later, Janet Yellen will meet with finance ministers in Brussels.

What To Expect: Monday’s regular session (9:30 AM – 4:00 PM EST) in the S&P 500 will likely open inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

Adding, last week, U.S. stock index futures auctioned sideways to higher, only after enduring a brief liquidation alongside anxieties surrounding the spread of COVID-19 variants, as well as an evolution in monetary policy.

Expectations into the middle of July call for a supported S&P 500; thereafter, the window for fundamental dynamics to take over is opened.

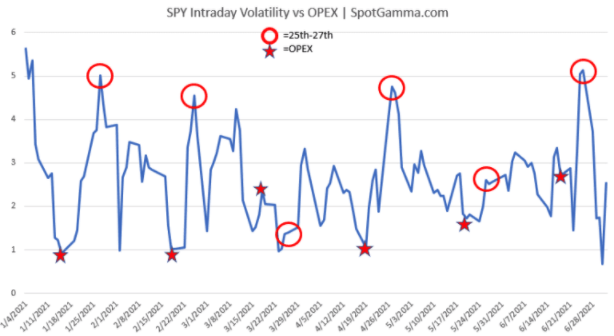

According to SpotGamma, “[t]he week after [options] expiration the market tends to experience its largest intraday volatility which corresponds to the reduction in large options positions, and the hedging associated with them.”

These expectations of increased volatility line up with the busy earnings season, kicked off by banks reporting second-quarter results this week. Additionally, a focus for participants in the coming days are some releases on consumer, producer, and import prices, as well as industrial production, consumer sentiment, and retail sales.

For today, participants can trade from the following frameworks.

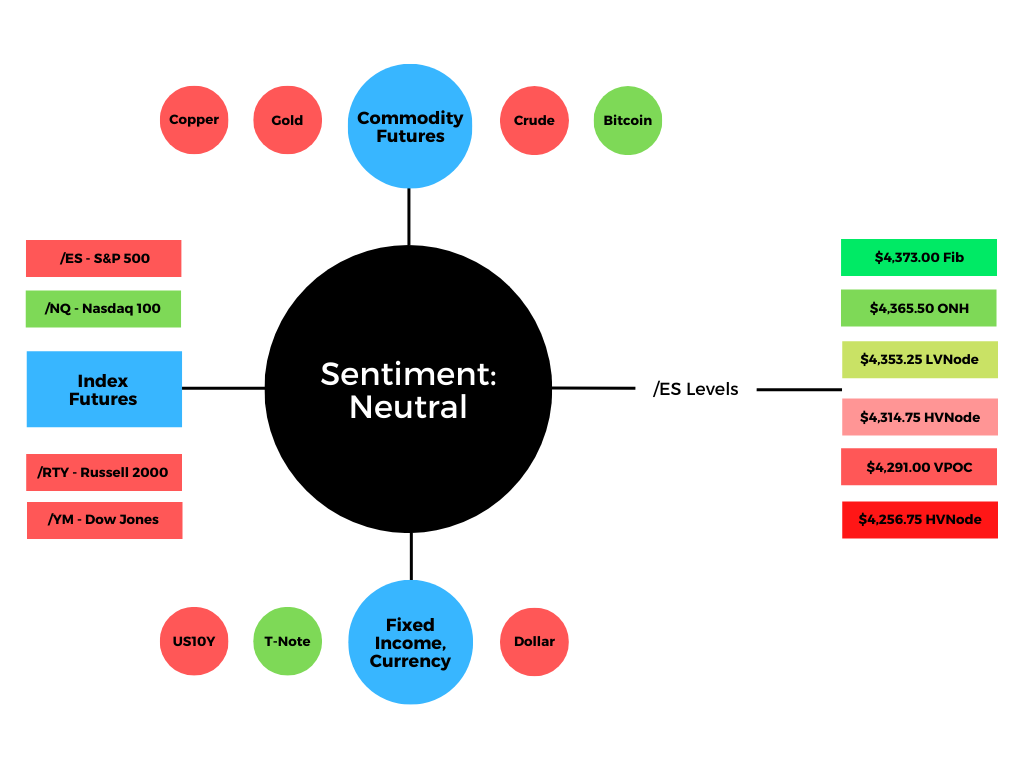

In the best case, the S&P 500 trades sideways or higher; activity above the high volume area (HVNode) pivot at $4,341.75 puts in play the $4,353.25 low volume area (LVNode). Trade beyond that signpost could reach as high as the $4,365.50 overnight high (ONH) and $4,373.00 Fibonacci extension.

In the worst case, the S&P 500 trades lower; activity below $4,341.75 puts in play the $4,314.75 HVNode. Initiative trade beyond that signpost could reach as low as the $4,291.00 untested Point of Control (POC) and $4,256.75 HVNode.

Volume Areas: A structurally sound market will build on past areas of high volume. Should the market trend for long periods of time, it will lack sound structure (identified as a low volume area which denotes directional conviction and ought to offer support on any test). If participants were to auction and find acceptance into areas of prior low volume, then future discovery ought to be volatile and quick as participants look to areas of high volume for favorable entry or exit. Overnight Rally Highs (Lows): Typically, there is a low historical probability associated with overnight rally-highs (lows) ending the upside (downside) discovery process. POCs: POCs are valuable as they denote areas where two-sided trade was most prevalent. Participants will respond to future tests of value as they offer favorable entry and exit.

News And Analysis

Economy | Global tax overhaul gains steam as G20 backs new levies. (NYT)

FinTech | Once Robinhood ‘house money’ gone, trading to lose allure. (NI)

FinTech | On crypto exchanges, the trades do not always add up right. (BBG)

Markets | Dealmakers see M&A rush, then chills, on antitrust progress. (REU)

Economy | China’s rate cut points to weaker than expected economy. (BBG)

FinTech | Square CEO doubles down on crypto, adds hardware wallet. (FL)

Economy | Recovery diminishes risks for reducing pandemic support. (Moody’s)

Energy | Oil prices loom over Biden’s bid to throttle drilling right sales. (BBG)

Economy | ECB’s Lagarde foresees a July policy shift, 2022 transition. (BBG)

What People Are Saying

About

Renato founded Physik Invest after going through years of self-education, strategy development, and trial-and-error. His work reporting in the finance and technology space, interviewing leaders such as John Chambers, founder, and CEO, JC2 Ventures, Kevin O’Leary, businessman and Shark Tank host, Catherine Wood, CEO and CIO, ARK Invest, among others, afforded him the perspective and know-how very few come by.

Having worked in engineering and majored in economics, Renato is very detailed and analytical. His approach to the markets isn’t built on hope or guessing. Instead, he leverages the unique dynamics of time and volatility to efficiently act on opportunity.

Disclaimer

At this time, Physik Invest does not manage outside capital and is not licensed. In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.